US CREDIT SUPPLY: Rabobank $Bmark Sr Pref FV

Oct-10 11:35

(Aa2/A+/A+)

• MNI FV 3Y Fixed 33a

• IPT 3Y Fixed +55-60 3Y FRN SOFR Equiv

• RABOBK 4.494 2029s ($750MM o/s) are trading at g34 today, and RABOBK’s curve is ~15bps inside 1 notch lower ABN with ABN 4.197 28s trading at g47. We adjust for the curve to get to our FV of 33a. The RABOBK 4.8 29s are relatively illiquid.

• Issuer: Cooperatieve Rabobank UA/NY (RABOBK)

• Format: 3a2, senior preferred

• Aa2/A+/AA- (expected)

• Bookrunners: BARCS, BNPP, BofA, JPM, RABO, WFS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - Bear Threat In Oil Futures Remains Present

Sep-10 11:32

- On the commodity front, Gold remains in a clear bull cycle and last week’s gains plus this week’s bullish start to the week, reinforce current conditions. The yellow metal has traded to a fresh all-time high. The break also confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3674.8, A 2.382 projection of the Dec 30 ’24 - Apr 3 - 7 price swing. Initial firm support lies at $3474.7, the 20-day EMA.

- In the oil space, the trend condition in WTI futures is unchanged - a bear cycle remains intact. The pullback from the Sep 2 high highlights a possible reversal and the end of the corrective phase. Initial resistance to watch is $66.03, the Sep 2 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would pave the way for a move towards $57.71, the May 30 low.

US TSY FUTURES: BLOCK: Dec'25 2Y Buy

Sep-10 11:28

- +4,000 TUZ5 104-12.62, buy through 104-12.5 post time offer at 0713:00ET, DV01 $163,200.

- The 2Y contract trades 104-12.5 last (-.62)

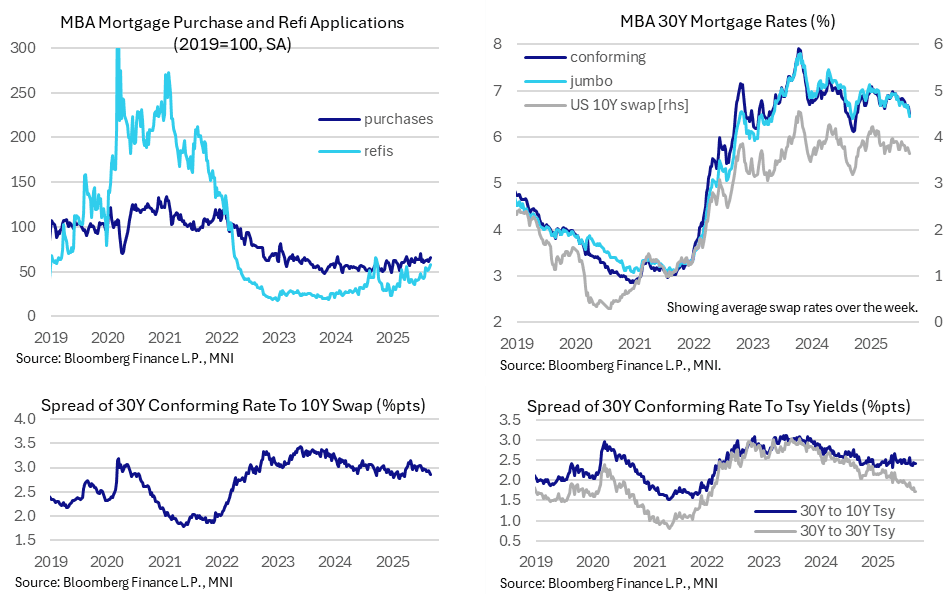

US DATA: Mortgage Applications See A Latest Step Higher On Rates Drop

Sep-10 11:25

MBA mortgage applications saw some traction from lower rates last week, with the level of composite applications at its highest since mid-2022 after 30Y mortgage rates fell 15bp to the lowest since Oct 2024.

- MBA composite mortgage applications stepped 9.2% higher last week (sa), following three small declines that had only chipped away at a solid 11% increase earlier in August.

- It was led by refis rising 12% M/M, but as opposed to that early Aug 11% increase when refis jumped 23%, there was a more broad-based contribution with new purchase applications rising 6.6% (vs 1.4% in that previous composite step higher).

- Bear in mind still very subdued levels relative to 2019 averages though: composite 63% (highest since Jul 2022), new purchases 65% and refis 58%.

- The push to new recent highs followed a sizeable drop in the 30Y conforming mortgage rate to 6.49% (-15bps) for a 35bp decline since mid-July and its lowest level since Oct 2024.

- The decline in mortgage rates exceeded the 7bp decline in the average 10Y swap rate over the week, pushing the 30Y mortgage to 10Y swap rate spread down to 285bp.

- That’s the tightest spread since reciprocal tariffs were first announced in early April at which point it widened to 315bp in the month that followed and then held around 300bp +/-5bp for some time. It’s also coincidentally back to where it averaged through 1Q25.

- Note that this follows US Tsy Sec Bessent in recent weeks talking on wanting to keep the spread between mortgage rates and treasuries flat or even bring it down.