CANADA DATA: Q2 GDP -1.6% Annualized On Auto Exports; July Flash +0.1%

- Canada Q2 GDP -1.6% annualized, most in 5 years, amid US trade tensions. Figure is close to Bank of Canada’s "current tariff scenario" of -1.5% and lower than -0.8% economists expected.

- Exports -27% or the most since 2009 financial crisis excluding the pandemic. Business investment in machinery and equipment fell the most since 2016, StatsCan said Friday.

- Final domestic demand +3.5% in Q2 from -0.9% in Q1.

- July advance GDP estimate +0.1% MOM after three straight declines of 0.1%. July increase was driven by real estate, mining and wholesale, partially offset by decline in retail.

- June GDP -0.1%, below economist expectations for +0.2%. Decline was driven by manufacturing -1.5%.

- Economists split on whether central bank will hold key interest rate or cut at Sept. 17 decision. BOC had said it could cut if economy weakens and inflation remains under control. Core inflation remains elevated at the higher end of BOC's 1%-3% target range.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Instant Answers For US Treasury Refunding

- Is the guidance on coupon issuance unchanged? “Treasury anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters.” YES, no change to guidance

- Total maximum purchase amount of buybacks in the 20Y-30Y range: USD8 billion

- Total maximum purchase amount of buybacks in the 10Y-20Y range: USD8 billion

No change in nominal Treasury coupon sizes to the coming quarter, marking six consecutive refundings of no increase.

Treasury is doubling the frequency of liquidity support buybacks in both the 10- to 20-year and 20- to 30-year nominal coupon buckets to four times per quarter from two times per quarter, based on feedback from market participants. These changes will increase the aggregate size of liquidity support buybacks from a maximum par amount of $30 billion per quarter to $38 billion per quarter.

It's also making a technical adjustment to the TIPS buyback buckets, increasing the size of cash management buybacks and planning to allow a "limited number" of additional counterparties to directly access buyback operations in the first half of 2026. Treasury is increasing the aggregate size of cash management buybacks from a maximum par amount of $120 billion per year to $150 billion per year.

For the current quarter, Treasury does not anticipate conducting cash management buybacks around the September tax date in light of the ongoing cash balance rebuild. Cash management buybacks are expected to resume in December.

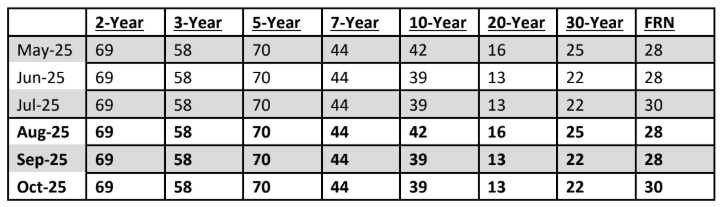

Table below shows the actual auction sizes for the May to July 2025 quarter and the anticipated auction sizes for the August to October 2025 quarter (in billions of dollars):

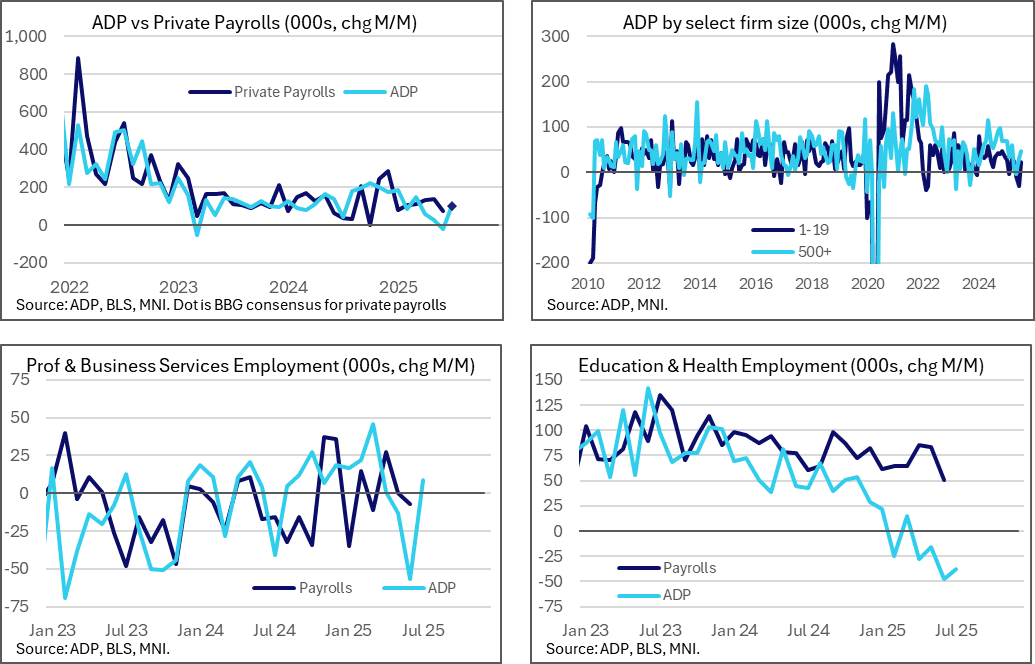

US DATA: ADP Surprises Stronger, With Improvements Across Most Sectors

- ADP private employment was stronger than expected in July, increasing 104k (cons 76k) after an upward revised but still unusually weak -23k (initial -33k) in June.

- Service-providing jobs increased 74k and goods-producing jobs increased 31k.

- Within services, there were sequential improvements almost across the board with exception for the education & health which continues to strangely weak compared to its BLS payrolls counterpart.

- The largest sequential improvement came for “professional and business” at 9k after a particularly heavy -57k and “financial activities” at 28k after a rare -12k.

- “Education & health” continued to buck the trend, falling -38k after -48k for a fifth monthly decline across the past six months. Highlighting just how weak this has been relative to payrolls, it averaged -31k in Q2 and 4k in Q1 compared to 73k and 64k for education & health private payrolls.

- Smallest businesses (1-19 employees) had come under most pressure with -31k in June but somewhat bounced back with 22k in July.

- ADP’s Nela Richardson on the report: “Our hiring and pay data are broadly indicative of a healthy economy. Employers have grown more optimistic that consumers, the backbone of the economy, will remain resilient."

- From the separate Pay Insights report: “ADP Pay insights:

- "Year-over-year pay growth in July was 4.4 percent for job-stayers and 7 percent for job-changers. Gains have held steady for the past four months."

STIR: Modest Hawkish ADP Adjustment In Fed Pricing, 45bp Cuts Priced Through Dec

Modest hawkish adjustment in Fed pricing following the firmer-than-expected ADP employment data, with the wages sub-component of the report holding above 4% growth levels.

- Still, moves are modest, with FOMC-dated OIS showing 45.5bp of cuts through year-end vs. ~46.5bp ahead of the data.

- Sub-1bp of easing price for this evening’s FOMC decision, 16.5bp through September and 28.5bp through October.

- Lack of movement explained by the lack of short-term ADP correlation to NFPs and impending heavy risk event schedule.

- SOFR-implied terminal rate pricing little changed at 3.18%.