EM CEEMEA CREDIT: SK Hynix: IPTs

(HYUELE; Baa2pos/BBBpos/BBBpos)

"IPT: SK Hynix $Benchmark; 3Y +115 Area, 5Y +120 Area" - BBG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NEW ZEALAND: Q2 Labour Data Expected To Be Weaker Than RBNZ May Forecasts

Q2 NZ labour market data is forecast to be weaker than the RBNZ assumed in its projections in May. Bloomberg consensus expects it to have softened in the quarter after some signs of stabilisation in Q1. The unemployment rate is forecast to rise 0.2pp to 5.3% more than the RBNZ’s 5.2% May projection. If the data print as weak as or weaker than consensus, then a rate cut on August 20 looks likely.

- Consensus is forecasting a 0.1% q/q drop in employment driving the annual rate down to -0.9% after -0.7% in Q1. This follows the monthly filled jobs data showing a contraction of 0.3% q/q in Q2. The RBNZ expected a rise of 0.2% q/q but looks likely to be disappointed as elevated uncertainty has weighed on hiring plans.

- Projections range from +0.2% q/q to -0.3% q/q leaving the annual rate between -0.6% and -1.0%. The domestic banks are generally more pessimistic than consensus with only ANZ in line. ASB, BNZ and Kiwibank expect employment to fall 0.2% q/q while Westpac is -0.3% q/q.

- Forecasts for the unemployment rate are between 5.1% and 5.3%. All of the domestic banks are in line with consensus at 5.3%, which would be the highest since Q4 2016. With a lacklustre economic recovery and job shedding, the unemployment rate could rise further by year end.

- The participation rate is expected to fall 0.1pp to 70.7%.

- Quarterly private wage growth may pick up to 0.5% q/q from 0.4% in Q1 but expectations are between 0.4% and 0.7%. ASB and Westpac are in line with consensus while BNZ and ANZ are higher at 0.6% and Kiwibank at 0.7%. Excess supply of labour is likely to put a cap on wage rises.

EUROZONE ISSUANCE: EGB Supply

Austria, Germany, Spain and France look to hold auctions this week. We pencil in issuance of E24.7bln, up from E17.2bln last week.

- Austria will kick off issuance for the week today with an RAGB auction, selling a combined E1.4375bln of the 2.90% Feb-33 RAGB (ISIN: AT0000A324S8) and the on-the-run 10-year 2.95% Feb-35 RAGB (ISIN: AT0000A3HU25).

- Germany will also hold an auction today with E5bln of the 1.90% Sep-27 Schatz (ISIN: DE000BU22106) on offer.

- Germany will return to the market tomorrow to hold a 15-year Bund auction. On offer will be E1.5bln of the 1.00% May-38 Bund (ISIN: DE0001102598) alongside E1.0bln of the 3.25% Jul-42 Bund (ISIN: DE0001135432).

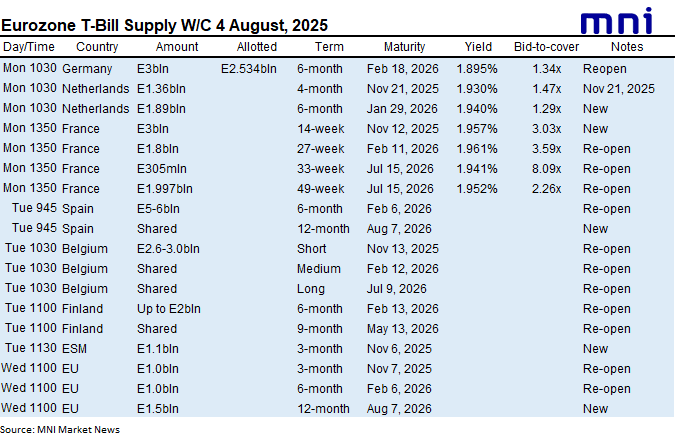

EUROZONE T-BILL ISSUANCE: W/C 4 August

Spain, Belgium, Finland and the ESM are due to sell bills today and the EU tomorrow while Germany, the Netherlands and France already came to the market yesterday. We expect issuance to be E28.2bln in first round operations, up from E14.2bln last week.

- This morning, Spain will look to sell 6-month Feb 6, 2026 letras alongside new 12-month Aug 7, 2026 letras. The auction size will be confirmed this afternoon.

- Belgian will then come to the market to sell a combined E2.6-3.0bln of the 3-month Nov 13, 2025 TC, the 6-month Feb 12, 2026 TC and the 11-month Jul 9, 2026 TC.

- Finland will look to sell up to a combined E2bln of the 6-month Feb 13, 2026 RFTB and the 9-month May 13, 2026 RFTB.

- The ESM will conclude today's bill issuance with up to E1.1bln of the new 3-month Nov 6, 2025 bills on offer.

- Tomorrow, the EU will bring the week's bill issuance to an end with up to E1.0bln of the 3-month Nov 7, 2025 EU-bill, up to E1.0bln of the 6-month Feb 6, 2026 EU-bill and up to E1.5bln of the new 12-month Aug 7, 2026 EU-bill on offer.