US DATA: Services PMI Solidity Continues To Contrast With ISM Weakness

Oct-03 15:58

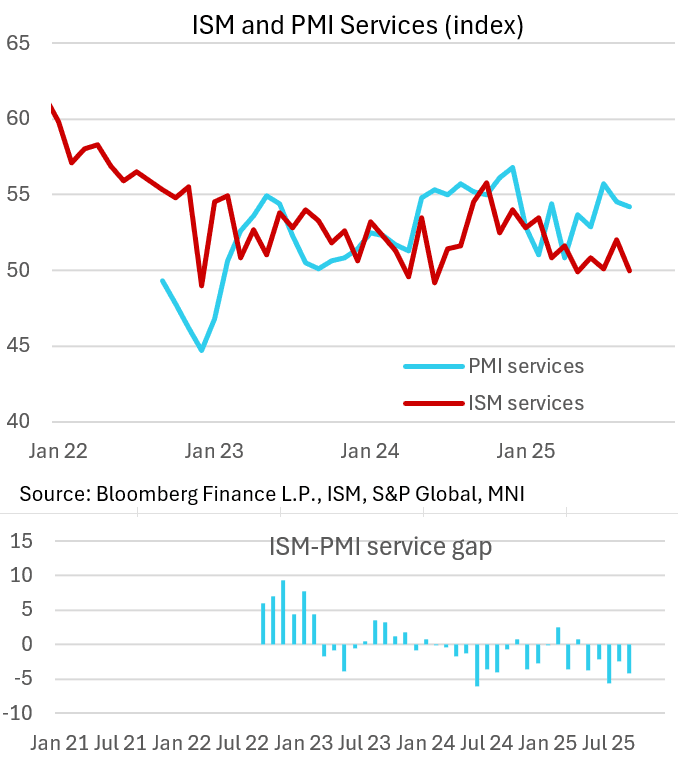

The final S&P Global US Services PMI was revised up 0.3 points from the flash estimate, at 54.2. That's a slightly smaller slowdown than previously estimated vs August's 54.4, and showed much stronger services sector activity than the ISM Services indicator (which fell to 50.0 vs 51.7 expected, 52.0 prior).

- From the S&P Global Services report: "Slower growth was linked to a softer expansion of new work, despite an improvement in foreign demand for the first time in six months. Meanwhile, sentiment regarding the outlook strengthened, linked in some instances by firms to lower interest rates. However, hiring activity increased only marginally amid some reluctance to replace leavers. On the price front, cost pressures remained elevated, driven principally by tariffs and higher salary payments. In response, service providers raised their own selling prices but at the slowest rate for five months."

- Bloomberg reported that the Services employment index fell to 50.4 vs 52.0 in August, which while the 7th consecutive month of expansion was also the lowest since April. Alongside a continued ISM Services contraction (albeit a M/M tickup) in this category, it suggests limited hiring impetus in the sector.

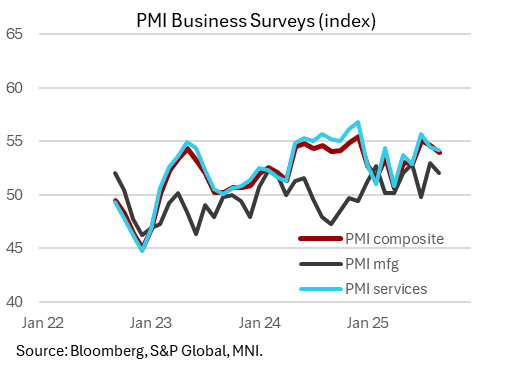

- Indeed when taking Manufacturing into account, "Both sectors covered by the survey recorded weaker output expansions in line with slower gains in new business. Employment meanwhile barely rose, but confidence in the outlook strengthened noticeably. Cost pressures remained elevated, although inflation softened to a five-month low. A similar trend was seen for output charges."

- Overall the Composite PMI fell to 53.9 in the final (slightly higher than the 53.6 flash) for a 3-month low (54.6 prior).

- Mirroring various GDP nowcasts, "over the third quarter, average monthly growth was the best recorded over a calendar quarter in 2025 so far", though "the index has now fallen for two months in a row, representing a slowdown from July’s year-to-date peak."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SECURITY: Trump To Speak w/Zelenskyy And Euro Leaders After Ukraine Summit Thurs

Sep-03 15:57

The Elysee confirmed that French President Emmanuel Macron, Ukrainian President Volodymyr Zelenskyy and ‘several other heads of state’ will speak with President Donald Trump at 08:00 ET 13:00 BST tomorrow, after a meeting of the ‘Coalition of the Willing’ in Paris.

- Trump said alongside Polish President Karol Nawrocki in the Oval Office that roughly 10,000 US soldiers will remain deployed in Poland, adding that number could be increased "if they want".

- Zelenskyy confirmed a short time ago that he discussed a US backstop to security guarantees w/EU counterparts in Copenhagen today: “We have signals from the US of a possible backstop [and] the role of EU membership in this holistic system of security guarantees...”

- Trump reiterated to reporters yesterday that there will be “consequences” for Putin slow-walking a meeting with Zelenskyy. He added: “I had actually a very good meeting with [Putin] a couple of weeks ago. We'll see if anything comes out of it. If it doesn't, we'll take a different stance.”

- It is unlikely Putin's recent concessions on a meeting will be seen by the White House as sufficient progress. See SECURITY: Putin Offers To Meet Zelenskyy And Trump In Moscow

- Treasury Secretary Scott Bessent told Fox on Monday that “all options are on the table” for further sanctions on Russia, adding “we’ll be examining those very closely this week.”

- Bessent and White House officials said EU countries need to align with the US on halting Russian oil purchases, but have equivocated on pursuing a similar secondary oil tariff on China to the one imposed on India.

- US Ambassador to NATO, Matthew Whitaker, told Bloomberg yesterday that the US has refrained from imposing secondary sanctions on China because of ongoing trade negotiations.

EGB SYNDICATION: Lithuania Long 10 / 20-year LITHUN: Priced

Sep-03 15:53

Long 10-year:

- Reoffer: 99.698 to yield 3.662%

- Spread set at MS + 95bp (Guidance was MS+105bp area and revised to MS + 95-100bp (WPIR))

- Size: E1.0bln (in line with MNI estimate)

- Books closed in excess of E1.9bln (ex JLM interest)

- Maturity: 10 March 2036

- Coupon: 3.625%, Short first

- HR 100% vs 2.60% Aug-35 Bund. Spot ref 98.76 / + 91.9bp

- ISIN: XS3175946071

20-year:

- Spread set earlier at MS +140bp (guidance was MS+145bp area)

- Size: E750mln (MNI pencilled in E1bln)

- Books closed in excess of E1.6bln (ex JLM interest)

- Maturity: 10 September 2045

- Coupon: 4.25%

- HR 99% vs 2.50% July-44 Bund. Spot ref 90.23 / + 116.5bp

- ISIN: XS3175947046

For both:

- Bookrunners: Erste Group (B&D), HSBC and Societe Generale

- Settlement Date: 10 September 2025 (T+5)

- Timing: TOE: 16:24 BST /17:24 CET. FTT immediately.

From market source / MNI colour

US TSYS: Poised to Extend Session Highs

Sep-03 15:47

- Treasury futures are poised to extend session highs ahead midday - mirroring German Bunds ahead into the European close.

- Currently, the Dec'25 10Y contract trades 112-18.5 (+14) vs. 112-19 high, 10Y yield -.0446 at 4.2168, curves remain flatter: 2s10s -1.370 at 60.643, 5s30s -2.137 at 121.475.

- THe Dec'25 10Y contract is nearing initial technical resistance at 112-20.5 (Aug 28 / 29 highs. A breach of this hurdle confirms a resumption of the current bull cycle and signals scope for an extension towards the 113-00 handle.