AUSSIE BONDS: Slightly Richer After Today's Q2 Wages Data

Aug-13 02:59

ACGBs (YM +1.5 & XM +0.5) are slightly stronger after today’s wages data.

- The Q2 WPI rose 0.8% q/q leaving annual inflation at 3.4% y/y after a recent trough at 3.2% in Q4 2024 and 4.1% in Q2 2024. Public sector quarterly wage gains outpaced the private sector for the third consecutive quarter at 1.0% q/q compared with 0.8%. Public wage growth is now up 0.1pp to 3.7% y/y, while private was 3.4% y/y. The RBA had forecast 3.3% for Q2 and in its August projections is expecting the WPI to trend lower to around 3% by Q2 2026. 2025 to date is showing some stabilisation in wage inflation.

- Cash US tsys are slightly mixed, with a flattening bias, in today’s Asia-Pac session.

- Cash ACGBs are flat to 2bps richer with a steeper 3/10 curve and the AU-US 10-year yield differential at -5bps.

- Expectations of sustained strong pricing at auctions proved accurate, with the latest round of ACGB Dec-35 supply seeing the weighted average yield print 0.22bp through prevailing mids. Moreover, today’s cover ratio rose to 3.2417x from 2.6500x.

- The bills strip is +1 to +3.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in September is given a 41% probability, with a cumulative 40bps of easing priced by year-end.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: JPY Crosses - Soft Opening For Risk Sees Momentum Stall

Jul-14 02:51

This morning has seen US futures open under pressure with Trump issuing fresh 30% tariffs on Europe and Mexico starting Aug. 1, ESU5 -0.45%, NQU5 -0.45%. The market has most recently been able to look through these tariffs, is this just another dip to be added to or will their accumulation finally tell ? This soft opening for risk in Asia is giving the JPY longs some reprieve in the crosses.

- EUR/JPY - Friday night range 171.42 - 172.42, Asia is trading around 171.95. This pair looks to be consolidating after a powerful move higher, the baton is now being picked up in the other JPY crosses.

- GBP/JPY - Friday night 198.25 - 199.24, Asia trades around 198.50. The pair has failed initially towards the 199.00/200.00 resistance a break of which will see more JPY longs pared back. First support around 198.00 then the more important 196.50 area.

- NZD/JPY - Friday night range 88.26 - 88.62, Asia is currently dealing 88.10. NZD/JPY broke through the resistance around 88.00 but has failed to have really followed through. This morning's soft opening for risk has seen it give back most of Friday's gains. The Support towards 87.00/50 needs to hold for the focus to turn back to the 90.00/91.00 area.

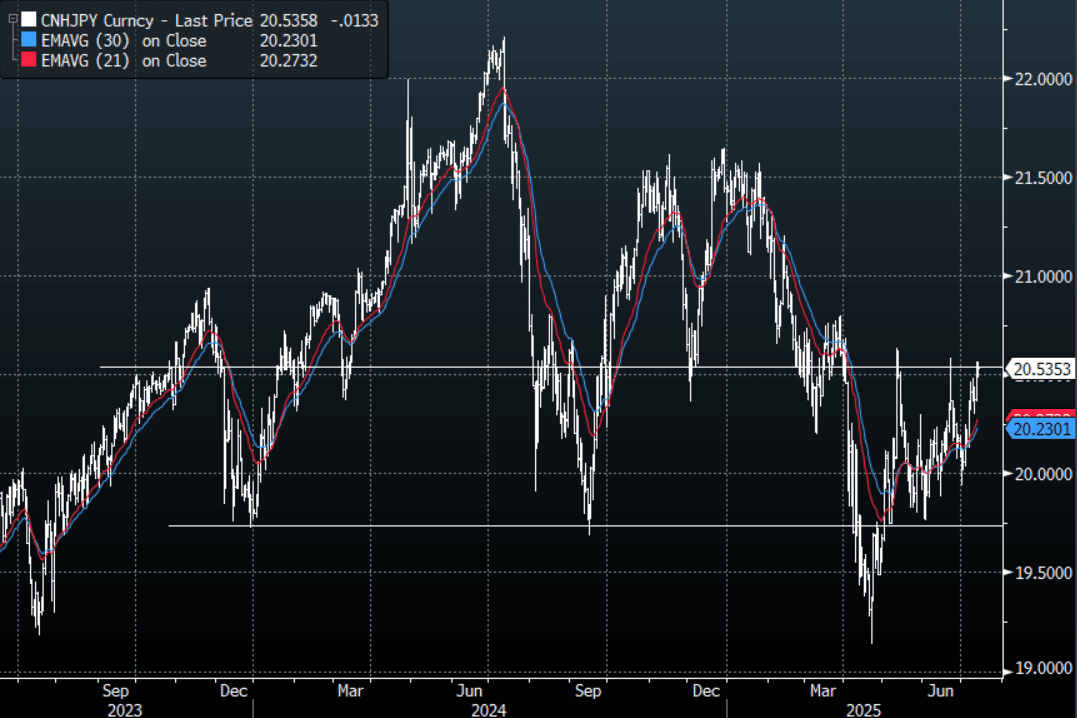

- CNH/JPY - Friday night range 20.4651 - 20.5676 Asia is currently trading around 20.5300. This pair is now back up towards the 20.50/20.60 resistance area, a sustained break back above 2.7000 will see more paring back of JPY longs.

Fig 1 : CNH/JPY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

MNI: CHINA H1 EXPORTS +7.2% Y/Y IN YUAN TERM: CUSTOMS

Jul-14 02:05

- CHINA H1 EXPORTS +7.2% Y/Y IN YUAN TERM: CUSTOMS

- CHINA H1 IMPORTS -2.7% Y/Y IN YUAN TERM: CUSTOMS

- CHINA H1 TRADE SURPLUS +CNY4.21 TRLN: MNI CAL

AUSSIE BONDS: Slightly Cheaper, Narrow Ranges On A Data-Light Session

Jul-14 01:52

ACGBs (YM -1.0 & XM -3.5) are slightly weaker on a data-light session. Ranges have been narrow.

- Cash US tsys are slightly mixed, with a steepening bias, in today’s Asia-Pac session after Friday’s bear-steepener.

- Cash ACGBs are 2-3bps cheaper with the AU-US 10-year yield differential at -5bps.

- The bills strip is slightly cheaper, with pricing -1 to -2.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in August is given an 88% probability, with a cumulative 59bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- “The Reserve Bank of Australia is set to start a fresh round of monetary easing in August, followed by further cuts in November, February 2026, and May 2026, Westpac said Friday.” (MTN via BBG)