AUSSIE 10-YEAR TECHS: (U5) Recovers From Its Recent Lows

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.805/960 - High Aug 8 / High Apr 7

- PRICE: 95.605 @ 15:58 BST Sep 2

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.720 - 1.0% 10-dma envelope

Aussie 10-yr futures remain above their recent lows - for now. To the upside, the next resistance is at 96.207, a Fibonacci retracement point. Initial near-term resistance is seen at 95.805, the Aug 4 high. A break of this hurdle would be a bullish development. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (U5) Recovers With Treasuries

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.960 - High Apr 7

- PRICE: 95.755 @ 17:30 BST Aug 1

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.707 - 1.0% 10-dma envelope

Aussie 10-yr futures traded under pressure for much of last week, keeping prices subdued into Friday’s NFP print. The subsequent US 10y rally dragged Aussie 10-year futures with it, putting prices toward the top end of the recent range. To the upside, next resistance is at 96.207, a Fibonacci retracement point. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition.

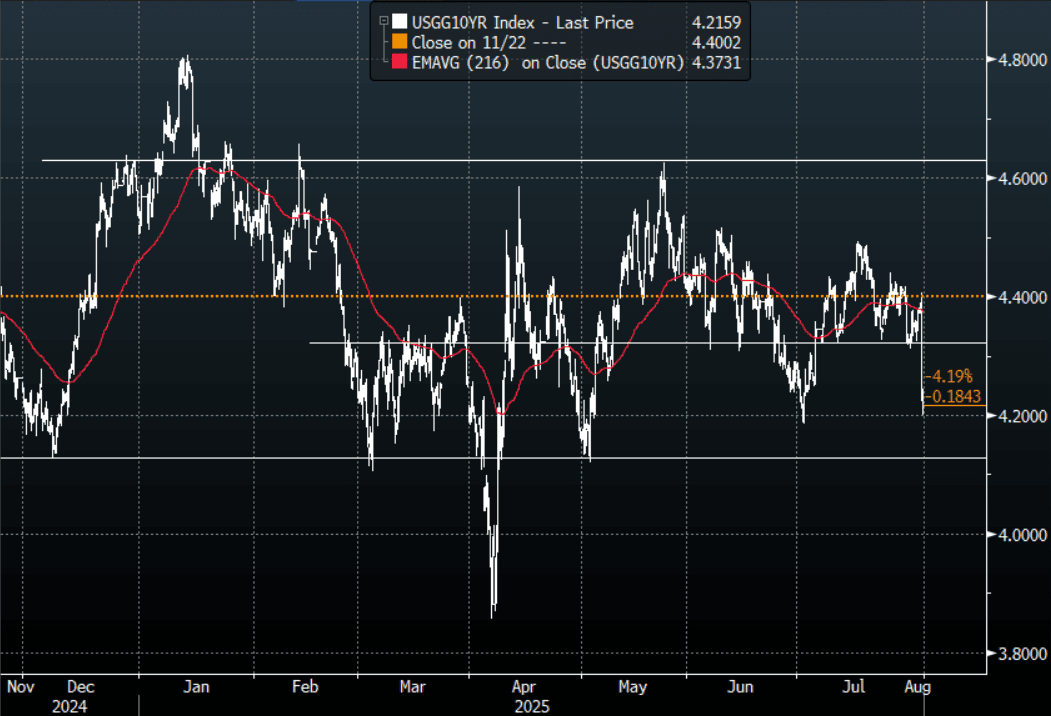

US TSYS: Yields Collapse Lower, Led By The Front-End

TYU5 reopens at 112-10+, up 0-04 from closing levels in today’s Asia-Pac session.

- Friday night the US 10-year yield had a range of 4.4060% - 4.2002%, closing around 4.216%.

- Treasury yields collapsed lower overnight; led by the front-end causing the yield curve to steepen (2s10s +11.53 at 53.012, 5s30s +13.74 at 106.324).

- MNI US DATA: Huge Downward Revisions For Payrolls Set The Tone. Nonfarm payrolls growth was weaker than expected in July at 73k (cons 104k) after huge downward revisions in both June (-133k to just 14k) and May (-125k to 19k). The downward revisions came from a combination of large shifts in both private and public payrolls, equally spread over both May and June.

- MNI FED: Bowman, Waller Cite Labor Concerns In Fed Dissents. Federal Reserve governors Michelle Bowman and Christopher Waller said Friday that they voted against the central bank’s "wait and see" rate policy this week because upside risks to price stability have diminished and it was time to proactively hedge against further weakening in the economy and the risk of damage to the labor market. In separate statements, the two governors said inflation is moving closer to the central bank's 2% target and cited increased concerns about the Fed's employment mandate.

- The 10-year yield had a powerful move lower in reaction to the NFP data, breaking below its 4.30% pivot within the wider range 4.10% - 4.65%. This now turns momentum lower in yields and you could expect buyers of treasuries on bounces back towards 4.30/35% now looking to initially test the 4.10% area. The move was even more aggressive in the 2-year which has rejected the move back towards 4% and now looks to target the pivotal 3.50% area.

Fig 1: 10-Year US Yield 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGB Yields Lower, As US Tsy Yields Plunge Post NFP

New Zealand government bond yields have opened lower across the curve, with the front end leading a touch in terms of yield losses. This follows in the aftermath of the US non-farms payroll report on Friday, which weighed notably on US Tsy yields. Front end NZGB yields are around 7.5bps lower, while longer dated tenors are down slightly less in yield terms.

- US Treasury futures gapped higher after the lower than expected jobs gain for July, June gains sharply down-revised, while unemployment rate held steady. Then futures extended higher (TYU5 +1-03 112-05) after lower than expected ISMs, lower UofM sentiment while 1Y inflation expectations climbs slightly on Friday. The 2yr Tsy yield finished down 27.5bps to 3.68%, the 10yr lost near 16bps to 4.22%.

- NZ's 2yr bond yield is back under 3.20%, fresh lows back to 2022. The 10yr is back under 4.44%, but remains within recent ranges.

- In the swap rate space, the 2yr is at 2.95%, down over 7bps. April lows were around 2.88%. The 10yr is around 3.89%, off by a similar amount and at fresh lows back to May of this year.

- Locally this week the main focus will be on Wednesday's Q2 labour market report. It is likely to show a contraction in employment and a further pickup in the unemployment rate and as a result further moderation in wage inflation. Q2 filled jobs fell 0.3% q/q after -0.1% signalling that there was job shedding in the quarter. The unemployment rate was stable in Q1 at 5.1%, helped by a 0.1pp fall in the participation rate, but this was up almost 2pp since the Q1 2022 trough. The economic recovery remains lacklustre despite 225bp of easing and thus given the lags the labour market is yet to pickup again.