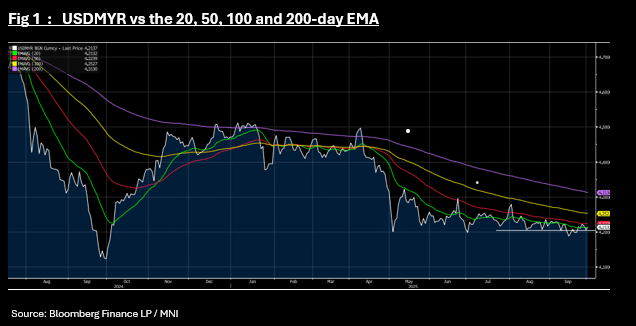

MYR: RInggit Through Key Technicals

- The Ringgit had a strong finish Tuesday, rallying into the close to end back at 4.2070. This is near the key technical it has tried multiple times to hold below, only to trade back above.

- This is what has occurred today as USDMYR gave back yesterday's gains and is weaker by +0.17% to be at 4.2140 ust above the 20-day EMA of 4.2132

- USDMYR I month ATM vol is up at 6.17 from 6.12

The FTSE Malay KLCI is having one its strongest day of the week, up +0.57% and bonds are selling off with the 3-Yr up +2bp to 3.14%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Most Major Bourses Lower in Monday Trade

The political unrest has seen a sell off in Indonesia continue, following Friday's steep declines. BYD’s Hong Kong-listed shares drop 8% in early trading on Monday after its second-quarter profit missed estimates as Morgan Stanley estimates its per vehicle profit, excluding contributions from BYD Electronic, likely fell to CNY4,800, the lowest quarterly level since 1Q22. Alibaba shares rise 15% in Hong Kong on Monday, the most in six months, after the Chinese e-commerce giant reported a surge in revenue from China’s AI boom, helping offset a surprise drop in profit.

- The HSI in Hong Kong has started the week off with a strong rally of +1.7% to trend above a major technical level. The CSI 300 is modestly lower by -0.12%, Shanghai Comp is up +0.12% and Shenzhen up +0.21%.

- The TAIEX in Taiwan kicks of another trading week with a decent fall of -1.2%.

- The KOSPI is down heavily by -1.3% at 3,143 to trade through the 20-day EMA. Below the 50-day EMA is at 3,113.

- Indonesia's is weighing heavy on SE Asia stocks with the JCI down -0.95% and the FTSE Malay KLCI down -0.75% .

- The Straits Times in Singapore is flat Monday whilst the PSEi in the Philippines is up +0.22%.

- The NIFTY 50 has started the week off positively with gains of +0.48%

LOOK AHEAD: Eurozone Final PMIs Start The Week Off

- The Eurozone final PMI surveys for August are due for manufacturing on Monday and services on Wednesday.

- The flash PMIs were surprisingly robust as the composite increased to 51.1 for another 0.2pt improvement, up from the 50.4 averaged in 1H25 and its highest since May 2024.

- Drivers were mixed however, with manufacturing leading the monthly improvement to 50.5 whilst services cooled to 50.7 as the two closed what has been sizeable divergence.

- This week's final readings should confirm that countries other than Germany and France have still been outperforming but by less than previous months.

- Since the flash PMI release, the European Commission's economic confidence index was softer than expected in August as it shifted back close to levels averaged in 1H25 and is comfortably below its long-term average.

JGBS: Futures Lower, JGB Yields Edge Higher, BoJ Speech/10yr Supply Tomorrow

JGB futures have tracked lower in the first part of Monday trade. We were last at 137.34, -.20 versus settlement levels for the Sep future. We are close to session lows, while Aug 26 lows at 137.22 aren't too far away. Today's move reinforces the bearish bias for JGB futures.

- There is no US cash Tsy trading today, but futures have been tracking lower (10yr to 112-13, -03) and this follows a steeper end to last week for the 2/10s curve. The Fed's Daly struck a dovish tone, noting policy will have to be recalibrated soon late on Friday.

- On the data front, capex in y/y terms was above expectations, pointing to a resilient backdrop. However, the q/q outcome was up only 0.2%. The MOF survey, based on demand-side data, is a key input for calculating Q2 GDP revisions due Sept 8. It suggested capex will be revised lower from the preliminary +1.3%, which was based only on supply-side data. Other data showed softer sales and company profits momentum for Q2.

- In the cash JGB space, yields have ticked higher, with the belly of the curve leading. The 7yr yield is up 2.5bps to 1.395%, while the 10yr is around 1.62%, just off recent cycle highs. The 2/30s JGB curve is at +231bps so slightly flatter versus end August levels.

- Note tomorrow, we have BoJ Deputy Governor Himino speaking in Hokkaido, at 10:30am local time.

- A 10yr JGB debt sale also takes place.