US 10YR FUTURE TECHS: (U6) Bear Cycle Still In Play

* RES 4: 111-03 50.0% retracement of the Mar 2 - May 19 bear leg * RES 3: 110-28+ High May 7, 2026 *...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Late Equities Roundup: Middle East Uncertainty Weighs on Stocks

- US equity indexes remain weaker late Wednesday, ongoing middle east tensions sapped any positive sentiment gained from this morning's in-line May CPI inflation data. Late pressure came on the back of Israeli official Katz stating the IDF was "poised to strike Iran with great force" after Trump said the US will "resume attacking Iran very hard" this morning.

- Currently, the DJIA trades -1.45%, SPX eminis -1.2%, the Nasdaq -1.5%.

- A combination of IT (hardware & chip makers), Industrials (construction/engineering) and Consumer Discretionary (auto & travel) sector shares continued to underperform in late trade.

- Super Micro Computer led declines -20.4% after it announced plans to issue $7B in equity/equity-linked transactions to help fund some $39B in AI-related customer orders. Other laggers include: QUALCOMM, ON Semiconductor Corp, Broadcom, First Solar and Western Digital Corp - all down between 5-6%.

- The Industrials sector was weighed down by: Generac Holdings, Caterpillar, GE Vernova, Quanta Services Inc and Eaton Corp - 5.75% to 7.25% lower. Meanwhile, autos and travel related shares weighed down the Consumer Discretionary sector, the following -4-6%: General Motors, Carnival Corp, Royal Caribbean Cruises, Norwegian Cruise Line, Tesla and Ford Motor Co.

- On the positive side, oil and gas shares helped the Energy sector outperform as crude prices bounced in the first half (WTI +2.3 at $90.50/bbl): Devon Energy, APA Corp, ConocoPhillips, ONEOK, EOG Resources and Targa Resources gained 3.5-6% in the second half.

COMMODITIES: Crude Rallies as Trump Threatens Further Iran Strikes, Gold Falls

- Crude oil extended gains after President Trump said that the US “will be attacking Iran hard today.” This followed earlier comments from Trump that Iran had taken too long to negotiate a deal and would “pay the price”.

- WTI Jul 26 is up by 2.6% at $90.5/bbl.

- Trump’s remarks will taper optimism that there is an imminent deal to reopen the Strait of Hormuz. Trump simultaneously said that a deal is near, but that additional strikes will continue. Overall, his comments highlight the fact that we could be further from a deal than officials and mediators will publicly admit.

- For WTI futures, the trend condition remains bullish and recent weakness appears corrective.

- A clear breach of key support at $90.51, the 50-day EMA would highlight a top and the start of a stronger correction, opening $77.22, the Apr 17 low.

- First resistance is at $97.00, the Jun 3 high, with key resistance defined at $105.21, the May 18 high.

- Meanwhile, precious metals have fallen further today, with spot gold down by 3.6% at $4,108/oz and silver declining by 0.9% to $64.8/oz.

- A bear theme in gold remains intact and this week’s extension reinforces the downtrend. The metal has pierced the $4,200.0 handle and a continuation lower would signal scope for a move towards the key medium-term support at $4,099.2, the Mar 23 low.

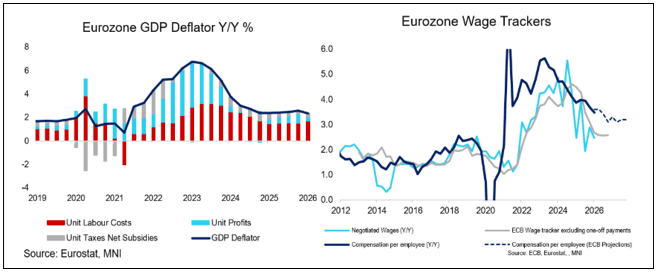

ECB: Macro Since Last ECB Decision - Wages: No Wage-Led Second Round Effects Yet

Compensation Per Employee Eases In Q1, Unit Profits Pull Back

- Eurozone compensation per employee eased to 3.5% Y/Y in Q1, down from 3.7% in Q4 for the lowest rate since Q1 2021. The ECB projected a 3.6% reading in its March baseline projections. At face value, the fact compensation pressures headed into the Iran war with downward momentum supports views expecting contained second round effect risks. Tracking wage expectations in surveys, negotiated wage and job posting data will be key in the coming months.

- That said, a weak productivity outcome for Q1 (-0.2% Y/Y on a per hour and per employee basis) meant that unit labour costs jumped to 3.6% Y/Y (vs 3.0% prior). This was above the ECB's 3.3% projection.

- Of course, Ireland has to be considered here. Given headline GDP growth declined to 0.3% Y/Y from 0.8% prior, mainly a function of Irish multinational accounting, productivity growth was mechanically skewed negative because employment and hours worked both rose 0.5% Y/Y. As such. we don't place too much weigh on the unit labour cost print, and focus more on compensation per employee.

- The overall GDP deflator pulled back to 2.3% Y/Y (vs 2.6% prior), versus an ECB projection of 2.6%. The contribution of unit labour costs to this annual reading increased to 1.7pp (vs 1.5pp prior), while unit profits declined to 0.3pp (vs 0.8pp prior).

- The declining unit profits contribution could be early evidence of companies absorbing higher (energy) input costs rather than passing them on. However, Q2 data will give a much better idea of these dynamics.

Corporate Telephone Survey: Medium-term wage signals appear favourable for now: "Contacts continued to anticipate moderating wage growth. On average, the quantitative indications provided would imply that wage growth is expected to slow, from 3.5% in 2025 to 2.9% in 2026 and 2.8% in 2027.". " a few contacts (around 10%) had made small upward revisions to their expectations for 2027 in view of the war in the Middle East, while a larger number (around 30%) saw the latter as an upside risk."

Indeed Wage Tracker: Eurozone posted wage growth remains contained, according to Indeed's latest wage tracker update. Eurozone-wide posted wage growth was 2.20% Y/Y in April, up from 2.13% in March but still below the 2.43% seen in February. That leaves 3mma growth at 2.25%, down from 2.33% prior for the lowest since July 2021