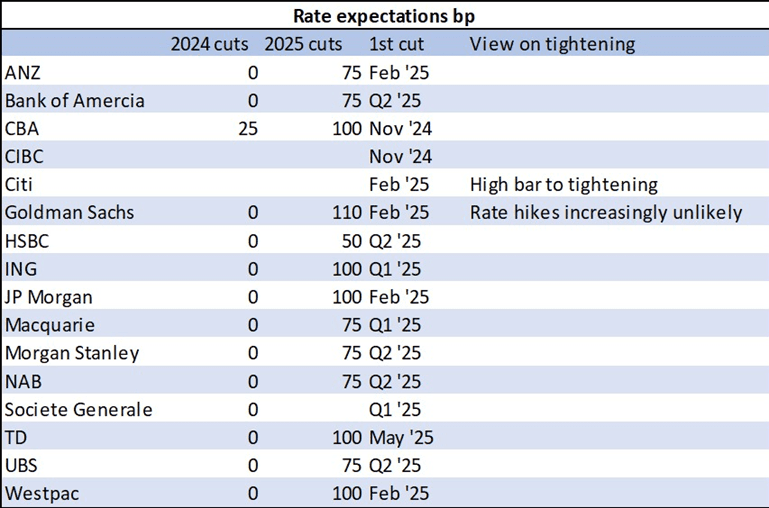

AUSTRALIA: RBA Rate Cut Expectations Delayed Until Well Into 2025

In August RBA Governor Bullock clearly said that it is too early to discuss rate cuts and while the Board isn’t “ruling anything in or out”, current conditions do not warrant a “near-term” easing. Forecasters have shifted out their rate cut expectations with few now projecting one before year end and Bloomberg consensus has one 25bp in Q1 2025 with 85bp by end-2025. However, our policy reaction function, now with the core inflation gap, still estimates rates trending higher.

- Bloomberg consensus has only 5bp of easing in Q4 2024 followed by 20bp in Q1 2025 compared with the current rate of 4.35%. There’s a full 25bp in Q2 2025. Many analysts don’t expect the first cut until Q2 2025, while in contrast the market has 25bp of easing priced in by end-2024.

Source: MNI - Market News/Bloomberg

- In the FY25 budget the federal government announced cost-of-living measures, which temporarily reduces headline inflation for the year from July, especially the energy rebate. July CPI data is released August 28.

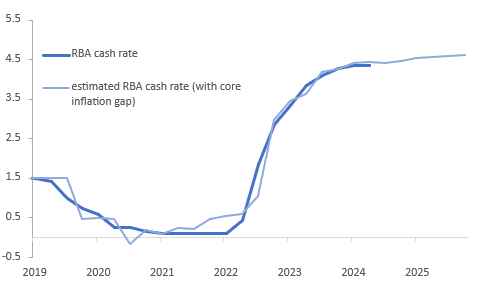

- The RBA has said that it will look through the transitory reduction in inflation and focus on the underlying trimmed mean. As a result, we have re-estimated our simple RBA policy reaction function with the core inflation gap.

- Economic fundamentals suggest that rates should be only around 5bp higher in Q3 than they currently are but then almost 40bp higher by end-2025. This is around 15bp more than the original equation, which continues to use the RBA’s May forecasts, as not only does the core inflation gap have a larger coefficient but it is forecast to be 0.1pp higher in Q4 2025.

Source: MNI - Market News/Refinitiv

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGB TECHS: (U4) Sell-Off Stabilises into Friday Close

- RES 3: 148.74 - High Jul 24 (cont)

- RES 2: 147.74 - High Jan 15 and bull trigger (cont)

- RES 1: 144.88/145.95 - High May 8 / High Mar 25

- PRICE: 142.93 @ 14:49 BST Jul 26

- SUP 1: 142.23 - Low Jul 02

- SUP 2: 141.57 - 1.0% 10-dma envelope

- SUP 3: 140.21 - 1.236 proj of Mar 22 - Nov 1 ‘23 - Jan 15 price swing

JGB futures looked to finish the week comfortably off the mid-week lows, although still lower since Monday’s open. The price action across Thursday & Friday trade snaps the losing streak off the mid-July highs and eyes the 50-dma resistance above at 143.07. Clearance here would shift the near-term outlook more positive, and eye 143.57 as the next key level. This week’s lows of 142.42 mark first support.

USDCAD TECHS: Overbought But Bull Cycle Remains In Play

- RES 4: 1.3899 High Nov 1 and a key resistance

- RES 3: 1.3866 1.0% 10-dma envelope

- RES 2: 1.3855 High Nov 10 2023

- RES 1: 1.3849 High Jul 25

- PRICE: 1.3814 @ 15:36 BST Jul 26

- SUP 1: 1.3778 Low Jul 24

- SUP 2: 1.3715 20-day EMA

- SUP 3: 1.3690 50-day EMA

- SUP 4: 1.33657 Low Jul 17

The impulsive rally in USDCAD persists, with the pair showing above 1.3792 resistance this week, topping out at 1.3849. This has resulted in a print above key resistance at 1.3846, the Apr 16 high. Conditions are overbought, however, a clear break of 1.3846 would strengthen the bull theme and pave the way for a continuation higher, towards 1.3899, the Nov 1 high ‘23 and a key resistance. Firm support lies at 1.3690, the 50-day EMA.

FED: MNI Fed Preview - July 2024: September Signals In Spotlight

We've just published our preview of the July 30-31 FOMC meeting - PDF here (and emailed to clients):

- The Fed will hold rates for an 8th consecutive meeting at its July meeting, putting immediate attention on any signals about rate cuts beginning in September.

- While inflation and the labor market cooled in the second quarter, providing a clear path to rate cuts by year-end, underlying demand has remained resilient in defiance of what FOMC officials see as “sufficiently restrictive” policy.

- With the lingering memory of various data "head fakes" in mind on both the upside and downside of the inflation and rate cycles, yet a “soft landing” still seen in reach, the FOMC is likely to express only cautious optimism.

- The policy statement is due for key adjustments to the characterization of recent inflation and employment, and perhaps to the shifting balance of risks – but it’s not clear the Committee will adjust the forward rate guidance, in contrast to previous cycles where it explicitly signaled that it could move rates at an upcoming meeting.

- That would put the focus on Chair Powell to deliver the message at the press conference that the FOMC is cautiously open to cuts at upcoming meetings.

- The absence of a clear signal about an upcoming rate cut would disappoint current market pricing for 2 to 3 rate cuts by year-end, which is more aggressive than the 1 to 2 cuts the FOMC eyed just 6 weeks ago.