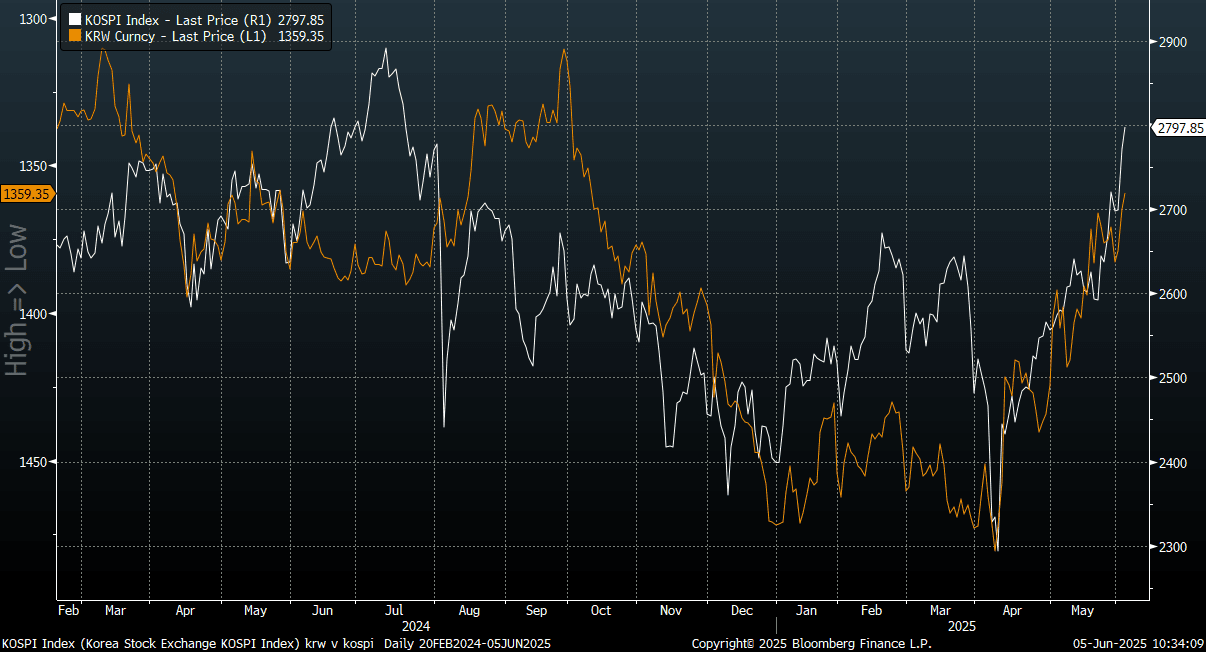

KRW: Spot USD/KRW Breaks Under 1360, Local Equity Surge Continues

Spot USD/KRW is testing lower in the first part of Thursday dealings. We were last under 1360, up close to 0.40% versus end Wednesday levels (session lows at 1358.15). This is also fresh YTD lows in the pair, with downside focus likely now on a test of the 1350 region. Onshore equities have opened up firmer, rallying close to 1% for the Kospi. We did have positive tech leads from US markets overnight, while optimism continues around new President Lee's policy agenda (he will hold his first cabinet meeting today).

- The chart below updates the Kospi versus USD/KRW spot trends. Note that USD/KRW spot is inverted on the chart.

- Earlier we had Q1 GDP revisions, with the q/q unchanged at -0.2%, but the y/y was revised to flat, versus -0.1% initially reported.

- Note our earlier data calendar had BoP figures also out today. This data comes out on June 10.

Fig 1: Kospi Versus Spot USD/KRW (Inverted)

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Pricing In Positive Outcomes

The ESM5 had an overnight range of 5655.25 - 5706.25, Asia is currently trading 5665. The market had another test above 5700 on the back of a stronger than expected ISM Services print, but could not hold onto these gains and closed weakly.

- “Ford shares fell after the automaker suspended its full-year guidance and said it expects to take a roughly $1.5 billion hit from US auto tariffs.”(per BBG)

- “Goldman expects a buy-the-dip opportunity in AI stocks after recent tech earnings beat expectations. While the firm’s US TMT AI Basket has sold off more than 20% in 2025, analysts predict sentiment will improve as economic data shows few signs of impact from tariffs.”(per BBG)

- The Stock market has seemed to price in a lot of positive scenarios. The reality still feels a little way off with tariffs still high and trade deals not yet finding a resolution. The market will need to start seeing some specifics on these deals this week to build on this bounce.

- The FOMC on Wednesday will be very important for markets, as traders start to align their views to be more inline with the Fed and have been reducing rate cut expectations. This implies the Fed Put for stocks to be a lot lower from the current market.

- The SPX has had a big bounce from its lows on 4800 handle, but we are approaching some key resistance between 5600-5800, the longer-term sellers should be active around here.

Fig 1: SPX Weekly Chart

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: AUCTION PREVIEW: ACGB Jun-54 Supply Due

The Australian Office of Financial Management (AOFM) will today sell A$300mn of the 4.75% 21 June 2054 Treasury Bond. The line was last sold on 24 March 2025 for A$300mn. The sale drew an average yield of 4.9874%, at a high yield of 4.9874% and was covered 2.7067x. There were 58 bidders, 30 of which were successful and 21 were allocated in full. The amount allotted at the highest yield as a percentage of the bid at that yield was 48.0%.

- This week's ACGB supply is larger than the recent average weekly issuance of $1500mn, with A$1000mn of the 3.75% 21 April 2037 bond also due on Wednesday and A$700mn of the 2.75% 21 November 2029 bond due on Friday.

- According to the Budget 2025-26 Issuance Program Update from the Australian Office of Financial Management (AOFM), total issuance of Treasury Bonds (including Green Treasury Bonds) in 2025-26 is expected to be around $150 billion. Issuance of Treasury Indexed Bonds by tender is expected to be between $2 billion and $3 billion (additional issuance by syndication may be considered).

- For 2024-25, issuance of Treasury Bonds has been revised to around $100 billion, including around $2 billion of Green Treasury Bonds. Treasury-Indexed Bond issuance will be around $3 billion.

- Results are due at 0200 BST / 1100 AEST.

LNG: Lower Demand Driving Gas Prices Down

In holiday-affected trading, European natural gas prices were flat on Monday at around EUR 33.08, close to the intraday high. They had traded in a narrow range through the session. Softer demand continues to weigh on prices with them down 21.7% in April but the fall has attracted Asian buyers. Soft manufacturing PMIs point to industrial usage remaining lacklustre or even deteriorating as US trade policy worries producers.

- Lower prices and a change in the weather as well as increased renewables-generated power have allowed the EU to begin refilling storage ahead of next winter and are now at over 40% although still below the 50% 5-year average.

- Bloomberg reported that the EU is about to present a plan to finish Russian gas imports by end-2027, but with increased supply expected by then the shift may have a limited impact on gas prices.

- US gas fell 1.7% to $3.57 after rising to $3.75 yesterday. In the near-term, the weather is expected to be mild but then warm up around mid-May, according to NatGasWeather, with the possibility of some cooling demand then.

- Yesterday lower-48 US production rose 4.6% y/y, while demand fell 4.1% y/y. The previous week EIA-reported US inventories returned to the 5-year average, according to Bloomberg.

- Flows at the US’ Freeport LNG facility have picked up again after power issues but one train remains offline at Cameron due to planned maintenance.