FED: SF's Daly: Do Not Want To See Further Labor Market Softening

SF Fed President Daly's comments in Q&A suggest that she's not overly concerned about the labor market, but sees enough signs of potential weakness - and not enough signs of tariff-related inflation persistence - that she agrees with the general principle of cutting rates as "insurance".

- Asked whether she would consider the labor market "weak", Daly says: "I wouldn't really characterize the labor market as weak. The unemployment rate is low,... The people are finding jobs. Wage growth is still expanding at productivity plus inflation. So you have a sense that people are moving and doing things. But what is true is that it's not as speedy as it once was. So if you think three years ago, it was what we called frothy, then it got to healthy, then it got to solid. Now I'd say it's sustainable, but I do not want to see further softening. So one of the things that you see in the [September] rate cut is some insurance - you see the labor market has softened at a pretty good clip. it's come down rapidly from its highs, but the level of where it's sitting right now isn't weak. But you want to prevent that weakness, because we know, historically, once it tips into weakness, it's extremely hard to get it back out."

- Daly: "I don't see stagflation as around the corner. What I do see is that inflation has been printing above our target for quite a while, and that people have been enduring that sense that prices are rising. They're rising at a faster clip. When I get up in the morning, I still have to think about price increases, and we have work to do there on the labor side... I'd see that's an economy that still needs monetary policy, you know, bridling, but not as much as we had. But it's not something that I see as faltering and recession risk... recession risk is very low right now... Stagflation is a very different thing."

- Daly doesn't sound concerned about persistent tariff impacts on inflation: "We haven't seen tariffs [impact] in any sector other than the directly tariffed sectors like goods, and only the tariff parts of that. And then in services, you haven't seen it gone up. And in housing, where they have many, many inputs that are tariffed, you haven't seen the cost of housing rise rapidly. In fact, shelter inflation has been coming down, not going up. So that's, I think, evidence so far that's consistent with tariffs being a one time thing... we're seeing that if you look at the announced tariffs ... they have not come into consumer prices because ... firms take them along the supply chain, and everybody shares a little bit of that, or spreads it out over a longer period."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

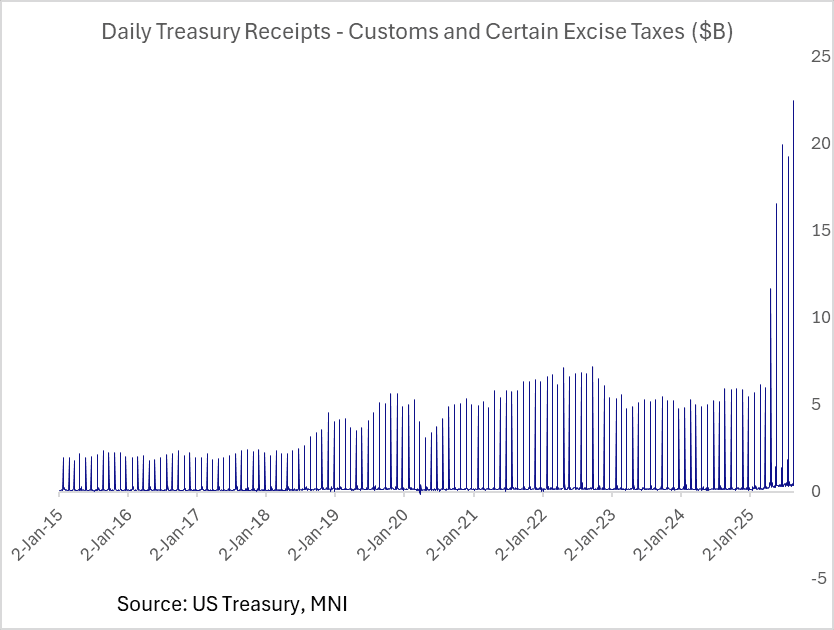

US FISCAL: August Tariff Revenues Headed For Fresh Monthly Record

The latest Treasury Daily Statement shows a single-day record $22.5B in customs revenue on August 22. This is the biggest tariff collection day of the month, when most corporates typically submit their payments, and exceeds the previous daily record of $19.9B set on June 24.

- That brings the total for August so far up to $29.6B, which is exactly the total collected in the full month of July. That sets it up to be a fresh record, on track to reach $32-33B for the full month of August.

- The rising figures are consistent with higher tariff rates being collected across a wider range of geographies, with the ramp-up starting in April following "Liberation Day".

- The Congressional Budget Office estimates that tariffs will total around $200B in the current fiscal year (Oct-Sep). With $181B collected so far with about 5 weeks to go, that estimate looks as though it will be exceeded.

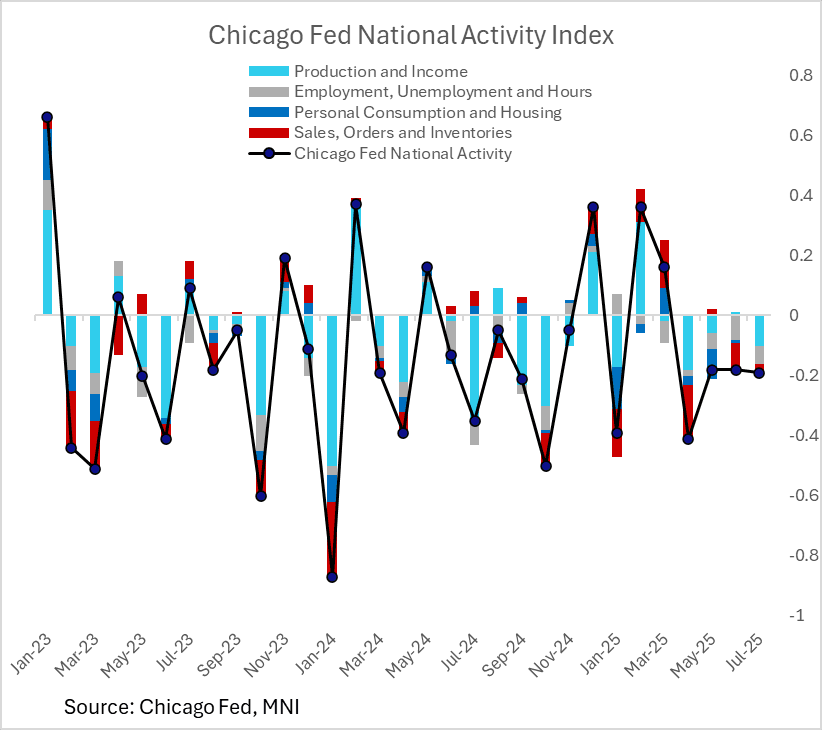

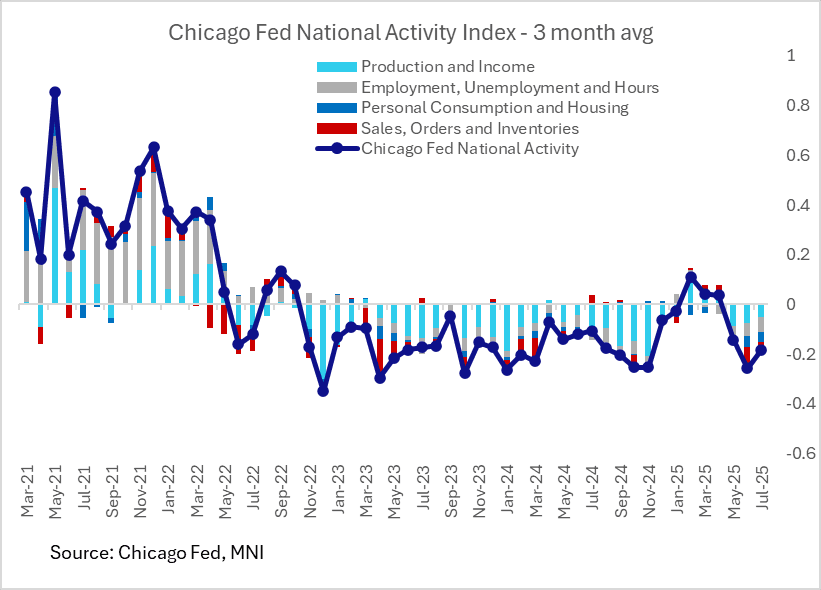

US DATA: Chicago Fed National Activity Index Implies Reversion To Sub-Par Growth

The Chicago Fed National Activity Index (CFNAI) edged lower to -0.19 in July from -0.18 in June, marking the 4th consecutive decrease in the index suggesting weakening activity.

- After spending 3 months in positive territory from Feb-Apr, the 3-month moving average has reverted to its usual negative territory over the last 3 months. Prior to this brief positive period, the 3-month average hadn't been above zero since late 2022.

- Changes in this index haven't been particularly well correlated with month-to-month or even quarter-to-quarter GDP growth per se (growth has been positive in almost all of the 3-month periods that the CFNAI has averaged negative).

- That said, the index and GDP growth look fairly similar over multi-quarter horizons, and a negative reading doesn't imply contraction, but rather below-average growth.

- In this regard it suggests that a spike in domestic demand/activity in H1 amid tariff front-loading has run its course with the economy starting to slow in H2.

FED: Dallas's Logan: More Room To Go On Reducing Reserves

Two takeaways from Dallas Fed President Logan's speech on central bank balance sheet policy Monday (which didn't include anything on current monetary policy):

- First, the ex-SOMA manager sees "more room to reduce reserves". While acknowledging what was already in the July FOMC meeting minutes about seeing "some temporary pressure around the tax date and quarter-end in September", Logan says she anticipates market participants will use the standing repo facility if necessary in September. "That will allow us to continue gradually bringing reserves to a more efficient level with market rates close to, but perhaps slightly below, interest on reserves on average over time." This sounds like she is not concerned with the ongoing reduction of reserves warranting a shift in Fed policy in the coming months.

- On this front, she again advocates for further development of so-called "ceiling" tools: "while we have made strides in enhancing the effectiveness of the discount window and Standing Repo Facility, it would be worthwhile to consider further steps, such as increasing or removing limits on the SRF’s size or centrally clearing those transactions."

- Second, she suggests that the Fed could shift to overweighting Treasury bills in its portfolio, over time: "it makes sense for the FOMC to hold primarily Treasuries in the long run, as we’ve repeatedly said we intend to do" and suggests that the Fed could in the long run "make its asset purchases proportional to Treasury issuance. In the medium term, overweighting Treasury bills in our purchases could more expeditiously move our current mix of holdings closer to matching the market."

- However, "the FOMC has made no decisions on the long-run composition of its Treasury holdings, and I look forward to continuing to discuss this topic with my colleagues" - as such this doesn't appear to be an imminent prospect.

- This adds another key update to current FOMC views on balance sheet composition. In June Gov Waller (a possible next Fed chair) concluded in a lengthy speech on the topic: "Though the FOMC has not finalized its desired efficient and effective size and composition of the balance sheet, it seems apparent that today's portfolio should be adjusted. And there are obvious steps to take. We are reducing the size of the balance sheet slowly and need to consider shifting it toward more bills."