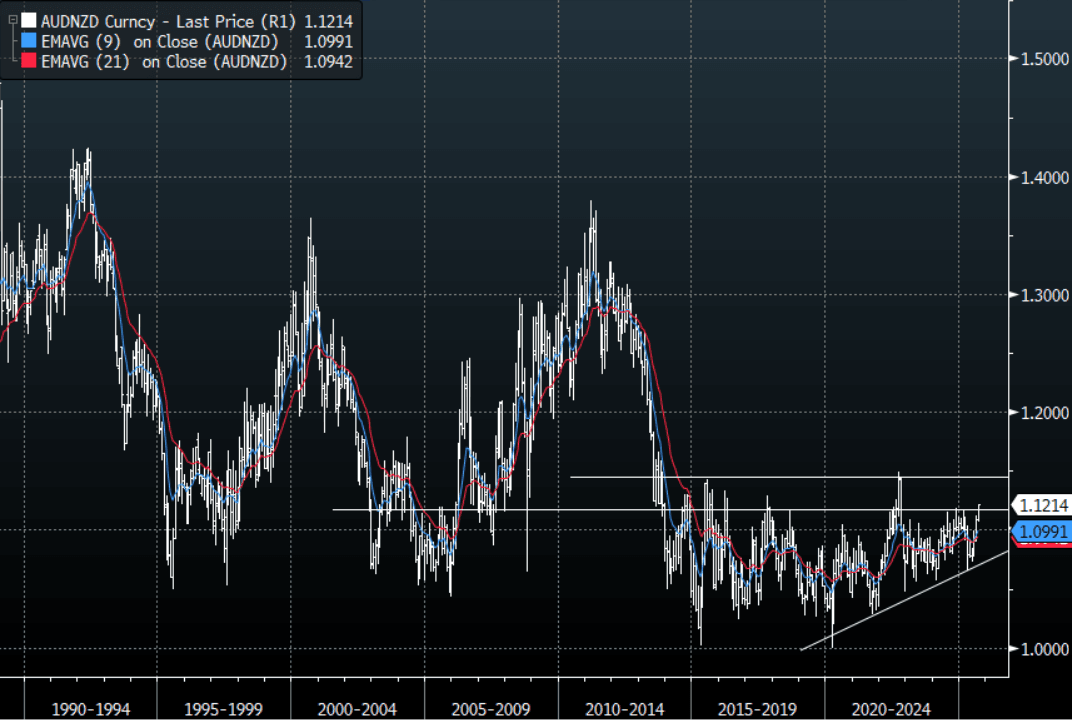

AUDNZD: The Cross Is Breaking Above 1.1200 On Poor NZ GDP, Is This The Start ?

The AUD/NZD is challenging some pivotal levels as it looks to build the momentum needed to break above what has been a decade long resistance. The very weak GDP data this morning points to very weak growth and increases the chance of larger rate cuts. This has given the cross the nudge it needed to break back above 1.1200 a level not seen since 2022, currently 1.1220(+0.62%). Australia Unemployment up next today which could also impact the price.

- The next target is back towards 1.1400/1.1500 a break of which would start to get bulls very excited about a potential new extended trend higher.

- The cross can become very crowded positionally very quickly hence the reversion back to the mean nature of the pairs price action, but dare I say it is starting to look constructive and the dips should now be supported.

- MNI AU: NZ Very Weak Growth Increases Chance Of Larger Rate Cut. Both the production and expenditure-based GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline. This and the broad-based softness across sectors as well as a sluggish recovery in Q3 to date are likely to drive 25bp rate cuts in October and November in line with the RBNZ’s August OCR path. With two votes for a 50bp cut in August, the risk of a larger move before year end is material.

Fig 1: AUD/NZD spot Monthly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RBNZ: MNI RBNZ Preview-August 2025: Rate Cut, Focus On OCR Path

- Download Full Report Here

- The RBNZ meets on Wednesday August 30 and is likely to cut rates 25bp to 3.0%, the mid-point of its estimated "neutral" range. While it paused at the July meeting, it was with a clear easing bias.

- With the cut widely forecast, attention will be on the revised RBNZ outlook and tone of the statement and press conference. The focus is likely to be on the projected OCR path and whether it is revised lower suggesting further easing towards stimulatory territory as excess capacity persists.

- With the focus on the medium-term, the 2026 and beyond inflation forecasts will be the important ones and should remain around the 2% band mid-point.

- RBNZ-dated OIS pricing is slightly firmer across meetings with 23bps of easing priced for tomorrow’s meeting, with a cumulative 41bps by November 2025.

US TSYS: Cash Open

TYU5 is trading 111-17+, up 0-01 from its close.

- The US 2-year yield opens around 3.76%.

- The US 10-year yield opens around 4.334%.

- (Bloomberg) - The air has started to seep out of the rate-cut-hope balloon, with a September cut now about 80% priced in. One more hot inflation (or consumer) print is all it will take to get us back to even odds, roiling bonds again. Deutsche Bank, for one, titled their recent note “Jury still out on September rate cut, but 50bps definitely out.”

- MNI US DATA: NY Fed Services Activity Sags As Sellers Hike Prices To Buoy Margins. The NY Fed's survey of regional services firms' business leaders showed a deterioration in activity and forward-looking sentiment in August, with inflation pressures remaining prevalent. The current general activity index fell for the first time since March, to -11.7 from -9.3 prior, with the business climate likewise worsening to -39.3 from -34.6. These are still better than the historically bad readings in April's survey amid heightened sensitivity to tariff-related news, but firmly negative by historical standards.

- Yields extended higher overnight, probing the pivotal resistance area within the greater 4.10%-4.65% range. The 4.35% area in 10-Year yields should still see demand initially, but the way the market keeps bouncing off levels just below 4.20% will be disconcerting for longs.

- Data/Events: Housing Starts, Building Permits

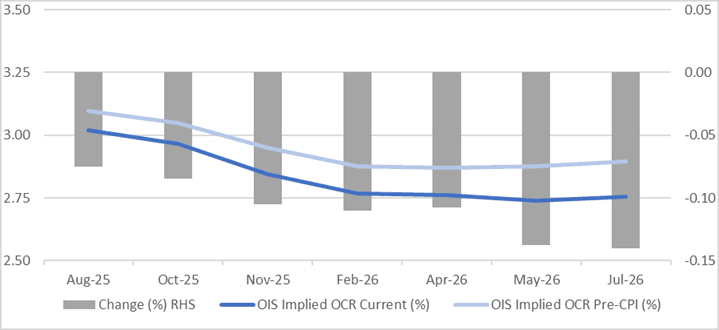

STIR: RBNZ-Dated OIS Softer Than Pre-CPI Levels Ahead Of RBNZ Decision

RBNZ-dated OIS pricing is slightly firmer across meetings ahead of tomorrow’s RBNZ Policy Decision.

- 23bps of easing is priced for tomorrow’s meeting, with a cumulative 41bps by November 2025.

- Notably, pricing is 8-14bps softer across meetings versus late July’s pre-CPI levels.

- NZ CPI rose less than economists expected in Q2. Headline CPI rose 0.5% q/q 2.7% y/y (estimate +0.6% and 2.8%). Tradeables rose 0.3% q/q, less than forecast, while non-tradeables were in line at 0.7% q/q.

Figure 1: RBNZ Dated OIS Current vs. Pre-CPI (%)

Source: Bloomberg Finance LP / MNI