EM CEEMEA CREDIT: SASOL: Profit warning, no surprise

Feb-05 08:27

SASOL (SASOL: Ba1/BB+/-)

Profit warning, not surprising

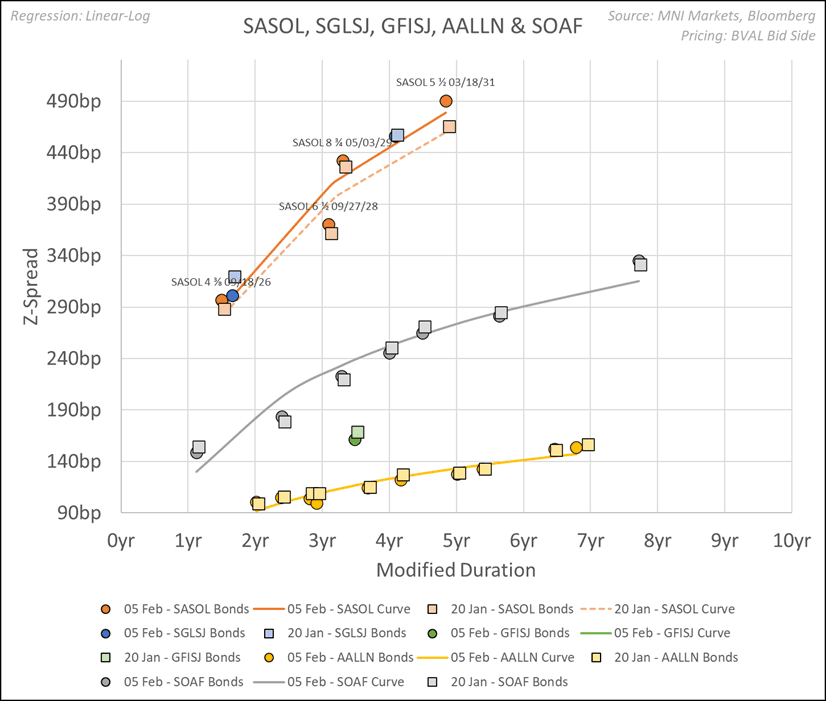

- SASOL 5.5 31 bonds have widened almost 30bp in z-spread (see chart below), following production update on 23rd Jan 25, while peers are broadly charting unchanged to marginally tighter, along with the sovereign curve.

- SASOL guiding for Adj-EBITDA for H1 24/25 of ZAR22-25bn compared to ZAR28 for same period last year. Not completely unexpected given that the co. reported disappointing production update in late January.

- A combination of issues resulted in weak volumes in H124/25, with on going coal quality issues and unrest in Mozambique resulting in lower gas volumes. Weaker QoQ chemical prices in Q2 also weighed on profitability. No further details were given for production into H124/25.

- Cash flow generation will be under pressure, for H124/25 and we expect FCF to be negligible. SASOL has limited near term debt maturities, and plenty of liquidity with ZAR15.6bn in cash & equivalents at the end of June 24.

- Sasol’s ratings were reviewed in Oct 24 by S&P and Moody’s so we don’t any rating action from these results, but if disruptions continue and FFO to debt falls below 30% then the co.’s outlook could change, probably closer to when the co reports full year results.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CROSS ASSET: EUR extends gains post Spanish PMIs

Jan-06 08:21

- A good beat from Spain, but no real impact in Bund, with desks likely more focussed on the German CPIs.

- The EURUSD has extended higher, but the initial push higher was more a function of the Dollar, as its tests broader lows against the GBP, CZK, PLN, MXN, SGD, CHF, ZAR, SEK and NOK.

MNI: SPAIN DEC SRVCS PMI 57.3 (FCAST 54.1); NOV 53.1

Jan-06 08:15

- MNI: SPAIN DEC SRVCS PMI 57.3 (FCAST 54.1); NOV 53.1

STIR: A Little Over 100bp Of ECB Cuts Priced For '25

Jan-06 08:13

Weakness in the long end has triggered hawkish repricing in EUR STIRs during early ’25, leaving ~103bp of easing priced through Dec vs. ~105bp late Friday and 115-120bp seen ahead of the Christmas break.

- Euribor futures 2.0 to 4.0 lower.

- ERZ5 ~10 ticks off its early November low.

- Services PMI data (final for Germany, France & the Eurozone) is due today, as is the flash German CPI data.

- Preliminary Eurozone CPI data is due tomorrow. The BBG survey median looks for +2.4% Y/Y for the headline CPI release vs. +2.2% in Nov.

- Our full preview of that release can be found here.

ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

Jan-25 | 2.654 | -26.5 |

Mar-25 | 2.375 | -54.4 |

Apr-25 | 2.178 | -74.1 |

Jun-25 | 2.046 | -87.3 |

Jul-25 | 1.999 | -92.0 |

Sep-25 | 1.936 | -98.3 |

Oct-25 | 1.905 | -101.4 |

Dec-25 | 1.888 | -103.1 |

Related bullets

Related by topic

SASOL

South Africa

Africa

EU Basic Industries

Credit Sector