AUSSIE 3-YEAR TECHS: (U6) Corrective Cycle

* RES 3: 96.064 - 61.8% retracement Oct '25 - Mar Downleg (cont) * RES 2: 95.925 - High Jan 9 (cont)...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Late SOFR/Treasury Option Roundup: Decent Second Half Calls

SOFR & Treasury options trade outlined below: Pick-up in secopnd half calls after surge in Sep and Dec SOFR put volumes since Pres Trump's threatening social media posts to Iran this morning. Underlying futures near the middle of the session range. Projected rate pricing (hike) looks steady to slightly less hawkish vs late Tuesday levels (*) with Dec still projected first 25bp hike: Jun'26 at +.8bp (+.7bp), Jul'26 at +3.5bp (+3.9bp), Sep'26 at +10.7bp (+11.5bp), Oct'26 at +15.5bp (+16.4bp), Dec'26 +24.6bp (+25.5bp).

- SOFR Options:

- +10,000 SFRZ6 96.43/96.62 call spds, 2.0 ref 96.05

- Block, 6,000 SFRZ6 96.37/96.50/98.00 broken call trees, .25 net

- Block, 16,000 SFRU6 96.18/96.25/96.37/96.43 call condors, 3.5 net ref 96.215

- +4,000 SFRZ6 96.31/96.75 call spds, 5.0 vs. 96.065/0.18%

- -4,000 SFRU6 96.12/96.37 put over risk reversals. 3.0 vs. 96.22/0.58%

- +10,000 SFRU6 96.25/96.37/96.75 call tree w/ 96.31/96.43/96.81 call tree strip, 3.0 total

- +3,000 SFRU6 96.25 straddle vs. 96.50 calls, 15.5 net

- +16,000 SFRZ6 96.06/96.18 put spds, 6.5 vs. 96.075/0.13%

- 12,300 SFRU6 96.87 calls, 1.5

- -3,000 OQU5 95.87 puts, 17.5 vs. 95.975/0.45%

- -2,000 SFRZ6 96.00 puts, 17.75 ref 96.065

- +4,000 SFRU6 96.12/96.31/96.50 call trees, 4.75

- +10,000 0QU6 95.25/95.37/95.75 put trees, 4.0 ref 95.985

- -2,000 SFRN6 96.18/96.25 strangles, 9.0-9.25 ref 96.205

- +2,000 SFRZ6 95.87/96.00 put spds, 4.75 vs. 96.04/0.08%

- 34,000 SFRZ6 96.06/96.18 put spds

- 20,000 SFRU6 96.06/96.18/96.31/96.43 put condors ref 96.205

- 9,000 SFRU6/SFRZ6 96.12/96.25 put spd spds

- 1,500 SFRZ6 95.93/96.06/96.18 call flys

- 1,750 SFRU6 95.87/95.93/96.12 broken put trees

- 3,000 SFRU6 96.00 puts ref 96.20

- 2,350 SFRZ6 96.50 calls, 7.25 vs. 96.055/0.22%

- 1,500 0QM6 96.00/96.12/96.25 call flys, 1.5

- Treasury Options:

- 8,200 FVN6 106.75 calls, 20.5 ref 106-22.25

- 30,000 wk1 TY 109.75 calls, 19 ref 109-07 (exp 07/02)

- 15,000 TYQ6 108/109/109.5/110.5 iron condors hah - not at all

- 5,250 TYN6 108/109 puts, 17 ref 109-07

- 1,500 TYU6 102.5 puts, 3 (yes, Sep 10Y 102.5 puts)

- 2,500 TYQ6 107/108.5 put spds ref 109-02

- 3,900 FVN6 107.5 calls ref 106-23.25

- 4,000 Wed wkly FV 106.5/106.75/107 call flys

- +2,500 Wed wkly TY 108.5 puts, 2 vs. 109-05.5/0.08% (exp today)

- -1,250 wk2 TY 108.5/109/109.5 put trees, 15 vs. 109-04.5/0.20% (exp Fri)

- +2,000 TYN6 108/109.5 put spds, 35 ref 109-06

EURJPY TECHS: Bullish Structure

- RES 4: 187.95 High Apr 17 and the bull trigger

- RES 3: 187.56 High Apr 30

- RES 2: 186.56 76.4% retracement of the Apr 17 - May 6 bear leg

- RES 1: 186.21 High Jun 5

- PRICE: 185.39 @ 17:10 BST Jun 10

- SUP 1: 184.01 Low Jun 8

- SUP 2: 183.50 Low May 07

- SUP 3: 182.05 Low May 06 and a bear trigger

- SUP 4: 181.87 Low Mar 16

The trend condition in EURJPY remains bullish and the latest appears to be corrective for now. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. A resumption of gains would open 186.56, a Fibonacci retracement. Key support lies at 182.05, the May 6 low. Clearance of this level would highlight an important bearish development. Initial firm support to watch is 184.01, Monday’s low.

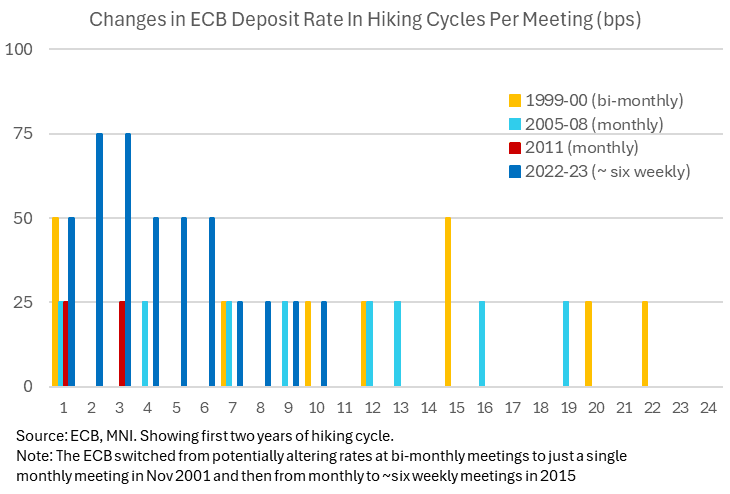

ECB: No Clear Historical Precedent On ECB's Favoured Hiking Cadence

The following is taken from the MNI ECB Preview, which can be found in full here.

- The ECB is fully priced and unanimously expected to hike its three key interest rates on Thursday having been on hold since it last cut 25bps back in June 2025. It will see the deposit rate raised by 25bps to 2.25%, the top end of the neutral range of 1.75-2.25% estimated by ECB staff. That said, some analysts view 2.5% as neutral, and the ECB’s range inherently embeds a great deal of uncertainty”.

- With this week’s decision seen as locked in and multiple hikes having been priced in for some time, attention will clearly be on gauging the Governing Council’s willingness to hike rates further.

- That’s both in terms of the speed and magnitude of hikes in moves that most expect will be portrayed as a re-calibration, or “measured adjustment” rather than a more material hiking cycle.

- The more contentious point currently is whether the ECB will follow with a back-to-back hike in July (~10bp of additional hikes priced) or wait until September (cumulative 28bp priced).

- The shift from an implied 5bp of hikes for July to 10bp over the past week has firmly reduced the appeal of paying July OIS in what had looked like asymmetrical risk of a hawkish surprise at those levels.

- Historical precedent doesn’t offer a strong preference for back-to-back or more spaced out moves in prior hiking cycles – see chart – with the market currently looking for a path that is closer to the 2011 experience. A caveat to the chart is the different meeting frequencies over time.

- One of the cleanest ways of interpreting a July hike potential could be whether Lagarde emphasises that the GC will have important data on second-round effects by then or whether she emphasises patience, for example by stressing that it will receive a lot more data by the September meeting.

- Whilst the revised projections and broad commentary will no doubt set the tone, it may still be worth watching how President Lagarde signs off the press conference. A rough repeat of “I wish you a happy day, happy summer for those of you who leave early” from when she closed out the June 2025 press conference could be construed as dovish seeing as that ended up being the start of the pause in rates (she followed it up in July with “I wish you all a nice wait and see holiday”).