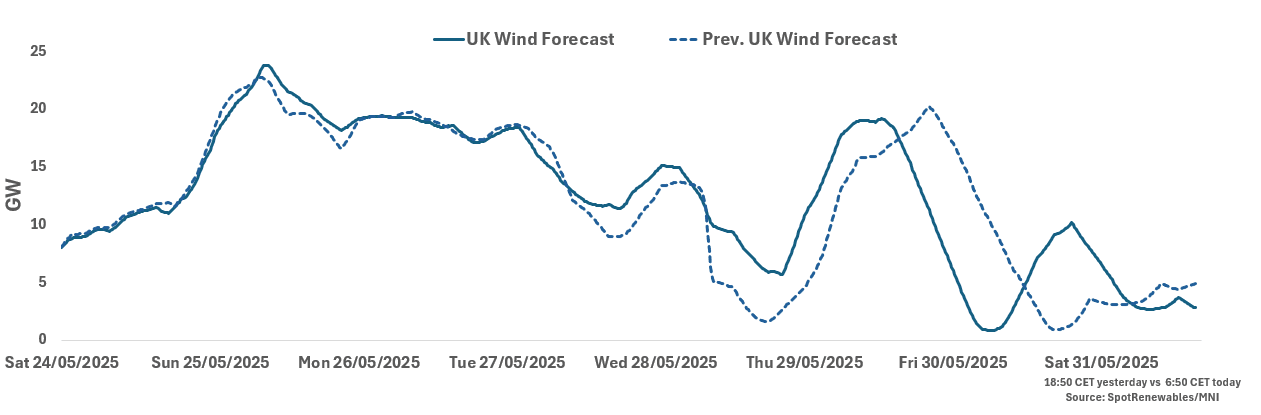

RENEWABLES: UK Morning Wind Forecast

See the latest UK renewables forecast for base-load hours for the next seven days. UK wind is expected to be between 50-71% load factors over 25-27 May before dropping to a 38% load factor on 28 May.

UK: Wind for 24-31 May

- 24 May: 10.98GW

- 25 May: 20.42GW

- 26 May: 18.60GW

- 27 May: 14.30GW

- 28 May: 10.89GW

- 29 May: 15.01GW

- 30 May: 5.38GW

31 May: 4.73GW

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

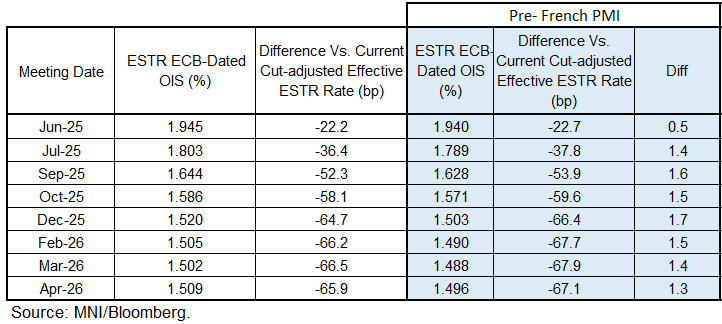

STIR: French/German Flash PMIs Don’t Change Near-term ECB Outlook

As noted above, there was little market reaction to the German and French flash April PMIs, even as both countries saw weaker-than-expected services readings. The prints haven’t really changed the outlook for near-term ECB policy, with a 25bp June cut still ~90% implied in OIS and a subsequent cut in July almost 60% implied.

- Year-end implied rates are ~1.5bps more hawkish than before the French data, with this morning’s rise in Bund yields setting the tone. 65bps of cuts are priced through December.

- After reaching a multi-month low of -39.0 ticks yesterday, the ER M5/M6 spread has since steepened back to -34.5 ticks at typing, +3.5 ticks on the session.

BUNDS: Trade developments are firmly at the forefront

- Tariffs are clearly at the forefront, EGBs and Bund have brushed aside the weaker German PMIs, Bund now tests Yesterday's low, with the Risk Tone tilted to the upside following Trump's comment on Powell, and offers of a good deal for China on any potential trade talks.

- Yesterday's low in Bund is still holding right now, but downside traction will Open to 130.87, the 17th April low.

GERMAN DATA: Apr Flash PMI: Tariff-related Impacts Apparent Across Sectors

The German April flash services PMI was weaker than expected at 48.8 (vs 50.2 cons, 50.9 prior). This was the first contractionary reading since November 2023, and the lowest since February 2024. Taken alongside the soft French services reading, the Eurozone-wide print is set to miss expectations of 50.5. The manufacturing index softened a touch to 48.0 (vs 47.6 cons, 48.3 prior), implying a slightly contractionary composite reading of 49.7 (vs 50.5 cons, 51.3 prior).

Tariff-related impacts are apparent, with services firms suffering from heightened uncertainty and manufacturers citing order frontloading and stock building.

Key notes from the release:

- "Service providers commented on the influence of concerns over tariffs and related uncertainty, with some clients reportedly delaying decision-making and reining in spending amid worries about the economic and political outlook".

- "Goods producers meanwhile noted a second straight monthly rise in new orders, supported by a first increase in export sales in over three years"..."there was evidence from panellists of the increases being partly driven by the frontloading of orders and related stockbuilding".

- "Both manufacturers and services firms revised down their growth expectations for the coming year, with the latter seeing sentiment deteriorate particularly sharply to the weakest since September 2023".

- "The decline in German private sector employment extended to an eleventh straight month in April"..."Further retrenchment in the manufacturing sector contrasted with sustained job creation in the service sector".

- "A slight uptick in the rate of inflation in average prices charged for goods and services"..."Manufacturers raised charges despite reporting a steep and accelerated reduction in input costs in April....Services firms, on the other hand, recorded a sharp and slightly quicker increase in operating expenses".

- "Data were collected 9-22 April".