EM LATAM CREDIT: Trinidad & Tobago: Exxon Exploration - Positive

(TRITOB; Ba2/BBB-/NR)

"Trinidad awards deepwater blocks to Exxon, could see $21.7 billion investment, minister says" - Reuters

Trinidad and Tobago is geographically close to Guyana where Exxon has already been authorized to explore and develop deep water oil reserves.

The U.S. based global super major integrated oil & gas company said it would first need to invest USD43mn in initial 3D seismic studies and expected to use some of its knowledge from successful drilling in Guyana.

Reserves need to be confirmed but already the company has confirmed more than 11 billion barrels of recoverable oil and gas at the neighboring waters of Guyana.

TRITOB 34s were last quoted T+219bp, 23bp tighter QTD and 16bp wider YTD.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Midday Equities Roundup: Miners, Pharmaceuticals & Banks Lagging

- Stocks are trading near steady (SPX eminis) to mixed Tuesday, the DJIA underperforming at midday with the Materials (specifically mining stocks w/ Gold lower) and Health Care sectors weighed by pharmaceuticals.

- At the moment, the DJIA trades down 329.57 points (-0.74%) at 44129.49, S&P E-Minis down 8.25 points (-0.13%) at 6302.25, the Nasdaq up 121.9 points (0.6%) at 20762.9.

- Weighing on the Materials sector in the first half: Newmont Corp -8.85%, Freeport-McMoRan -5.00%, Steel Dynamics -2.14%, Vulcan Materials -1.96% and Nucor Corp -1.89%. Pharmaceuticals weighed on the Health Care sector: Agilent Technologies -3.31%, Eli Lilly & Co -3.11%, AbbVie Inc -3.05% and Regeneron Pharmaceuticals Inc -2.77%.

- Individually, some banks and services underperforming after reporting earnings this morning, namely Wells Fargo & Co -5.77%, Blackrock -5.57%, State Street -3.70%, American Express -2.59%.

- On the positive side, semiconductor makers supported the the tech heavy Nasdaq after several were greenlighted for China imports: Super Micro Computer +8.08%, Advanced Micro Devices +7.11%, First Solar Inc +5.65%, NVIDIA Corp +4.45% and Synopsys Inc +2.76%.

- Earnings announcements expected early Wednesday: Prologis, Progressive, First Horizon, PNC Financial Services, Bank of America Corp, Johnson & Johnson, Goldman Sachs and Morgan Stanley. After the close: United Airlines Holdings, Rexford Industrial Realty, Alcoa Corp and Kinder Morgan.

BONDS: EGBs-GILTS CASH CLOSE: Early Rally Reverses After US CPI

Bunds outperformed Gilts Tuesday as a rally in the first half of the session reversed.

- Core FI saw solid gains through the morning, with 10Y Bund yields erasing most of the previous three sessions' rise, and Gilt yields touching the lowest intraday levels in 6 sessions.

- There was no major catalyst for the move, which looked through stronger-than-expected German ZEW and Eurozone industrial production data.

- The initial read of US CPI data extended the rally as core came in softer than expected, but global FI sold off about an hour later as it became clear that the report indicated rising tariff-related goods price pressures, pushing up breakeven inflation expectations.

- The German curve twist flattened, with the UK's leaning bear steeper. Periphery/semi-core EGB spreads were little changed on the day. PM Bayrou's 2026 budget announcement didn't bring any major moves in OAT spreads vs Bund.

- After hours we hear from BOE's Bailey and Chancellor Reeves at the Mansion House event.

- Wednesday's calendar highlight is UK CPI - MNI's preview is here (including our outlook for Thursday's labour market report). For CPI, we are watching headline closely and the biggest risk to this month’s print seems to be food inflation continuing to surprise to the upside.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.1bps at 1.887%, 5-Yr is down 1.5bps at 2.263%, 10-Yr is down 1.7bps at 2.712%, and 30-Yr is down 1.9bps at 3.226%.

- UK: The 2-Yr yield is up 2.4bps at 3.836%, 5-Yr is up 1.6bps at 4.031%, 10-Yr is up 2.5bps at 4.625%, and 30-Yr is up 2.8bps at 5.458%.

- Italian BTP spread down 0.3bps at 86bps / French OAT down 0.4bps at 70bps

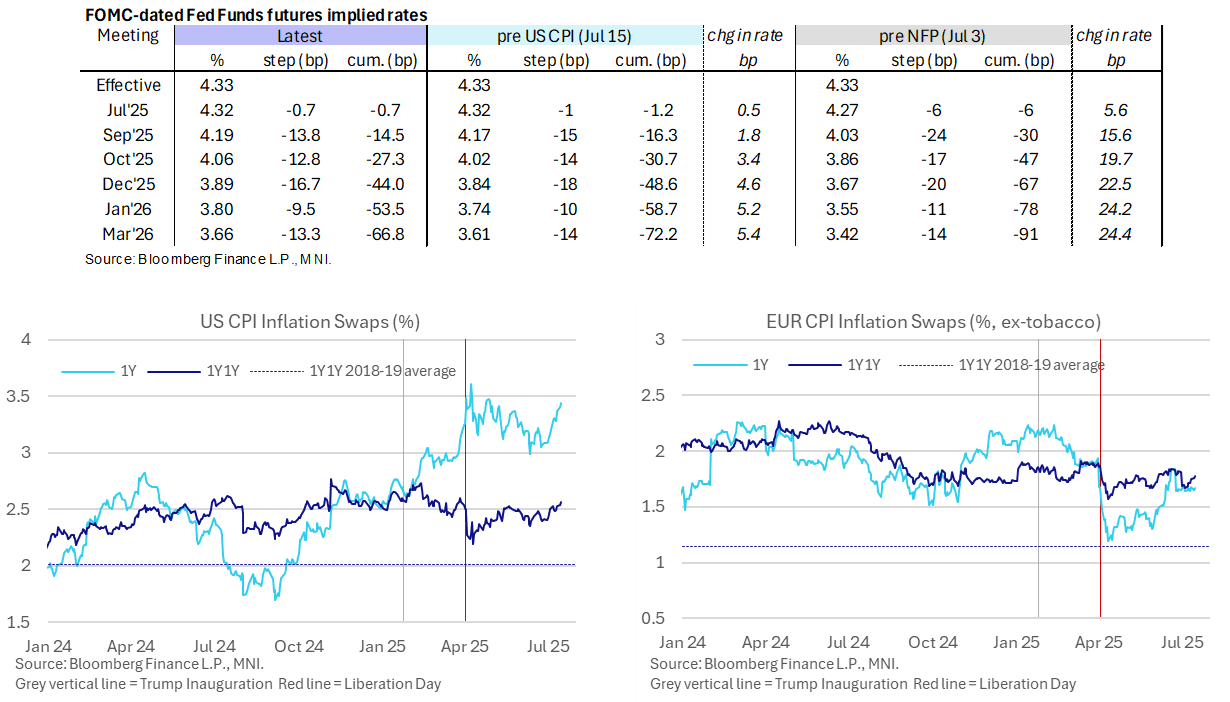

STIR: Fed Rates Hold Hawkish Shift On CPI Along With Short-Term Inflation Swaps

- Fed Funds futures are holding their belated push higher after a US CPI report for June which showed signs of increasing passthrough to consumer prices from tariffs.

- Cumulative cuts from 4.33% effective: 0.5bp Jul, 14.5bp Sep (vs 16.5bp pre CPI), 27.5bp Oct, 44bp Dec (vs 48.5bp), 53.5bp Jan and 67bp Mar (vs 72bp).

- The Dec 2025 implied rate is now 22.5bp higher than prior to the June non-farm payrolls report one and a half weeks ago.

- The CPI report extends a marked increase in short-term US inflation expectations. The 1Y inflation swap is 3.5bp higher today at 3.44%, following the 3.29% averaged through much of last week and 3.12% in the holiday-shortened week before that into Independence Day. This peaked at 3.61% (looking at closes) in the week after US reciprocal tariff announcements in April.

- Recent increases have been mostly confined to just 1Y, on the assumption that tariff increases have short-lived inflationary impacts, although 1Y1Y rates are drifting higher as well so it’s not entirely in isolation. See the below charts including a comparison with EU inflation swaps over the same period.