USDCAD TECHS: Trading Closer To Its Recent Highs

- RES 4: 1.4200 Round number resistance

- RES 3: 1.4167 50.0% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.4111 High Apr 10

- RES 1: 1.4080 High Oct 16

- PRICE: 1.4047 @ 16:49 BST Oct 17

- SUP 1: 1.3959/3884 20- and 50-day EMA values

- SUP 2: 1.3810 Bull channel base drawn from the Jul 23 low

- SUP 3: 1.3727 Low Aug 29 and a bear trigger

- SUP 4: 1.3689 Low Jul 28

The trend outlook in USDCAD is unchanged, a bull cycle remains intact and the pair is trading closer to its recent highs. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 1.4111, the Apr 10 high, and further out, scope is seen for an extension towards 1.4167, a Fibonacci retracement. First key support is 1.3884, the 50-day EMA. Support at the 20-day EMA lies at 1.3959.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDJPY TECHS: Challenges Support

- RES 4: 151.62 61.8% retracement of the Jan 10 - Apr 22 bear leg

- RES 3: 150.92 High Aug 1 and a key resistance

- RES 2: 149.81 76.4% retracement of the Aug 1 - 14 bear leg

- RES 1: 148.17/149.14 High Sep 11 / High Sep 3

- PRICE: 146.73 @ 20:57 BST Sep 17

- SUP 1: 145.49 Low Seo 17

- SUP 2: 145.40 50% retracement of the Apr - Aug upleg

- SUP 3: 144.10 61.8% retracement of the Apr - Aug upleg

- SUP 4: 143.45 Low Jul 3

USDJPY traded sharply lower Wednesday before finding support. The pair cleared support at 146.21, the Aug 14 low and a bear trigger. A break of this level highlights a stronger bearish threat and highlights a range breakout. Note too that price has pierced 145.80, a trendline drawn from the Apr 22 low. A resumption of weakness would open 145.40, a Fibonacci retracement. On the upside, key resistance is at 149.14, the Sep 3 high.

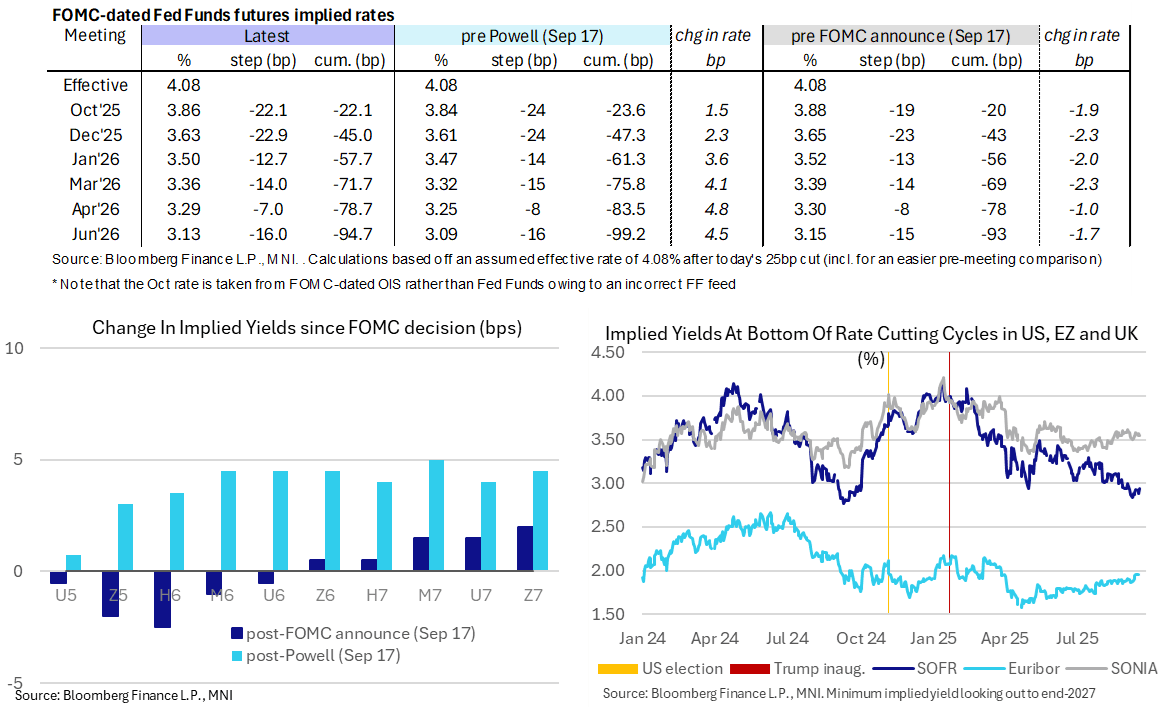

STIR: Rally Pared,Fed Rates Lean To Two More Cuts This Year But Not Fully Priced

- With Fed Chair Powell’s press conference wrapped up, Fed Funds implied rates have seen a sizeable paring of their dovish shift on the initial FOMC announcement and SEP including a highly anticipated dot plot.

- Implied rates out to mid-2026 are 1.5-2.5bp lower since the FOMC announcement having climbed between 1.5-4.5bp higher during Powell press conference, mostly in the first half.

- Cumulative cuts from an assumed 4.08% effective: 22bp Oct (vs 20bp pre-FOMC and 23.5bp pre-Powell), 45bp Dec (vs 43bp and 47.5bp), 57.5bp Jan, 71.5bp Mar (vs 69bp and 76bp), 78.5bp Apr and 94.5bp Jun (vs 93bp and 99bp).

- [Note that these pre-FOMC levels for cumulative cuts are adjusted for today’s 25bp cut, and that the Oct level more broadly is taken from OIS rather than Fed Funds owing to an incorrect FF feed].

- SOFR futures are 3-5 ticks lower through Z5-Z7 contracts since Powell started speaking, having fully reversed the initial rally from Z6 onwards (-0.5 post-FOMC and -5.5 on the day for the Z6, -2 post-FOMC and -7 on the day for the Z7).

- In yield terms, the terminal 2.935% (SFRH7) is 0.5bp higher post-FOMC for 5.5bps higher on the day having consistently climbed ahead of the decision. It’s at the high end of recent post-NFP ranges and now suggests ~115bp of cuts seen ahead after today’s cut.

US TSYS: Late SOFR/Treasury Option Roundup: Leaning Hawkish

Heavier SOFR & Treasury option flow leaning hawkish prior to underlying futures near lows after reversing the initial rate-cut knee-jerk reaction, projected rate cut pricing cools slightly vs. early morning levels (*): Oct'25 at -22bp (-46.4bp), Dec'25 at -59.7bp (-69.1bp), Jan'26 at -72.4bp (-82.9bp).

- SOFR Options:

- 12,000 SFRX5 95.62/95.75 call spds, 1.0 vs. 96.325/0.05%

- +2,500 SFRH6 96.37 puts, 8.0 ref 96.60

- +20,000 SFRV5 96.50 calls, 2.25 vs. 96.345/0.20%

- Block/screen -100,000 0QZ5 97.00/97.25 call spds, 10.0

- +2,500 SFRZ5 96.00/96.18/96.50/96.75 call condors 12.5

- +10,000 2QZ5 96.75 puts, 7.0 ref 97.005

- +5,000 SFRH6 96.00/96.25 put spds 2.5 over 0QH6 96.50/96.75 put spds

- 3,000 0QZ5 97.25/2QZ5 97.18 call spds

- +10,000 SFRZ5 95.81/95.93/96.06 put flys, 0.75

- +2,000 SFRV5 96.37/96.50/96.62 call flys, 2.25

- Block, 5,000 2QX5 97.12/97.37/97.50 broken call flys, 4.75 net/splits

- +3,500 SFRF6 96.00/96.31/96.50 broken put flys, 2.75

- +4,000 SFRX5 96.00/96.06/96.12/96.18 put condors, 1.0

- 2,000 SFRZ5 96.43/96.56 1x2 call spds ref 96.36

- 1,800 0QX5 97.37/97.62/97.75 broken call flys ref 97.105

- over 6,300 SFRX5 96.18 puts ref 96.36

- 3,500 SFRF6 96.00/96.3196.50 broken put flys ref 96.615

- -4,200 0QV5 96.81 straddles, 31.0 ref 97.105

- +3,000 SFRZ5 95.93/96.06/96.18 put flys, 1.5

- +3,000 SFRZ5 95.93/96.06/96.18 2x3x1 put flys, 0.5 ref 96.355

- +5,000 SFRZ5 96.75/97.00 call spds, 1.25 ref 96.355

- +5,000 SFRZ5 96.25 puts, 6.5

- -3,500 0QV5 96.93 puts, 3.5

- Treasury Options:

- 3,000 TUX5 105 calls ref 104-12.88

- +30,000 Wed/wkly FV 110/110.25 call spds ref 109-27.25

- over +15,000 FVV5 109.5 puts, 7-8.5

- over 6,000 FVV5 108.75/111.25 strangles ref 109-27.75

- -2,000 wk1 TY 113.25 puts, 25 vs 113-18.5/0.40%

- +2,000 TYV5 112.5 puts, 5 vs. 113-16.5/0.10%

- +5,000 TYV5 113 puts, 11

- 3,000 wk3 US 119 calls, 9

- over 6,000 TYV5 112.5 puts, 5 last ref 113-19.5

- +2,000 wk3 FV 109.5 puts, 3.5

- +3,500 TYV5 114.25 calls, 9

- +4,000 TYX5 112.5 puts, 21

- +2,000 TYV5 114/114.5 call spds 7 vs. 113-16/0.16%

- over 6,500 wk3 TY 113 puts, 4 ref 113-19 to -19.5 (exp 9/19)