EU HEALTHCARE: Trump Sends Letters to Pharma Companies

Bloomberg headlines out today regarding letters Trump has sent to various drug manufacturers globally. So far we see LLY, PFE, NOVO, ABBV, BING, BMY, NOVN, GILD, AZN, AMGN, JNJ, GSK, MRK, REGN and SANFP.

Trump Letter on Truth Social:

- Unacceptable Burden' of Brand Name Drug Prices Ends With Trump Administration

- Calling on U.S. Drug Makers to Extend Most-Favored-Nation Pricing to Medicaid

- Guarantee Most-Favored-Nation Pricing for Newly Launched Drugs

- Return Increased Revenues Abroad to U.S. Patients, Taxpayers

- Provide for Direct Purchasing at Most-Favored-Nation Pricing

- Expect U.S. Drug Makers to Engage Immediately With Health Secretary Kennedy, CMS Administrator Oz

- I Look Forward to Your Binding Commitments to Each of These Goals by September 29'

While this headline contains a lot of proposals, we think the Most Favored Nation pricing request is most important given the Administration could push for Medicaid and Medicare to adopt these more stringent pricing mechanisms. Recall, the US already "negotiates" pricing for the top 10 drugs in the Medicare program; however, this would appear to indicate the Administration's desire to negotiate every drug approved for Medicare/Medicaid. It is too soon to determine real impacts to Global Pharma; however, these headlines will persist and put pressure on the sector in both equity and credit markets.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Wednesday Data Calendar: June ADP Employment

- US Data/Speaker Calendar (prior, estimate)

- 07/02 0700 MBA Mortgage Applications (1.1%, --)

- 07/02 0730 Challenger Job Cuts YoY (47.0%, --)

- 07/02 0815 ADP Employment Change (37k, 95k)

- 07/02 1130 US Tsy $65B 17W bill auctions

- Source: Bloomberg Finance L.P. / MNI

BONDS: EGBs-GILTS CASH CLOSE: Flattening To Start The Quarter

European yields pulled back Tuesday in a flattening move.

- There was a strong rally in early trade, largely following the cue of US Treasuries as the month/quarter got underway.

- Gains faded by mid-afternoon in Europe, with US data releases showing firmer-than-expected job openings, and still-elevated manufacturing sector prices.

- The German curve bull flattened on the day, with the UK's twist flattening. Periphery/semi-core EGB spreads widened slightly, with Greece underperforming.

- In data, Spanish PMI beat expectations but Italy missed. Eurozone June flash inflation metrics came in line with consensus though ECB 1-year and 3-year ahead inflation expectations both eased.

- BoE's Bailey reiterated that the direction of rates continues to be downwards, while ECB's Lagarde repeated that there was no commitment to any particular rate path.

- Wednesday's calendar includes labor market data for Italy, Spain and the Eurozone, and commentary from dovish BoE dissenter Taylor.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.2bps at 1.849%, 5-Yr is down 2.2bps at 2.148%, 10-Yr is down 3.3bps at 2.574%, and 30-Yr is down 4.7bps at 3.053%.

- UK: The 2-Yr yield is up 1bps at 3.827%, 5-Yr is down 1.4bps at 3.936%, 10-Yr is down 3.5bps at 4.454%, and 30-Yr is down 5bps at 5.229%.

- Italian BTP spread up 0.6bps at 87.5bps / Greek up 2.1bps at 71.1bps

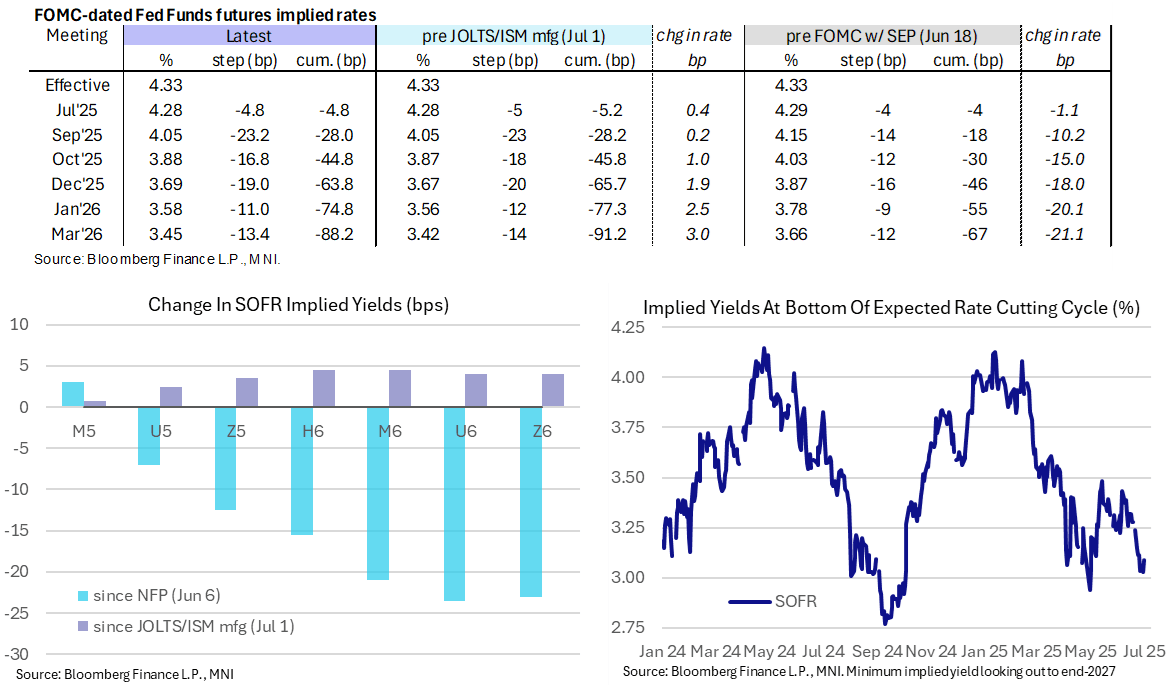

STIR: Fed Rate Path Holding A Sizeable Shift Off Recent Dovish Lows

- Fed Funds implied rates are holding the day’s marked increase, with a surprisingly strong JOLTS report adding to an earlier intraday rise by ruling out a sharper labor deterioration (even if it’s only for May as opposed to upcoming June releases tomorrow and Thursday).

- Cumulative cuts from 4.33% effective: 5bp Jul, 28bp Sep, 45bp Oct, 64bp Dec, 75bp Jan and 88bp Mar.

- The 64bp of cuts for 2025 compares with 69bp at the NY crossover.

- The SOFR implied terminal yield of 3.09% (SFRZ6) is 6bp higher on the day with 4bp of that coming post-JOLTS as it lifts away from what had been close to its lowest level since Oct 2024, i.e. prior to the US presidential election.

- The ISM manufacturing survey meanwhile improved a touch in June as broadly expected (49.0 vs cons 48.8 after 48.5 in May) along with still elevated prices paid (69.8 after 69.4 in May), although with weak new orders (46.4 after 47.6) and employment (45.0 after 46.8) components. Elsewhere, the final manufacturing PMI was stronger than previously thought at a robust 52.9 in June (flash and cons 52.0) after 52.0 in May for its highest since May 2022.

- Shortly ahead of the data, Fed Chair Powell was asked if July is too soon to seriously consider a rate cut and he certainly didn’t categorially rule it out, even if it's couched in typical central bank-speak: "Yeah, I really can't say - it's going to depend on the data. And we are going meeting by meeting. I mentioned, you know, how I'm thinking about that, but I wouldn't take any meeting off the table or put it directly on the table, it's going to depend on how the data evolve."

- Tomorrow sees important labor updates in ADP employment and Challenger job cuts before Payrolls and ISM Services on Thursday ahead of Friday's Independence Day holiday.