FRANCE: Rpts-Lecornu Could Be Reappointed; Wider Deficit Targets To Pass Budget

France's political environment remains in a state of uncertainty ahead of caretaker PM Sebastien Lecornu's appearance on France 2 this evening at 20:00CET (14:00ET, 19:00BST). Earlier, Lecornu claimed that the prospect of a dissolution of parliament was fading. The fact that it is Lecornu speaking, and not President Emmanuel Macron, may lend credence to this view. It would be the head of state speaking to announce a dissolution.

- Instead, after meeting this afternoon with figures from the centrist/centre-right 'presidential bloc', Lecornu will hold talks with Macron at ~18:00CET on the political situation.

- Le Parisien reports that "According to our information, one scenario is holding the upper hand more than ever in recent hours: a reappointment of Lecornu [...]. "this would allow the president to [buy some] time and perhaps pass a budget before the end of the year, because that remains the priority," explains a senior figure in the executive."

- A major issue remains the prospect of the suspension of the 2023 pension reforms. A senior figure from the conservative Les Republicains has warned, "We don't see how the right could not censor a government that reverses the pension reform."

- Le Monde notes, the caretaker PM said earlier, "The public deficit target must be kept below 5%" in the next budget, or "between 4.7% and 5%." [...] The 5% figure is striking. It means that Sébastien Lecornu is prepared for the public deficit to fall by only 0.4 points of GDP in 2026, half the amount targeted by François Bayrou." A softer stance on fiscal consolidation would also be a sign of efforts to bring the Socialists on board.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

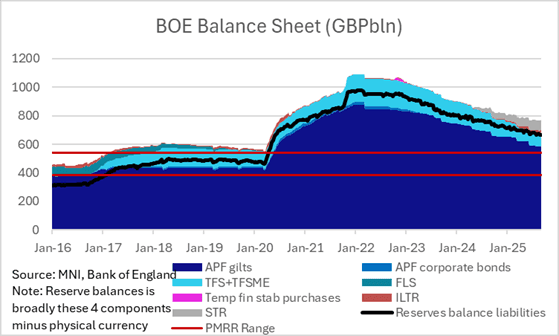

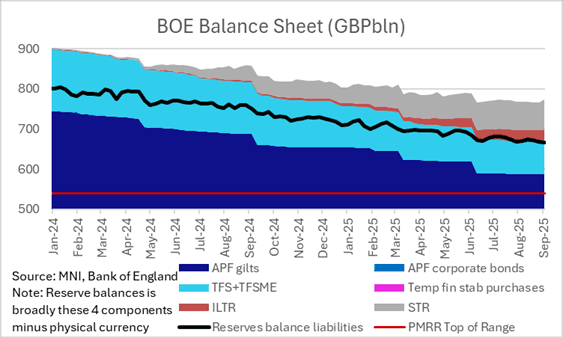

BOE: STR and ILTR operations post gilt redemption may impact 25/26 APF decision

- We will also be focusing on the take up of the STR and ILTR this week following the redemption of the formerly 10-year 2.00% Sep-25 gilt that has now matured.

- The BOE held GBP26.2bln of this gilt in nominal terms and will reduce the size of the APF holdings by GBP28.3bln in initial purchase terms.

- This follows a couple of weeks in which we have seen STR usage pick up by GBP9.6bln and ILTR usage pick up by GBP1.6bln.

- Together this means that demand-led balances have increased to GBP108.1bln (from the previous cycle peak of GBP102.2bln around 2 months ago.

- The market reaction will in our view will factor into the MPC’s decision on the size of the QT programme in the Oct’25 to Sep’26 period (which will be decided at the upcoming September MPC meeting).

- We favour keeping the pace of active sales broadly inline with the pace seen this year which would see around a GBP60-65bln target reduction in the size of the APF programme (including passive sales).

- We wrote more on this in July in BOE September APF Decision: What you need to know (see here).

US LABOR MARKET: MNI US Payrolls Preliminary Benchmark Revision Preview

We have published and e-mailed to clients the MNI Preview for tomorrow's preliminary benchmark revision to payrolls data. See the full note here: https://media.marketnews.com/US_Prelim_Benchmark2025_Preview_f1d718139b.pdf

- Tuesday’s preliminary annual payrolls benchmark revision is widely expected to imply large downward revisions to nonfarm payrolls growth through the twelve months to March 2025.

- We’ve seen estimates for a downward revision of at least 500k (using mid-point estimates when analysts quote a range) with a central guess of around -750k.

- History suggests the actual benchmark revision due with the Jan 2026 payrolls report will be smaller than what’s reported this week, but downward revisions could still be significant.

- Beware extrapolating these downward revisions beyond March 2025 after significant changes in the labor force since then.

- Also recall that last year saw issues in the publication of this preliminary estimate, with a late release.

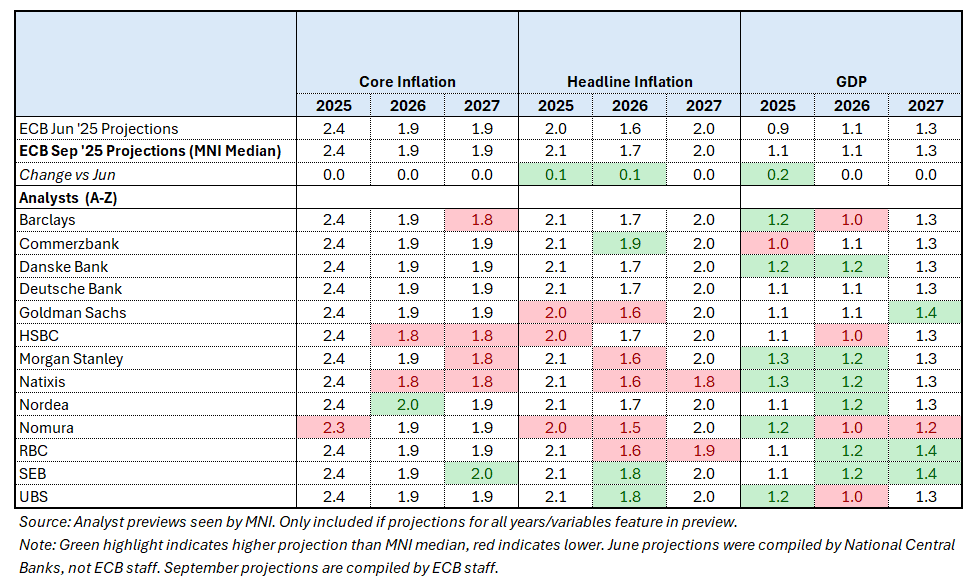

ECB: September Projection Revisions Expected To Be Centred In 25/26 (2/2)

Headline Inflation: Analysts pencil in small (one tenth) upward revisions to 2025 and 2026 headline inflation projections to 2.1% and 1.7% respectively. 2027 headline inflation is still expected to be on target at 2.0%.

- Higher-than-expected spot energy and food prices are expected to drive the upward revision to 2025 and 2026 headline inflation, albeit offset somewhat by a stronger Euro.

- Analysts are not expecting many revisions to culminate from the EU-US trade deal, while some highlight that the German government's U-turn on a proposed household electricity tax cut will push 2025 and 2026 projections higher.

- While 2025 headline inflation projections are concentrated at 2.0% and 2.1%, there is a larger range for 2026 of 1.5% to 1.9%. This appears to be due to differing expectations around the ECB’s technical assumption cut-off date – which would imply different estimates for oil and gas contributions to inflation revisions.

Core Inflation: Analysts on net do not expect any core inflation forecast revisions through 2027 (2025: 2.4%, 2026: 1.9%, 2027: 1.9%).

- Only one analyst expects a downward revision to the 2025 projection to 2.3%

- For 2026 and 2027, expectations range between 1.8-2.0%.