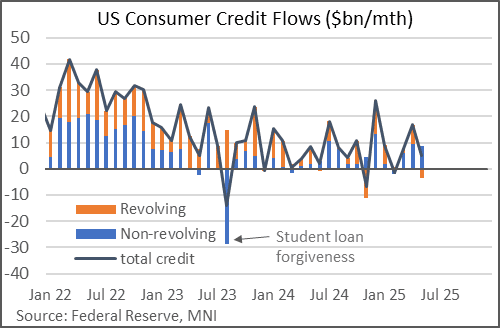

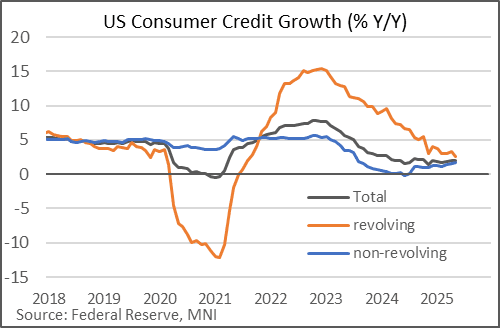

US DATA: Revolving Consumer Credit Growth Continues To Slow

Consumer credit growth continued to pick up modestly in June, though gains are increasingly led by non-revolving as opposed to revolving credit.

- Total consumer credit rose by $7.4B, roughly in line with expectations, and a pickup from $5.1B prior (revised slightly higher unrounded).

- But the breakdown showed a $1.1B contraction in revolving credit, the 2nd consecutive monthly fall, versus a $8.4B rise in nonrevolving credit (which

includes auto loans and student loans). - Revolving credit - which makes up 25% of overall consumer credit, and largely made up of credit cards - has been stuttering of late.

- The 3M annualized average growth of overall credit was steady at 2.3%, but for revolving it dipped to 0.7% from 1.6% prior for a 7-month low, with non-revolving ticking up to 2.9% on that basis, a 29-month high.

- On a Y/Y basis, revolving credit is up 2.5%, same as June for a joint-weakest in 46 months; non-revolving Y/Y growth ticked up to 1.9% from 1.8% for a 22-month best.

- Slowing revolving credit growth suggests that credit may be going from a modest tailwind for consumption and the economy, to something increasingly neutral.

- The latest Fed Senior Loan Officer Opinion Survey (July) showed mixed dynamics, though pointed to softer revolving credit growth: "For consumer loans, standards tightened for credit card loans and remained basically unchanged for auto and other consumer loans. Meanwhile, demand weakened for credit card and other consumer loans and strengthened for auto loans."

- This week's release of the NY Fed Household Debt and Credit Report saw consumer delinquency rates saw another push higher in Q2, driven by a further large jump in those for student loans as collections resumed.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: Small Business Hiring Steady Amid Stubborn Wage Pressures (2/2)

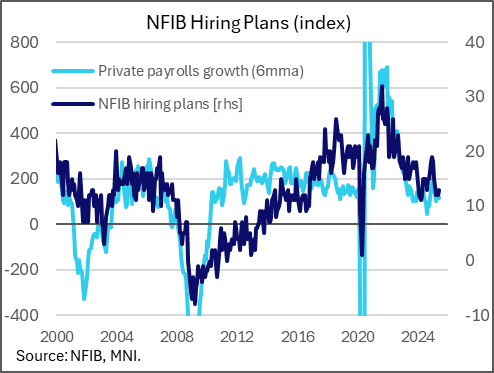

The second standout in June's NFIB report was the set of the labor market indicators. Net hiring plans have stabilized at 12-13% over the last 4 months, including 13% in June, after looking as though they were dropping quickly (18% in January). That's consistent with continued growth in private payrolls, albeit at low levels.

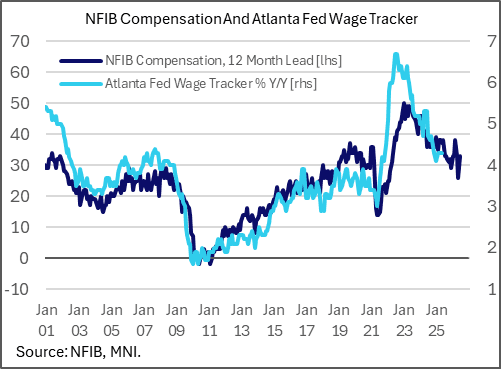

- The stubbornness in net compensation is more notable.

- Compensation plans were fairly steady (down 1 point to 19%, within the same broad range of the year so far), but the 33% reading for actual net compensation represented a 7ppt bounce from May which was a 51-month low but now looks like a temporary dip.

- This would be consistent with wage growth - per the Atlanta Fed's median wage tracker - in the low 4% Y/Y area for the next year.

- That could be interpreted largely through the lens of continued resilience in the labor market, but it could also be a warning sign for inflationary pressures vie higher unit labor costs if productivity fails to gain pace.

US DATA: Price Pressures Growing For Small Businesses (1/2)

The NFIB Small Business Optimism index ticked slightly lower in June (0.2pp to 98.6m exactly in line with consensus), resembling many surveys stabilizing after a tariff-related drop earlier in the year. But as usual with this report, the details were more interesting than the headline reading.

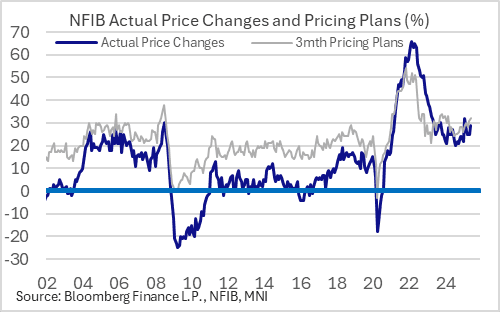

- The first standout was an increase in the main inflationary gauges which both appear to have bottomed out late last year.

- The net % raising selling prices (vs 3 months earlier) rose to 29% from 25%, the highest since February.

- And planned price increases (3-month ahead) picked up to a 15-month high net 32%, from 31% prior.

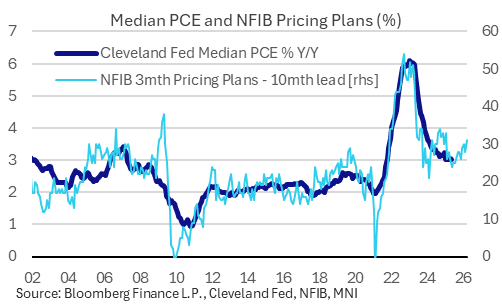

- These levels are consistent with underlying PCE inflation steadying out above 3% over the next 10 or so months (see chart).

- Small businesses are arguably under more pressure to absorb rising tariff costs than their larger corporate counterparts, so this bears watching over the coming months.

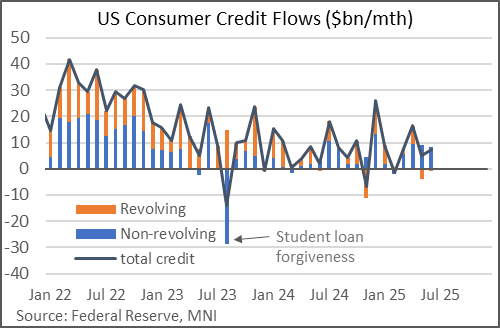

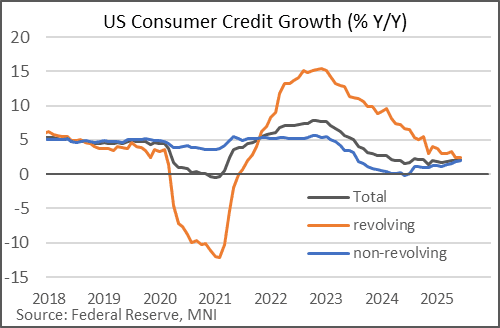

US DATA: Revolving Credit Growth Gradually Softening

Total consumer credit rose by $5.1B in May, about half of the consensus expectation and well below the $16.9B in April (downward rev from $17.9B). This was the lowest since February's $1.3B contraction.

- But the composition was also noteworthy: revolving credit (largely made up of credit cards) fell $3.5B (was +$7.5B prior), the first drop since November 2024 and only the 3rd fall in the last 17 months. Nonrevolving credit (which includes auto and student loans) flows remained strong, rising $8.6B (was +$9.4B prior).

- These series are very volatile on a month-to-month basis but broader trends are emerging. Revolving credit flows are now growing at the slowest rate (2.6% Y/Y) since August 2021, having gradually receded from double-digit growth in 2022 (which followed a sharp contraction in 2021).

- Conversely, nonrevolving growth has ticked up on that basis to 1.8% Y/Y, highest since August 2023.

- This represents a deleveraging in real terms given nominal GDP growth of 4-5% (was 4.7% in Q1). Indeed total credit outstanding remains below levels seen late last year.

- While sustained employment income gains have been the key underpinning of consumption in the last couple of years even as Covid-related government transfers have faded, slowing revolving credit growth and pickup in household savings suggests that credit may be going from a modest tailwind to something more neutral.

- That said, despite May's weakness, April's strong credit flow suggests a firmly positive credit impulse (3M/3M change vs year before), and other indicators (including the latest Dallas Fed banking and Fed Senior Loan Officer surveys) suggest consumer credit conditions are holding in.