US CREDIT SUPPLY: UBS $Benchmark Debt Offering in 5 Parts FV

Sep-18 17:25

(A2/A-/Apos)

- FV 4.25NC3.25 +75a, 6NC5 Variable +83a, 11.5NC10.5 Variable +92a

- IPT 4.25NC3.25 Variable +90-95, 6NC5 Variable +105a, 11.5NC10.5 Variable +120a

- 4.25NC3.25 FRN, 6NC5 FRN

- UBS secondary curve, with 2030s trading at ~g70-75, and 2036 trading at ~g92.

- Issuer: UBS Group AG (UBS)

- Format: 144a Reg S, senior unsecured

- Bookrunners: UBS (B&D)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: CAD Weakens Post CPI, Softer Equities Weigh on AUD & NZD

Aug-19 17:19

- Despite some initial weakness on Tuesday, the USD index tilted back into positive territory late in the session, set to moderately extend the rally this week. Price action was assisted by a dip lower for the major equity benchmarks, as a cautious risk off mood prevails given the lack of progress regarding a Russia/Ukraine ceasefire and the notable weakness for tech stocks in the US.

- Canada inflation data came in slightly below expectations and while unlikely to prompt renewed easing from the BOC, the Canadian dollar has sold off today. USDCAD has risen 0.4% to 1.3860, closing in on the August 01 highs off 1.3879. A break of this level would cancel a bear threat and resume the recent bull cycle.

- Elsewhere, risk dynamics have negatively impacted the likes of AUD and NZD, while Norwegian Krone is at the bottom of the G10 leaderboard.

- For AUDUSD, the pair is comfortably off its most recent highs but continues to trade in a range. From a trend perspective, the condition remains bullish highlighted by MA studies that remain in a bull-mode position; however, spot has narrowed the gap substantially to key support at 0.6419, the Aug 1 low.

- Kiwi weakness is notable ahead of Wednesday’s RBNZ decision, recording the first print below 0.5900 in two weeks. With a 25bp cut widely forecast, attention will be on the revised RBNZ outlook and tone of the statement and press conference. The focus is likely to be on the projected OCR path and whether it is revised lower suggesting further easing towards stimulatory territory as excess capacity persists.

- GBPUSD has consolidated around the 1.35 mark on Tuesday amid gilts paring some of yesterday's weakness. A technical bull cycle remains intact, keeping sights on 1.3636, the 76.4% retracement of the bear leg between Jul 1 and Aug 1 ahead of tomorrow's UK CPI release.

- FOMC minutes are also due for release tomorrow before the Jackson Hole symposium kicks off Thursday.

US TSY FUTURES: September'25-December'25 Roll Update

Aug-19 17:18

Latest Tsy quarterly futures roll volumes from September'25 to December'25 below. Percentage complete is running 5% or lower across the curve ahead the "First Notice" date on August 29. Current roll details:

- TUU5/TUZ5 appr 87,200 from -8.25 to -8.0, -8.0 last; 4% complete

- FVU5/FVZ5 appr 293,000 from -5.0 to -4.25, -4.75 last; 7% complete

- TYU5/TYZ5 appr 78,900 from -0.25 to +0.25, -0.25 last; 5% complete

- UXYU5/UXYZ5 under 22,500 from 0.5 to 1.0, 1.0 last; 2% complete

- USU5/USZ5 appr 38,100 from 13.25 to 14.0, 13.75 last; 4% complete

- WNU5/WNZ5 appr 38,800 from 8.0 to 8.5, 8.25 last; 2% complete

- Reminder, Sep futures don't expire until next month: 10s, 30s and Ultras on September 22, 2s and 5s on September 30. Meanwhile, Sep'25 Tsy options will expire this Friday, August 22.

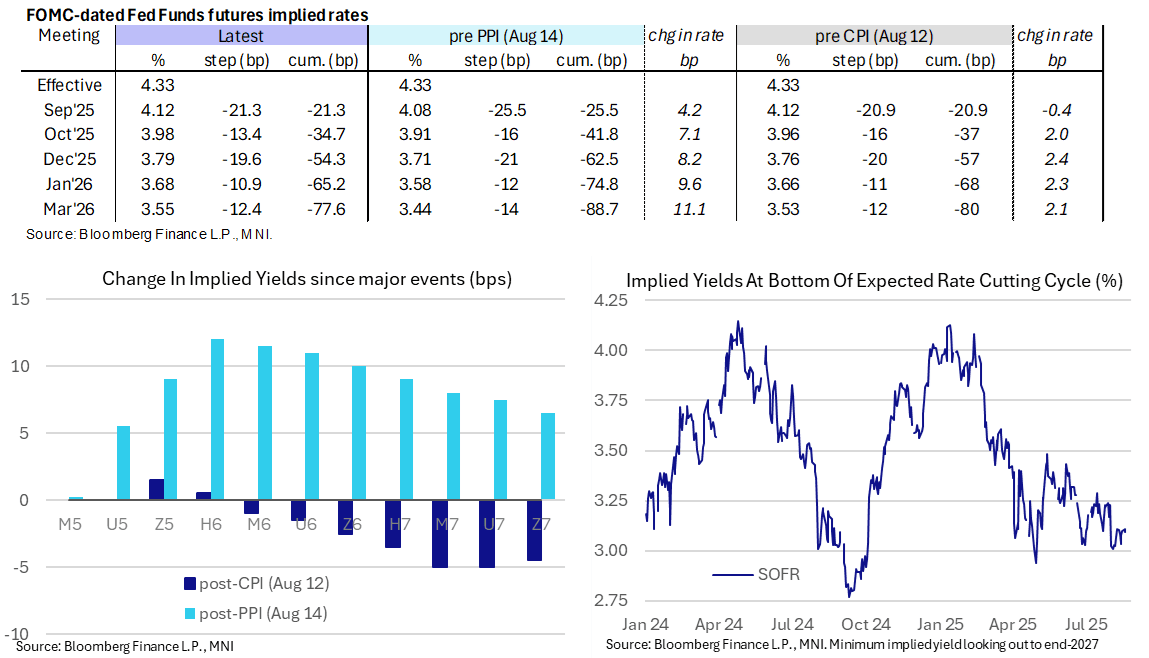

STIR: Fed Rate Path Keeps To Narrow Range Seen So Far This Week

Aug-19 17:06

- Fed Funds implied rates are marginally softer on the day for meetings out to Mar 2026 after a 1bp decline since the NY crossover.

- US housing data was mixed (strong housing starts but the more underlying building permits data were weak) and there was some mild spillover from a dovish reaction to CAD CPI.

- Cumulative cuts from 4.33% effective: 21.5bp Sep, 34.5bp Oct, 54.5bp Dec, 65bp Jan and 77.5bp Mar.

- The SOFR implied terminal yield of 3.095% (SFRH7) continues to hold particularly narrow ranges so far this week. It more broadly holds the +/-5bp of 125bp of cuts from current levels range seen since the Aug 1 payrolls report.

- Fed VC Supervision Bowman (permanent voter, dove) on Bloomberg TV didn’t have an impact on near-term rates earlier, focusing on banking supervision with further comments to come on that front at a Blockchain Symposium at 1410ET (text only).

- Tomorrow sees the FOMC minutes before Powell's Jackson Hole address on Friday. However, when it comes to Sept cut prospects, the August payrolls and CPI releases plus QCEW details (for preliminary payroll benchmark revision estimates) are all still to come before the next FOMC decision on Sep 17.