STIR: Still Uncertainty Around The Timing of The Next ECB Cut

ECB-dated OIS pricing remains consistent with one more 25bp cut this cycle, but there is still some uncertainty as to whether this cut will be delivered at the September or December macroeconomic projection meetings. Recall the MNI Policy Team’s post-Sintra forum sources piece, which said “officials are virtually unanimous that their June projections are so far being confirmed by incoming data, despite ongoing risks from global trade tensions, paving the way to a likely September cut, though some more cautious policymakers would prefer to wait until December”.

- US President Trump’s 30% tariff threat against the EU over the weekend hasn’t done much to change that narrative, with focus still on the outcome of negotiations between the two parties.

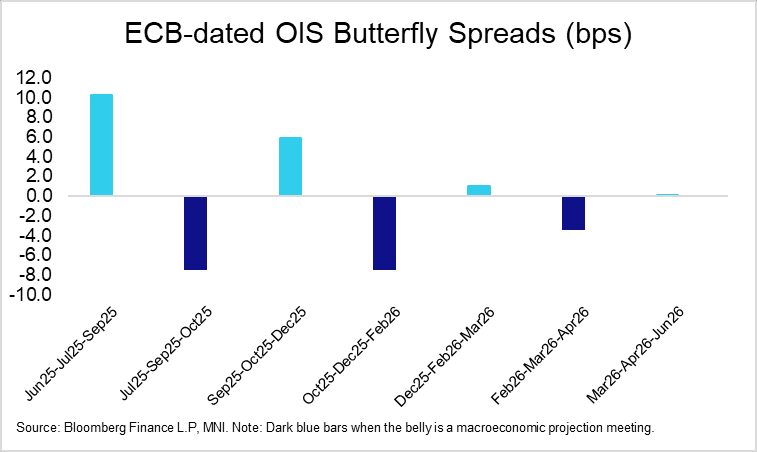

- OIS currently price virtually no implied probability of a cut at next week’s meeting. Meanwhile, there are 11bps of sequential cuts priced between July and September, 3bps between September and October, and 9bps between October and December.

- Interestingly, the curvature of the OIS curve around the two upcoming projection meetings is identical – butterfly spreads centred on the September and December projection meetings are both -7.4bps.

- Yesterday evening, ECB’s Nagel re-iterated his preference for a “steady hand” in setting rates, in line with previous comments and his hawkish leaning view.

- Today’s regional calendar includes final Italian June HICP and May Eurozone trade data. Wider focus will be on the US PPI report following yesterday’s CPI reading, which started to show some tariff impact in core goods categories.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Jul-25 | 1.921 | -0.2 |

| Sep-25 | 1.816 | -10.7 |

| Oct-25 | 1.785 | -13.8 |

| Dec-25 | 1.695 | -22.8 |

| Feb-26 | 1.679 | -24.4 |

| Mar-26 | 1.653 | -27.1 |

| Apr-26 | 1.660 | -26.3 |

| Jun-26 | 1.667 | -25.6 |

| Source: MNI/Bloomberg Finance L.P. | ||

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: ECB Implied Cuts Pared On Middle-East Inflation Risks

ECB-dated OIS price 21bps of easing through year-end, 3bps more hawkish than yesterday’s close. The inflationary risks stemming from continued Israeli/Iranian tensions over the weekend appear to have driven the move, while core FI is also pressured by the latest uptick in equity benchmarks. For the Eurozone inflation outlook and therefore the ECB reaction function, the most important risk to monitor is whether the latest escalation impacts actual global oil/gas supply or disrupts key shipping routes in the region. Overall, we think the ECB remains comfortable with current market pricing that implies a high chance of one more 25bp cut this cycle.

- Over the weekend, President Lagarde re-iterated that heightened dampens investment and that "we are within reach of the 2% medium-term inflation target" in an interview with Xinhua News Agency.

- Meanwhile, Vice President de Guindos told Reuters that “inflation is going in the right direction”. In particular, he noted that the “risk of [inflation] undershooting is very limited in my view”. This suggests he also views the risks of overshooting as similarly limited.

- De Guindos highlighted that trade policies are “by far the most relevant factor of uncertainty that we considered in our projections”. Speaking on the risk of disinflationary trade diversion, he stated, with a slightly more dovish tone that ECB’s Schnabel, that “I don’t know whether it’s going to be a big risk, but undoubtedly this is something that we have to monitor and take into consideration.”

- See above for commentary on Nagel’s latest, uncontroversial, remarks.

- Euribor futures are -2.0 to -4.0 ticks versus Friday’s settlement, with the greens/blues leading the selloff.

- ECB’s Cipollone is scheduled to speak today, while final Q1 Euro area labour costs won’t be too interesting to markets.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Jul-25 | 1.906 | -1.9 |

| Sep-25 | 1.799 | -12.7 |

| Oct-25 | 1.771 | -15.4 |

| Dec-25 | 1.712 | -21.3 |

| Feb-26 | 1.703 | -22.2 |

| Mar-26 | 1.688 | -23.7 |

| Apr-26 | 1.691 | -23.4 |

| Jun-26 | 1.696 | -22.9 |

| Source: MNI/Bloomberg Finance L.P. | ||

ECB: Nagel Sees ECB In "Very Good Position" To Respond To New Developments

At current interest rates, ECB's Nagel sees the Governing Council well positioned to react to any shocks threatening price stability, reiterating the ECB should remain data-dependent:

- "In my view, this interest rate level puts us in a very good position to respond to a wide range of developments."

- "The current price data and inflation forecasts signal that the mission has been accomplished. We in the Governing Council can be very satisfied with this. However, we cannot afford to sit back and relax. Rather, we must keep our eyes and ears open for risks to price stability."

- "Given that crucial factors can change rapidly in the current environment, we would be well advised to remain flexible. This means that it does not make sense to make any predetermined decisions – neither on a further interest rate cut nor on maintaining the status quo in monetary policy. We should continue to make decisions on a meeting-by-meeting basis depending on the data and not rush into anything."

- "I am confident that inflation will stabilize at 2 percent in the long term and that we will thus achieve our medium-term inflation target. [...] A sustained undershooting is unlikely. The underlying inflation and, above all, the increase in the cost of services are too high for that."

- "German fiscal policy is likely to dampen inflation noticeably in the short term when relief measures such as the reduction in electricity tax or grid fees come into effect. On the other hand, higher spending on defense and infrastructure could drive aggregate demand and, indirectly, consumer prices in the medium term."

Elsewhere, he remains within common themes re the economic outlook in Germany - but sees some upside vs Bundesbank's recent 2025 forecast:

- "According to our recent forecast for Germany, the economy will remain flat on average for the current year. However, this forecast did not take into account the fact that the revised growth rate for the first quarter is now twice as high as originally reported. A slight increase in overall economic performance therefore seems quite possible on an annual average."

- "Economic output is likely to stagnate in the second quarter. Exports are undoubtedly suffering from US tariff policy. In addition, industrial capacity utilization is comparatively low. Accordingly, companies have relatively little incentive to invest. Furthermore, private household consumption is currently subdued. This is because the labor market is tending to deteriorate and wages are no longer rising as strongly."

BUNDS: Extending losses Through support

- After clearing the 131.52 level, Bund is seeing a pick up in Volumes, sold in 5k through new lows.

- The Bid in Risk has been the early driver, although other Investors might look at Inflationary Risks through Commodity Markets (Oil).

- The main initial target is still eyed at the 2.60% level.

Today, reference 130.27:

- 2.60% = 130.05.