EM CEEMEA CREDIT: ROMANI: Spreads remain elevated ahead of second round

Republic of Romania (ROMANI; Baa3neg/BBB-neg/BBB-neg)

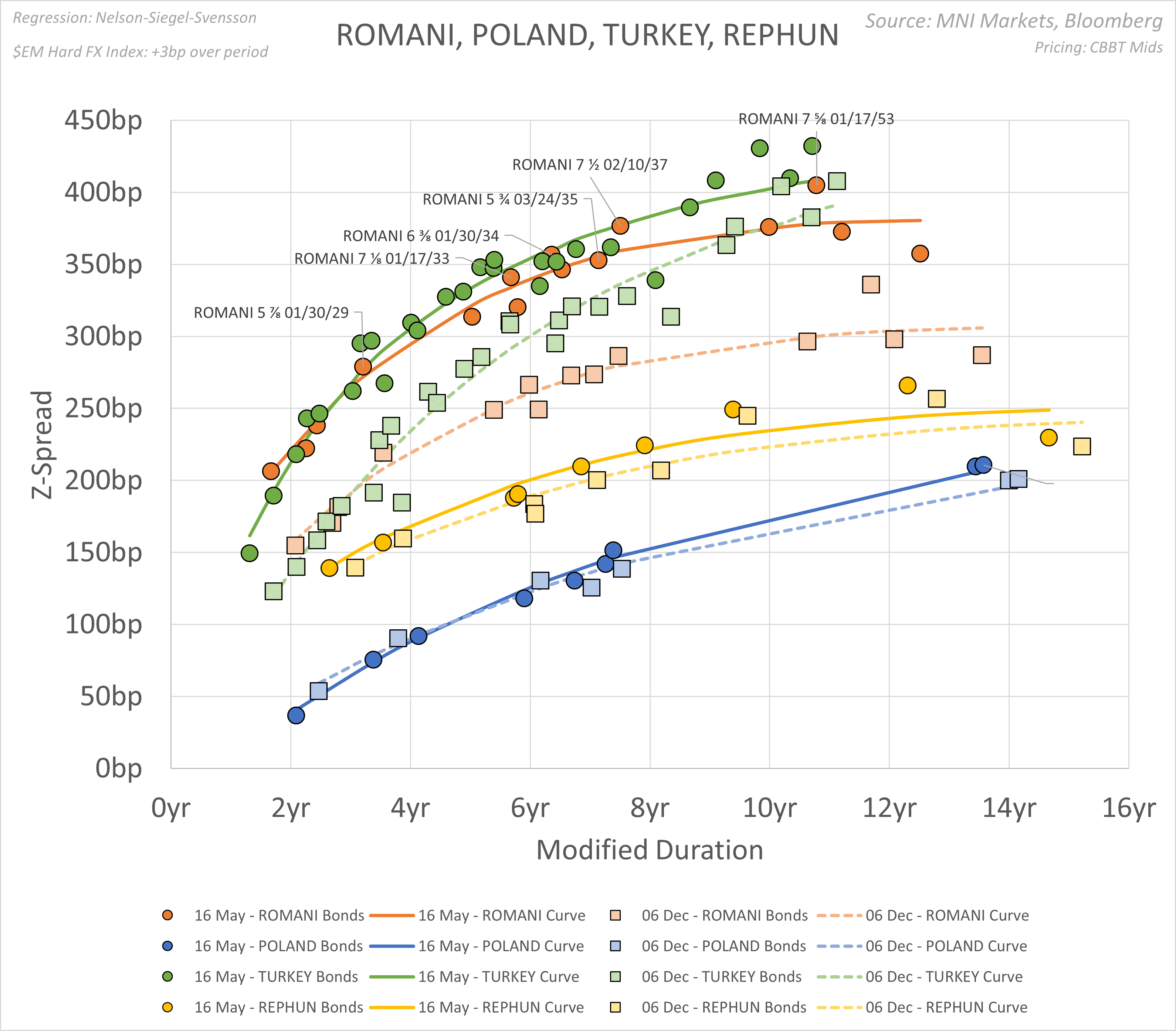

Spreads remain elevated ahead of the electoral second round

- We look at the recent spread evolution for Romania’s USD denominated sovereign curve, with anchor point Dec 6, 2024. Looking at peer sovereign curves, we note that with 10Y Romania at z+350bp area, the curve charts almost in line with Türkiye, whose 10Y is around z+360bp (see chart below).

- We highlight that in terms of moves, z-spreads for Romania’s 10Y tenors are some +70/+80bp wide vs levels seen on Dec 6, 2024. This move is twice that of Türkiye’s USD curve over the same period, whereas Hungary’s spreads are a mere +10/20bp and Poland’s - which is also seeing elections this w/e - are almost unchanged.

Romania is heading back to elections this w/e for the second round of the rerun of their presidential elections. Please refer to our earlier note for more context, link below:

https://www.mnimarkets.com/articles/romani-spreads-remain-elevated-ahead-of-elections-1741610596254

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Sell-Side Analyst Views After Q1 GDP

- Commerzbank expects the Chinese economy to come under significant pressure in the coming quarters. They have lowered their growth forecast for 2025 from 4.3% to 3.8% and for 2026 from 4.0% to 3.6%. To counter the tariff impact, they expect Beijing to frontload its stimulus measures, with more concrete policy steps probably announced after the Politburo meeting later this month.

- Goldman Sachs expects sequential GDP growth to drop significantly in Q2 and remain low in H2 on the back of severe external shocks from increased US tariffs despite the ongoing easing measures. They believe that the urgency for more policy stimulus is on the rise, with fiscal expansion to do most of the heavy lifting towards stabilising growth.

- HSBC says that the strong Q1 sets a good foundation for the year, but it's clear that more will need to be done to help offset the increased external headwinds. They see accelerated fiscal policy rollout, ongoing monetary easing as well as more policies to boost consumption to help support growth.

- JP Morgan have reduced their China GDP growth forecast further, reflecting the additional tariff shock and Q1 GDP data. They lower their Q3 GDP growth forecast to 0.4% q/q saar (from 1.8%q/q saar) and the Q4 GDP growth forecast to 2.0% q/q saar (from 3.0%). Their 2025 full-year growth forecast now stands at 4.1%, down from 4.4% previously.

- Nomura cut their annual GDP growth forecast from 4.5% to 4.0%, given the strong headwinds to growth. They expect quarterly y/y GDP growth to drop to 3.7%, 3.6% and 3.6% in Q2, Q3 and Q4, respectively. They take into account a larger and faster stimulus package from Beijing but believe that the gap might be too large for Beijing to meet its “around 5.0%” growth target.

- SocGen lower their 2025 and 2026 GDP growth forecasts to 4%, assuming additional stimulus of 2.5% of GDP, and now expect more sustained deflationary pressures this year and next. The short-term impact on the labour market is likely to be extremely hard to deal with. They believe a near-term RRR cut is possible to ease liquidity constraints and expect consumption and housing to be prioritised at the late April Politburo meeting.

US DATA: Strong First Quarter For US Industry, But Slowdown Looming

March industrial production was largely as expected, with headline IP growing contracting by 0.3% M/M (-0.2% survey) but prior upwardly revised by 0.1pp (+0.8%). Manufacturing production rose by 0.3% (0.2% survey 1.0% prior upwardly revised from 0.9%). Capacity utilization fell slightly (77.8% vs 78.2% prior).

- Dragging on IP was the utilities sector's 5.8% drop in output, "as temperatures were warmer than is typical for the month" (per the Fed report), a second consecutive month of contraction (-1.5% prior) - but this volatile category still posted 4.4% growth on a Y/Y basis (compared with 1.3% for IP as a whole). Mining also slowed in March, to 0.6% after 1.7% prior.

- Within the major final products categories, consumer goods saw a strong pullback (-1.0% M/M after 0.5% prior), and has barely grown in the past year (0.3% Y/Y), though business equipment fared better (1.7% M/M after 1.8%).

- Despite the March contraction, IP posted annualized growth of 5.5% in the first quarter of the year, the best 3M reading since May 2022. Overall manufacturing rose 5.1% for the quarter (annualized), led by durables (7.9%). There were some idiosyncrasies here, with motor vehicles and parts production jumping by 9.2% in February (likely tariff front-running) with the aerospace index rising 65% after contractions in previous quarters, potentially reflecting the end of a work stoppage at Boeing in Q4.

- Looking ahead to Q2, core durable goods orders have slowed since late last year while ISM Manufacturing has returned to contractionary territory (joining multiple other indicators in pointing to a tariff-related retrenchment), suggesting that the best may be behind the sector which could a pullback in activity in Q2.

EQUITIES: US Cash Opening calls

SPX: 5,338.3 (-1.1%); DJIA: 40,234 (-0.3%/-135pts); NDX: 18,482.5 (-1.8%).