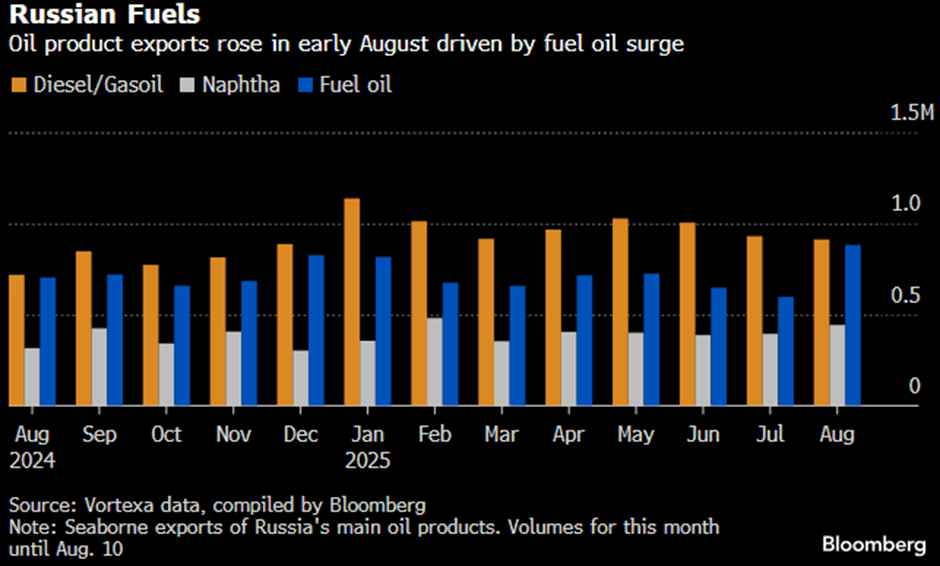

OIL PRODUCTS: Russia’s Fuel Oil Exports Hit Wartime High

Russia’s Petroleum product exports increased in early August despite intensified Ukrainian drone strikes on the country’s refineries, led by a surge in fuel oil outflows to the highest level since the war in Ukraine began, Bloomberg said.

- Total refined product exports climbed to 2.31m b/d over Aug. 1-10, the highest since February and up 9% on July.

- Drone strikes have intensified ahead of the Trump-Putin summit, causing oil processing rates to drop sharply.

- The jump in fuel oil shipments helped offset diesel flows that declined to the lowest level in 2025, while gasoline exports have been banned until the end of August.

- Fuel oil flows are up 48% on the month to 882k b/d, the highest since Feb. 2022.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: BLOCK: Dec'25 SOFR Call Condor

- 10,000 SFRZ5 96.25/96.50/96.75/97.00 call condors, 4.0 net ref 96.125 at 0857:04ET

SOFR OPTIONS: Effective Fed Funds Rate

- FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $104B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $261B

- Earlier Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.33% (+0.02), volume: $2.759T

- Broad General Collateral Rate (BGCR): 4.32% (+0.02), volume: $1.125T

- Tri-Party General Collateral Rate (TCR): 4.32% (+0.02), volume: $1.094T

- (rate, volume levels reflect prior session)

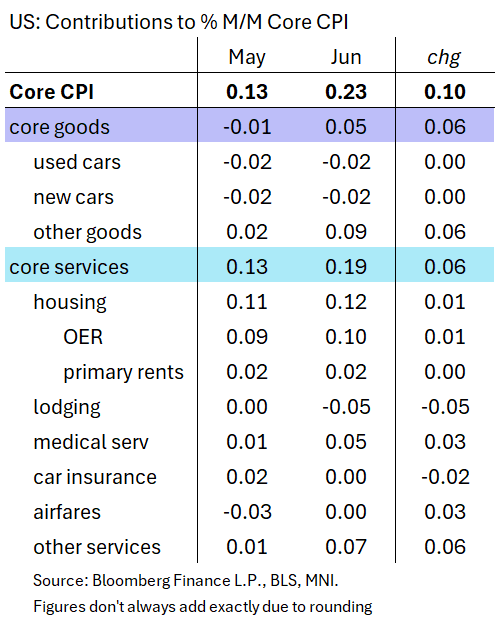

US DATA: Core Goods Pickup Unusually Driven By Ex-Vehicles In Tariff Sign

The 0.1pp pickup in core CPI M/M to 0.23% from 0.13% was basically equally split between core goods and services: note that vehicle price inflation didn't really make much of a sequential contribution difference (subtracting around 0.02pp to core CPI each, with used -0.7% after -0.5% and new -0.3% for a 2nd month). The standout was "other goods", ie ex-vehicle goods, raising their contribution to 0.09pp from 0.02pp prior. See table below though also note slight differences in aggregates due to rounding.

- That's the biggest such contribution since June 2022 in what is arguably the clearest sign yet that tariffs are beginning to seep through into CPI.

- For example, apparel accelerated to 0.43% M/M (-0.42% prior), contributing 0.01pp to CPI, most in 4 months. But there were multiple other core goods areas that are seen sensitive to inflation that saw acceleration, including recreation commodities (0.77% from 0.41%) and household furnishings and supplies (0.98% from 0.34%).

- Core goods ex-used vehicles rose the fastest since Feb 2022 (0.32% M/M after 0.03).

- On the services side, note the 0.05pp drag on core inflation from lodging. Medical services made up for that, rebounding to contribute 0.05pp after 0.01pp; "other services" were then 3rd biggest contributor in our aggregates outside of housing (0.12pp) and the above-mentioned "other goods") (0.09pp).