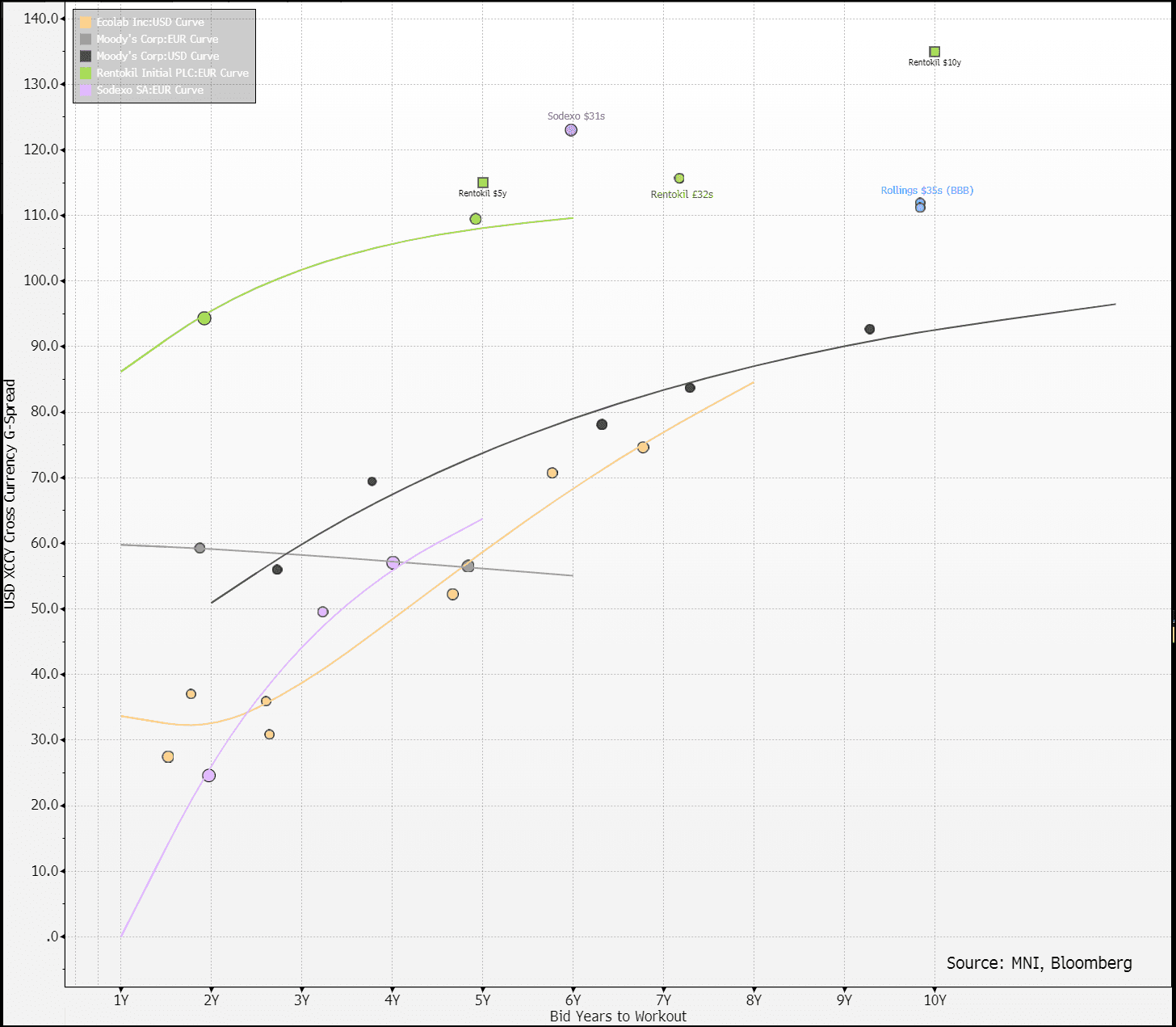

EU CONSUMER CYCLICALS: Rentokil; $ FINAL pricing

(RTOLN; NR/BBB/BBB)

• Well covered books, pricing was inside Sodexo $31s but still +40 wide of $-Moody's.

• Bears will point to cash px (priced below par, CoC at 101) for $ being able to head tighter than €/£.

• As we said LBO rumours have long since been dismissed.

• We are bit disappointed it has brought net supply of $550m/+0.5x when it was well outside leverage target (2.9x vs. 2.0-2.5x) - S&P has commented since and seems fine with it.

• We still see some value on the € high-cash px lines though above has weakened it. US skewed exposure but can be diversified through services peers like Elis (no US).

- $750m 5y UST +115

- -30 from IPT, books $2.6b

- $500m 10y UST +135

- -35 from IPT, books $3.0b

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US FEB NEW HOME SALES +1.8% TO 0.676M SAAR

- MNI: US FEB NEW HOME SALES +1.8% TO 0.676M SAAR

- US JAN NEW HOME SALES REVISED TO 0.664M SAAR

EQUITY TECHS: E-MINI S&P: (M5) Holding On To Its Recent Gains

- RES 4: 5970.87 61.8% retracement of the Feb 19 - Mar 13 bear leg

- RES 3: 5924.59 50-day EMA

- RES 2: 5864.25 Low Jan 13 and a recent breakout level

- RES 1: 5834.00 Intraday high

- PRICE: 5819.25 @ 13:48 GMT Mar 25

- SUP 1: 5650.75/5559.75 Low Mar 18 / 13 and the bear trigger

- SUP 2: 5483.50 2.00 proj of the Dec 6 ‘24 - Jan 13 - Feb 19 swing

- SUP 3: 5396.00 2.236 proj of the Dec 6 ‘24 - Jan 13 - Feb 19 swing

- SUP 4: 5341.87 2.382 proj of the Dec 6 ‘24 - Jan 13 - Feb 19 swing

The trend condition in S&P E-Minis is bearish and the latest recovery appears corrective. MA studies are unchanged - they remain in a bear-mode set-up, highlighting a dominant downtrend. However, this week’s gains have resulted in a breach of the 20-day EMA, at 5803.08. This signals scope for a continuation higher near-term - towards 5864.25, the Jan 13 low. A reversal lower would refocus attention on 5559.75, the Mar 13 low and bear trigger.

GBP: Most Analysts See Risks Tilted to EURGBP Strength

- SocGen believe that GBP positioning sits uncomfortably with the parlous state of the UK’s public finances. They state there’s a good case for being long EUR/GBP here, regardless of yesterday’s stronger PMI data, and remain bearish GBP vs. the Scandies.

- ING have noted the gilt market will be on the lookout for any missteps in the very tight room for fiscal manoeuvring, and the bar for a negative reaction either in bonds or a meaningful repricing lower in growth expectations both have the potential of hitting sterling. They see upside risks to EUR/GBP extending beyond the recent 0.845 highs this week.

- BBVA have said that with a challenging domestic environment and subdued growth outlook, they believe sterling will weaken for the rest of the year, particularly against EUR.

- JP Morgan’s technical team stated that GBPUSD’s decelerating rally triggered a cluster of their pattern-base sell signals, which increase the probability for a near-term pullback within the developing bull trend. JPM believe that EURGBP is about fair; however, there is room to overshoot fair value if fiscal concerns intensify. Notably, they have entered a EUR/GBP & EUR/CHF topside dual digital.

- Separately, Rabobank say EUR’s recent loss of momentum has allowed EUR/GBP to edge lower towards its average level of the past 6-month. Rabo see scope for the EUR to give back some more of its recent gains in Q2 and they retain their forecast of EUR/GBP0.83 on a 3-month view.