TURKEY: Public, Private Household Inflation Survey Gap Still Too Wide

- Banking sector loan volumes are rising, according to Dunya. The total book rose faster than inflation in the seven months to July, at a pace of 5.2% in real terms to just shy of TRY 20trl.

- The divergence in public and private inflation expectations surveys continues: the Koc-Konda Household Inflation Expectations survey sees current inflation at 71%, year-end at 65% and 12-month at 61%. This compares to official surveys showing 12m expectations at just 54.5%. Ekonomi write that success in fighting inflation will require a convergence in these two metrics.

- Firms of various sizes and across industries are opting to restructure debt and extend terms rather than pay off the principal, according to an Ekonomi report. They write that individuals, SMEs and larger businesses are keeping cash on hand rather than paying down outstanding debt in the current environment.

- Volatile items prices have come into focus this week, particularly on reports that fresh fruit prices are dropping at a rate of 9% a month. Today, Dunya cite comments from the Istanbul Fresh Fruit and Vegetable Exporters' Association in writing that this year's frost prompted a decline in capacity across Q1, but a gradual recovery is underway thanks to the start of seasonal production and an increase in export orders.

- The favourable run of recent inflation data has firmed expectations that more CBRT easing is to come, according to columnist Erkin Isik in Dunya. They write that this should support bond and equity investments as markets price a medium- to long-term economic recovery.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

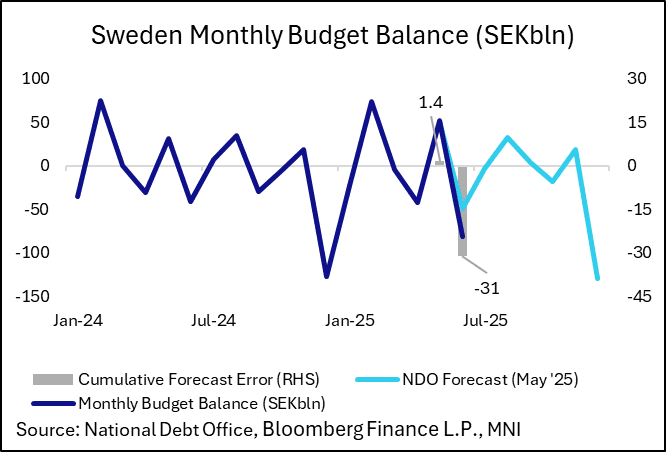

SWEDEN: Budget Balance Well Below Debt Office Forecasts In June

The Swedish budget moved back into deficit in June, with the -SEK81.7bln reading well below the National Debt Office’s -SEK49.2bln projection in the May borrowing report. Two factors explain the forecast error: First, net lending to government agencies was SEK22.7bln higher than expected (due to lower-than-expected deposits from the Swedish Pensions agency). Second, there was a SEK16bln shortfall in net tax receipts, with the primary balance at -SEK51.0bln (vs -SEK40.7bln projected).

- The next NDO Borrowing Report is not due until November 27th. Any changes to the net borrowing requirement and associated issuance strategy will take into account existing budget balance forecast errors from the May report and the details of the autumn budget (expected to be presented in September).

- The Government has already announced a plan to cut corporation tax to 20% from 20.6%, potentially alongside a cut to the tax on electricity consumption (see here)

- Additionally, the Government has committed to NATO’s 3.5% +1.5% GDP defence target. While the NDO already assumed defence spending of 3.5% in the May report, there may (but not necessarily) be some upside risks to borrowing estimates from the extra 1.5% on “defence-related spending” (see here).

- NDO issuance is on summer break after a heavy June, which included the launch of the new 2.5% Oct-36 SGB and a E2bln syndicated launch of the 2% Jun-26 EUR SGB. Demand metrics at the Oct-36 SGB conventional auctions weren’t too strong, which may represent markets adjusting to the higher nominal issuance auction sizes (SEK6bln).

SILVER TECHS: Trend Signals Remain Bullish

- RES 4: $39.026 - 1.382 proj of the Apr 7 - 25 - May 15 swing

- RES 3: $38.246 - 1.236 proj of the Apr 7 - 25 - May 15 swing

- RES 2: $38.000 - Round number resistance

- RES 1: $37.317 - High Jun 18 and the bull trigger

- PRICE: $36.584 @ 08:13 BST Jul 7

- SUP 1: $36.072 - 20-day EMA

- SUP 2: $34.944/31.651 - 50-day EMA / Low May 15

- SUP 3: $30.915/28.351 - Low Apr 11 / 7 and the bear trigger

- SUP 4: $27.686 - Low Sep 6 ‘24

A bull cycle in Silver remains intact. The metal has recently traded through resistance at $34.903, the Oct 23 ‘24 high and a key bull trigger. The break of it marks an important medium-term bullish development. Sights are on the $38.00 handle next. On the downside, initial support to watch lies at $36.072, the 20-day EMA. It has been pierced, a clear break of it would open $34.944, the 50-day EMA.

USDCAD TECHS: Trend Structure Remains Bearish

- RES 4: 1.3920 High May 21

- RES 3: 1.3862 High May 29

- RES 2: 1.3798 High Jun 23

- RES 1: 1.3667/3769 20- and 50-day EMA values

- PRICE: 1.3649 @ 08:09 BST Jul 7

- SUP 1: 1.3557 Low Jul 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

The trend needle in USDCAD continues to point south and last week’s move down reinforces current conditions. S/T gains between Jun 16 - 23 appear to have been corrective. Sights are on key support and the bear trigger at 1.3540, Jun 16 low. Clearance of this level would resume the downtrend and open 1.3503, a Fibonacci projection. Pivot resistance is at the 50-day EMA, at 1.3769. A clear break of it would signal scope for a stronger recovery.