CHILE: Retail Sales Slightly Above Expectations, IP Growth Disappoints

Aug-29 13:02

- "*CHILE JULY RETAIL SALES RISE 5.7% Y/Y; EST. +5.5%" - BBG

- "*CHILE JULY UNEMPLOYMENT RATE 8.7%; EST. 9.1%"

- "*CHILE JULY INDUSTRIAL PRODUCTION RISES 1.0% Y/Y; EST. +2.8%"

- "*CHILE JULY MFG PRODUCTION RISES 2.7% Y/Y; EST. +3.0%"

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Post-Data Phase of USD Strength Helps Majors Through New Levels

Jul-30 13:00

Post-data phase of USD strength has USD/JPY clearing yesterday's highs at typing - this makes for a fourth session of higher highs and brings key resistance at 149.18 into range - the Jul 16 multi-month high. This raises focus on sizeable option interest into 148.65/149.00 ($2.38bln). Having started somewhat weaker, the USD is now ahead as the best performer in G10 and EUR still remains the favoured expression: following yesterday's close below the 50-dma, EUR/USD is clear of 1.1519 support to expose 1.1446 and below.

- This makes for a higher USD Index: 99.421 the latest level to have been cleared, opening 99.864 downtrending 100-dma.

- In tandem with the USD strength, spot gold is under pressure here, dropping $15/oz to challenge the Monday pullback low.

STIR: Less Than 45bp Fed Cuts Priced Through Dec After GDP

Jul-30 12:57

Firmer-than-expected GDP data is worth ~1bp of additional hawkish repricing in end-of-year FOMC-dated OIS, leaving ~44.5bp of cuts priced over that horizon vs. 46.5bp pre-ADP.

- Contract fails to test last week’s hawkish extreme of ~41bp.

- Within the data, advance Q2 PCE metrics were mixed, headline was softer than expected, while core was firmer.

- SOFR-implied Fed terminal rate pricing out to 3.21% vs. 3.18% post-ADP, also well within the multi-week range.

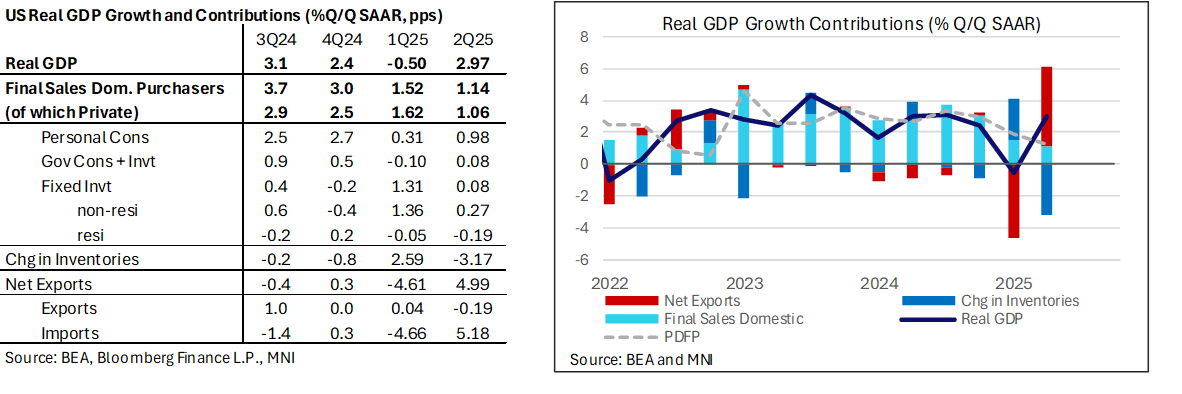

US DATA: Private Demand Softens Again In Q2 Flash But Could Have Been Worse

Jul-30 12:56

- Real GDP was stronger than expected in the Q2 advance release, rising 2.97% annualized vs Bloomberg consensus of 2.6%, although it was close to the 2.90% upgrade in yesterday’s final Atlanta Fed GDPNow entry.

- The 1.2% averaged in 1H25 compares with 2.5% in 2024.

- Private domestic final purchases (PDFP), a measure Powell frequently acknowledges, moderated further to 1.2% annualized (its weakest since 4Q22) from 1.9% in Q1. The 1.6% averaged in 1H25 compares with 3.0% in 2024.

- The 1.06pp contribution to GDP from PDFP was better than the 0.7pp pencilled in by GDPNow with an offset from weaker government consumption, only adding 0.1pp vs expectations of 0.4pp.

- The upward surprise to analyst expectations came away from private consumption, which underwhelmed slightly with 1.4% annualized (both Bloomberg consensus and GDPNow pencilled in 1.5%) after 0.5% in Q1. Tomorrow’s monthly PCE report for June will give a better idea of latest momentum.

- As for the noisier items, there were even larger swings in trade and inventories than expected, but they netted out relative to GDPNow expectations.

- Net exports: 4.99pp (GDPNow 4.00pp) after -4.6pp

- Changes in inventories: -3.17pp (GDPNow -2.2pp)

- Other notable contributions came from non-residential investment returning to a more typical 0.3pps after a booming 1.4pp in Q1 on likely tariff front-running whilst residential investment remains under pressure with -0.2pp. The latter has seen a volatile few quarters but its weakening trend is becoming increasingly clear with -1.3% Y/Y.