USDCAD TECHS: Sights Are On The Bear Trigger

- RES 4: 1.3920 High May 21

- RES 3: 1.3862 High May 29

- RES 2: 1.3798 High Jun 23

- RES 1: 1.3733/74 50-day EMA / High Jul 17

- PRICE: 1.3629 @ 16:06 BST Jul 24

- SUP 1: 1.3557 Low Jul 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

The trend needle in USDCAD continues to point south and a move down this week reinforces the bearish theme. Resistance at 1.3733, the 50-day EMA, remains intact for now. A clear break of this average is required to highlight a possible stronger short-term reversal. For bears, sights are on key support at 1.3540, the Jun 16 low. Clearance of this level would confirm a resumption of the downtrend.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Monitoring Resistance At The 50-Day EMA

- RES 4: 1.4111 High Apr 4

- RES 3: 1.4016 High May 12 and 13 and a key resistance

- RES 2: 1.3920 High May 21

- RES 1: 1.3825 50-day EMA

- PRICE: 1.3713 @ 16:51 BST Jun 24

- SUP 1: 1.3635 Low Jun 18

- SUP 2: 1.3540/3528 Low Jun 16 / 1.0% 10-dma envelope

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

A primary downtrend in USDCAD remains intact and recent gains appear corrective. Resistance at the 20-day EMA, at 1.3713, has been breached. A continuation higher would signal scope for a stronger retracement. Pivot resistance to monitor is at the 50-day EMA, at 1.3825. Key support and the bear trigger has been defined at 1.3540, the Jun 16 low. Clearance of this price point would resume the downtrend.

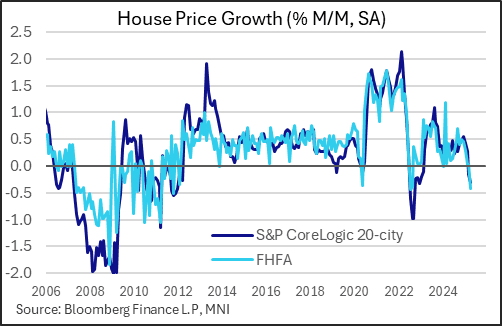

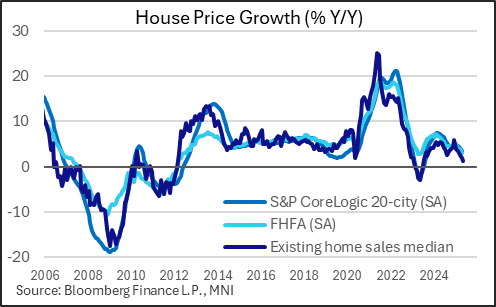

US DATA: House Prices Starting To Sag Amid Broader Market Weakness

The latest release of monthly house prices for April showed weakness is picking up, in something of a lag from poor sales activity and a nascent pickup in net supply.

- FHFA prices unexpectedly fell 0.4% M/M (SA), after 0.0% prior - the weakest monthly change since June 2022 (0.0% consensus). Meanwhile the S&P CoreLogic 20-City index showed a 0.31% M/M fall (-0.02% consensus, -0.16% prior) for the weakest print since December 2022.

- FHFA prices were up 3.0% Y/Y, slowest since May 2023, with the S&P 20-City's 3.4% the softest since August 2023.

- This is hardly a crisis for existing homeowners, with nominal prices up over 50% from pre-pandemic levels on both indices.

- But further weakness ahead looks likely - for example as we noted Monday, existing home inventory (1.54 million units, up 6.2%) now represents 4.6 months of sales, the most for any month since 2016, and prices appear to be rolling over.

- The overriding dynamic here is persistently high mortgage rates, which now appear to be coinciding with a loosening labor market that is starting to force some homeowners to sell, or at least consider their options.

US TSYS: Iran/Israel Ceasefire Holding, Fed Keeps Rate Cut Door Ajar

- US Treasuries look to finish at/near late Tuesday session highs - support twofold: risk sentiment improved as Israel/Iran hostilities appeared to de-escalate (ceasefire pledges watched closely after some morning confusion over timing).

- Secondary: Fed Chairman Powell's policy testimony to the House this morning - while maintaining patient stance regarding rate cuts, Chair Powell conceded he could see inflation not coming in "as strong as expected", however, "inflation is projected to have moved higher due to tariffs". Meanwhile, a "majority" feel it's appropriate to cut interest rates later this year.

- Projected rate cut pricing largely gaining vs. morning levels (*): Jul'25 at -4.7bp (-5.7bp), Sep'25 at -25.3bp (-24.2bp), Oct'25 at -41.2bp (-39.7bp), Dec'25 at -59.6bp (-56.6bp).

- On data, The Philly Fed non-manufacturing survey saw firms dial back particularly negative views on the regional economy to one closer to their own experiences. The Johnson Redbook retail sales index rose by 4.5% Y/Y in the week ending Jun 21, a slowdown from 5.2% the prior week and bringing month-to-date June sales gains to 4.8% Y/Y (vs a 5.7% gain targeted by retailers).

- Greenback weakness will likely have been bolstered by cleaner short-term positioning, weaker-than-expected US consumer confidence and Fed Chair Powell not ruling out the chance of an FOMC rate cut as soon as July.