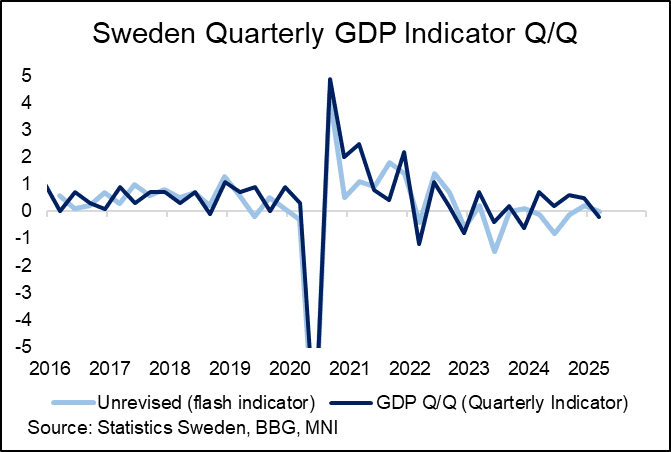

SCANDIS: Surprisingly Weak Swedish Q1 GDP

Surprisingly weak Swedish Q1 GDP print: -0.2% Q/Q versus a 0.0% flash print and 0.5% Riksbank March MPR projection. Last quarter’s reading was also revised down to 0.5% from 0.8% initial. All else equal, this is a dovish input ahead of the Riksbank’s June decision (markets price a ~50% implied probability of a cut). However, the impact is muted by the lagged nature of the data, and there’s no significant impact in Scandi FX crosses to note.

- The flash indicator hasn’t been a good predictor of actual GDP outcomes since the start of 2024, but errors since then had been correlated to underestimate the final read. Q1’s reading bucks this trend, overestimating GDP for the first time since Q4 2023.

- In Norway, NAV have restarted their seasonally adjusted registered unemployment series, after pausing it last month due to substantial data revisions/comparability issues. In May, registered unemployment was 2.1%, a tenth above March’s reading and Norges Bank’s March MPR projection. It doesn’t seem enough to shift sentiment ahead of the June decision though – expect the cautious and non-committal stance with respect to rate cuts to continue.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROPEAN INFLATION: France CPI/HICP Both Expected at 0.7%Y/Y

France April inflation is due at 07:45BST / 08:45CET today. Our full April Eurozone HICP preview is here. The release follows firmer-than-expected Spain data yesterday.

- BBG consensus:

- HICP 0.7% Y/Y (vs 0.9% prior), 0.4% M/M

- CPI 0.7% Y/Y (vs 0.8% prior), 0.4% M/M

- Analyst views:

- Goldman Sachs: 0.7% headline, 1.7% core (both HICP). “Services moving slightly lower on a year-over-year basis, with stronger airfares component offset by weaker package holidays and insurance (which we expect to grow by 1.1%mom nsa vs 3.6%mom nsa in April 2024)”.

- Morgan Stanley see “a relatively uneventful inflation print for France in April”, with core CPI/HICP at 1.6%/1.9% Y/Y. “This fundamentally reflects that inflation in France has landed, in line with negotiated wages, which have been below 3% since mid-2024. So, the focus is on small movements that might pull the print in one direction or the other”

- The April flash PMI noted “further easing of cost pressures, with input prices rising at the slowest pace in the year-to-date. At the same time, prices charged were discounted for the first time in three months, with company reports indicating that this was in response to fierce competition.”

BTP TECHS: (M5) Overbought But Remains Bullish

- RES 4: 121.93 76.4% of the Dec 5 ‘24 - Mar 14 bear leg (cont)

- RES 3: 121.43 1.618 proj of the Mar 14 - Apr 4 - 9 price swing

- RES 2: 121.00 High Feb 7 (cont) and a key resistance

- RES 1: 120.65 1.382 proj of the Mar 14 - Apr 4 - 9 price swing

- PRICE: 120.02 @ Close Apr 28

- SUP 1: 119.60/119.07 Low Apr 23 / 20-day EMA

- SUP 2: 117.28 Low Apr 10

- SUP 3: 116.06 Low Apr 9

- SUP 4: 115.75 Low Apr 14 and a bear trigger

A bull cycle in BTP futures remains intact and the contract is holding on to the bulk of its recent gains. The Apr 24 rally reinforces current bullish conditions. The move higher resulted in the break of key resistance at 120.39, the Feb 28 high. Sights are on 120.65 next, a Fibonacci projection. Firm support to watch lies at 119.07, the 20-day EMA. The contract is overbought, a pullback would unwind this trend condition.

MNI: GERMANY MARCH RETAIL SALES -0.2% M/M

- GERMANY MARCH RETAIL SALES -0.2% M/M