LNG: Second Wilhelmshaven FSRU to Start Aug. 29: Platts

Deutsche Energy Terminal (DET) will start commercial operations at its second floating LNG import facility in Wilhelmshaven on Ag. 29, following full commissioning of the Excelsior FSRU Platts said.

- The vessel has so far received 790,000 mt of LNG from the US. It will feed up to 1.9 Bcm of gas into Germany’s grid in 2025, increasing to 4.6 Bcm annually from 2027.

- The project, delivered in about half the usual time for large LNG terminals, is seen as a key step towards energy supply security, diversification and resilience.

- Wilhelmshaven’s first FSRU, the Hoegh Esperanza, began operations in December 2022, receiving 1.28m mt so far in 2025.

- With Excelsior, Germany now has four operational FSRUs.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Early SOFR/Treasury Option Roundup: Shift (Mostly) to Calls Ahead PPI

With few exceptions, SOFR & Treasury options saw better call volumes overnight, couple larger SOFR trades on otherwise limited volumes. Treasury highlight buyer of over 47,000 Sep'25 10Y put spds (block/screen). Underlying futures firmer with focus on June PPI data this morning. Projected rate cut pricing holds steady vs late Tuesday (*) levels: Jul'25 at -0.6bp, Sep'25 at -14.2bp, Oct'25 at -27.1bp, Dec'25 at -43.7bp.

- SOFR Options:

- 1,500 SFRZ5 95.62/95.75/95.87 put flys, ref 96.08

- -19,750 SFRQ5 95.68/95.75 put spds 1.25 ref 95.815

- Block/screen, +20,000 SFRH6 96.37/96.50 call spds vs. 96.00/96.12 put spds, 0.5 net vs. 96.31/0.15%

- 1,000 SFRU5 95.68/95.75/95.872x3x1 broken put flys ref 95.815

- Treasury Options:

- +5,000 TYU5 113/115 1x2 call spds, 2 vs. 110-12.5/0.05%

- -2,500 TUU5 103.25 puts, 5.5

- +15,000 TYU5 115 calls, 3

- +10,000 TYU5 115.5 calls, 3

- +5,000 TYU5 108/109 put spds, 11

- Block/screen over +47,000 TYU5 108.5/109.5 put spds 16 vs. 110-10/0.15%

- 2,500 TUU5 103.12/103.37/103.5/103.62 broken put condors, 0.5 net ref 103-17.12

- -3,000 TYQ5 109.75/110.75 call over risk reversals, 0.0

- 4,300 TYV5 111/112 call spds ref 110-08

- 4,250 TYQ5 110.5 calls ref 110-12

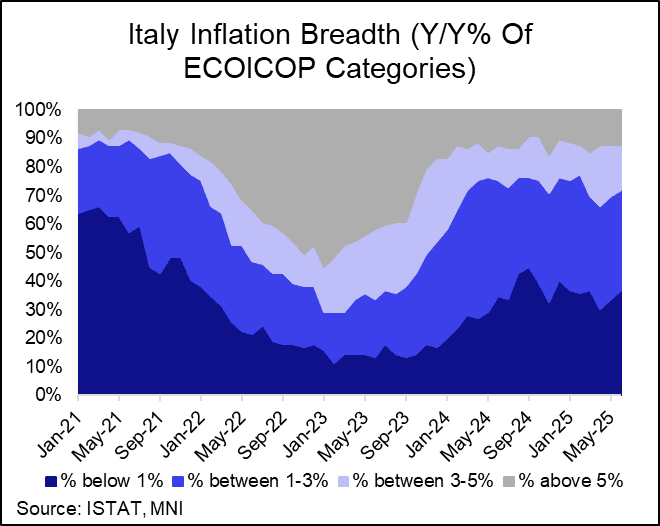

EUROPEAN INFLATION: Energy Drives Upward Revision To Italian June HICP

Italian final June HICP was revised up a tenth on a rounded basis to 1.8% Y/Y (vs 1.7% in May). Energy inflation was revised up three tenths to -2.1% Y/Y (vs -1.9% in May), while services was revised up a tenth to 3.0% Y/Y (vs 2.9% in May). This was mostly offset by a three tenth downward revision to processed food inflation to 2.8% Y/Y (vs 2.8% in May). Non-energy industrial goods was unrevised at 0.5% Y/Y (vs 0.4% in May), as was unprocessed foods at 4.5% Y/Y (vs 3.9% in May).

- Within services, there were accelerations in the restaurant and hotels, recreation and culture and transport services components.

- Package holidays rose 7.5% Y/Y (vs 6.3% prior), which was partially offset by a pullback in recreation and cultural services inflation (5.5% Y/Y vs 6.6% prior).

- Airfares inflation decelerated to 2.9% Y/Y (vs 4.6% prior). Although airfares rose 9% M/M on an NSA sequential basis in June, this was below last year’s reading and also some of the analyst expectations we had seen. As such, the rise in transport services was due to non-airfare (i.e. less volatile) components.

- Communication services were 0.5% Y/Y (vs 0.6% prior), while miscellaneous services were steady at 1.9% Y/Y. A pullback in insurance inflation was offset by a rise in personal care.

- Core goods inflation trends remain subdued – as is also seen in the broader Eurozone basket. In June, there was a small uptick in clothing and household appliance inflation, offset by a pullback in household textiles.

- The proportion of HICP sub-components with inflation rates between 1-3% Y/Y was steady at 35% (vs 36% prior).

FOREX: GBP Consolidating Most Recent Weakness, UK Labour Market Data Thursday

- This morning’s higher-than-expected UK CPI readings have been shrugged off by the pound, as markets await labour market data on Thursday and assess the ongoing fiscal concerns for the UK economy. GBPUSD’s post data advance was contained to a 20 pip rally to 1.3417 before then oscillating either side of 1.3400.

- Technical considerations are likely helping cable consolidate its most recent weakness. Following a clean break of the 50-day EMA, spot subsequently breached important trendline support (drawn from the Jan 13 low) below 1.3430 yesterday, which has helped cap the topside today. Developments strengthen a bearish threat, and the next immediate focus is on 1.3371, the Jun 23 low and a key short-term support. Below here, attention will be on 1.3335 and 1.3245, the May 20 & 19 lows respectively.

- In similar vein, a bullish condition in EURGBP remains intact and fresh 3-month highs this week maintain the price sequence of higher highs and higher lows, highlighting a dominant uptrend. Scope is seen for a climb towards key resistance at 0.8738, the Apr 11 high.

- Tomorrow’s labour market data takes on increased significance following BoE's Bailey flagging the MPC's potential responsiveness to further jobs declines in his interview with The Times this weekend. We previewed the data fully here: https://mni.marketnews.com/4eQADLZ