JGBS: Slightly Weaker But Off Session Worsts, Real Wages Fall Again

In Tokyo morning trade, JGB futures are weaker, -17 compared to settlement levels, but the session’s worst levels.

- MNI Brief: Japan’s inflation-adjusted real wages fell 1.4% y/y in September, marking the ninth consecutive month of decline after a 1.7% fall in August, preliminary data from the Ministry of Health, Labour and Welfare showed Thursday. The data highlight that nominal pay increases continue to lag inflation, leaving households squeezed by high living costs and adding pressure on the government to step up measures against rising prices.

- Cash US tsys are ~1bp richer in today’s Asia-Pac session after yesterday’s sell-off.

- Conservative Supreme Court justices Amy Coney Barrett, Neil Gorsuch, and Chief Justice John Roberts all appeared skeptical of President Donald Trump's reciprocal tariffs, during questions to Trump's lawyer during today's hearing. The implied probability of Trump winning the case has dropped to 20%, per Polymarket.

- “Japan Innovation Party co-leader Fumitake Fujita says a Bank of Japan move to raise interest rates would likely send a mixed message on policy as the government is calling for more investment in the private sector.” - BBG

- Cash JGBs are flat to 1bp cheaper across benchmarks, with the 10-year underperforming. The benchmark 10-year yield is at 1.675% versus the cycle high of 1.705%.

- Swap rates are flat to 2bps lower.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

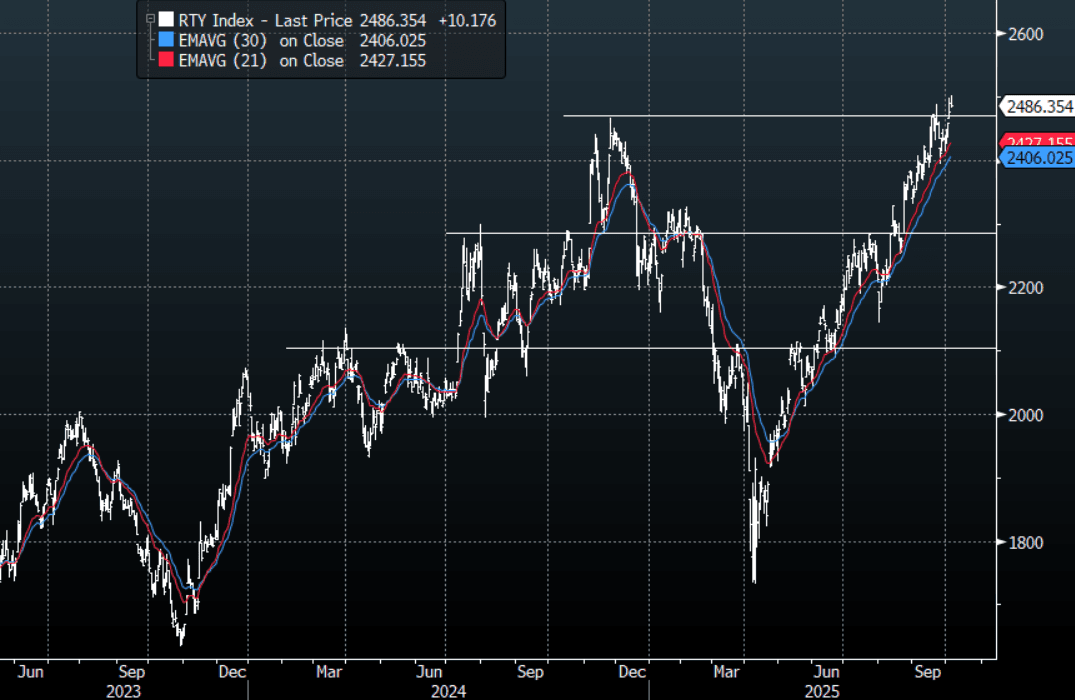

US STOCKS: Russell Index, Makes New All-Time Highs Tests 2500

The Russell 2000 overnight range was 2481.34 - 2501.91, closing +0.41%. The Russell 2000 found demand back towards 2400 and bounced nicely as the market reacted to benign US data last week. The Russell would be the biggest beneficiary of a new cutting cycle and is looking to regain topside momentum as it makes new all-time highs above 2500. CFTC data is not available but the price action suggests leveraged funds continue to pare back their large shorts.

- CNBC - “Paul Tudor Jones says the stage is set for a massive rally before the bull market reaches a “blow off” top. “All the ingredients are in place, and, certainly from a trading standpoint, you have to position yourself like it's October 1999.” Jones said in an interview with CNBC.

- MNI: Schmid Says Fed Must Maintain Credibility On Inflation. Kansas City Fed President Jeff Schmid said Monday that monetary policy must remain restrictive in the face of an inflation path that remains unacceptably elevated. "With inflation still too high, monetary policy should lean against demand growth to allow the space for supply to grow and relieve price pressures in the economy," Schmid said according to prepared remarks. "The current environment is one where aggressively boosting demand could raise the risk of an outsized increase in prices, as firms gain pricing power and increase the passthrough of tariffs to consumers.

Fig 1: Russell 2000 Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

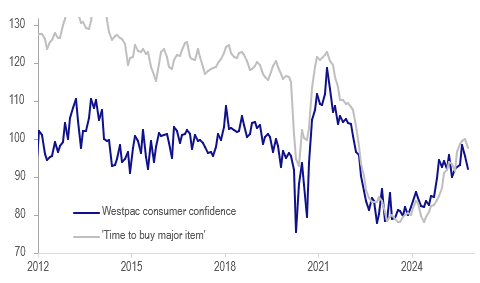

AUSTRALIA DATA: Stall In Disinflation Weighing On Consumer Confidence

Westpac consumer confidence fell for the second straight month in October as higher inflation prints appear to have weighed on assessments of family finances and the economy. Thus, Q3 CPI on 29 October is likely to be important for households too. The RBA’s decision to leave rates at 3.6% and cautious tone appear to have actually reassured consumers. Sentiment was down 3.5% m/m to 92.1, the lowest in 6 months. Households remain cautious but are prepared to spend at the right price. Q3 expenditure growth improved compared to Q2 with signs of a pickup in discretionary spending.

- The RBA noted in September that private consumption was stronger than it expected as financial conditions have eased and real incomes higher. Previously Deputy Governor Hauser noted that consumer confidence may be impacted by a “scarring effect” from the previous fall in real incomes. Quarterly consumption volumes in the September release on 3 November before the 4 November RBA decision will be monitored.

- Westpac expects a November rate cut but it states that it is “far from assured”.

- Westpac observed that responses following the RBA’s 30 September decision were around 2-3 points higher than prior. A bit more than half expected rates to rise over the coming year before the decision but that fell to about a third afterwards. Mortgage rate expectations over 12 months increased 15.6% to 101.7.

- Family finances over the next 12 months fell to 97.1, its lowest in just over a year. This sentiment appears to be impacting purchasing decisions with “time to buy a major item” down 1.1% to 97.2, well below the series average.

- Unemployment expectations fell 2.9% to be just below average signalling ongoing confidence in labour market stability.

- House price expectations continued rising in October up 2.1% with the over 75% of respondents expecting further increases over the year.

Australia Westpac consumer sentiment vs "time to buy"

Source: MNI - Market News/LSEG

JGBS: Slightly Cheaper Ahead Of 30Y Supply After Strong HH Spend

In Tokyo morning trade, JGB futures are weaker, -18 compared to settlement levels.

- Japan household spending for August was stronger than forecast (+2.3%y/y, versus 1.2% forecast, 1.4% prior). We are below earlier 2025 highs from a y/y momentum standpoint, but the trend has steadily improved from late 2024 lows. It should add, albeit at the margins, to the case for a further BoJ rate hike, although little is priced for the Oct meeting (implied rate of 0.52%, versus a current effective rate of 0.477%).

- On the political side, ahead of Takaichi's first formal actions in government, one of her primary policy advisers Honda stated that Takaichi wants the Bank of Japan to proceed "cautiously" on interest rates, and that an October rate hike is "difficult". While the comments appeared to pressure the Bank away from tightening policy, the view that a December hike is not a problem was notable.

- Cash US tsys are flat to 1bp cheaper, with a steepening bias, in today’s Asia-Pac session after yesterday’s modest sell-off.

- Cash JGBs are flat to 1.5bps cheaper across benchmarks. The benchmark 30-year yield is 1.4bps higher at 3.319% ahead of today’s supply.

- Swap rates are flat to 1bp lower, with swap spreads tighter.