OUTLOOK: Price Signal Summary - Gold Appears Comfortable Above $4000.00

Oct-08 11:05

- On the commodity front, a bull cycle in Gold remains in play and this week’s breach of $4000.0 reinforces the uptrend. The move higher maintains the price sequence of higher highs and higher lows. Furthermore, momentum studies highlight a condition known as momentum drag - where momentum remains in overbought territory and moves sideways - a bullish signal. Sights are on $4074.54, a 2.500 proj of the May 15 - Jun 16 - 30 price swing. Support to watch is $3775.3, 20-day EMA.

- In the oil space, WTI futures have recovered from the most recent low print - a correction. A bearish theme remains intact. Last week’s sell-off resulted in a move through key support and the bear trigger at $60.85, the Aug 13 low. Clearance of this level strengthens the bear threat and paves the way for an extension towards $57.50, the May 30 low. Initial firm resistance has been defined at $66.42, the Sep 29 high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Modestly Twist Steeper Within Payrolls Driven Ranges

Sep-08 11:01

- Treasuries sit twist steeper but within Friday’s payrolls-driven range.

- The JGB curve twist steepened following Sunday’s resignation of LDP leader Ishiba although spillover to Treasuries was limited with the Asia cash open.

- It’s a quieter start to the week with Trump remarks to the White House Religious Liberty Commission at 1010ET possibly the main scheduled event along with the NY Fed's consumer survey including its inflation expectations.

- Greater focus is on preliminary payrolls benchmark revisions, PPI and CPI over Tue-Thu, with previews for those out later today and tomorrow.

- Cash yields are between 0.8bp lower (2s) to 1.8bp higher (30s).

- Curves are off recent steeps, including 2s10s at 58.3bp off Wednesday’s 63.9bp and 5s30s at 119.3bp off 126.9bp post-NFPs (multi-year steeps).

- TYZ5 trades near unchanged at 113-11 (-01+) on modest cumulative volumes of 265k.

- The post-payrolls high of 113-21+ marked another fresh short-term cycle high and points to a bullish structure. It marks resistance after which lies 113-26+ (2.764 proj of Jul 15-22-28 price swing) whilst support is seen at 112-28+ (Sep 5 low).

- Data: NY Fed consumer survey Aug (1100ET), Consumer credit Jul (1500ET)

- Bill issuance: US Tsy $82B 13W & $73B 26W bill auctions (1130ET)

- Politics: Trump delivers remarks (1010ET)

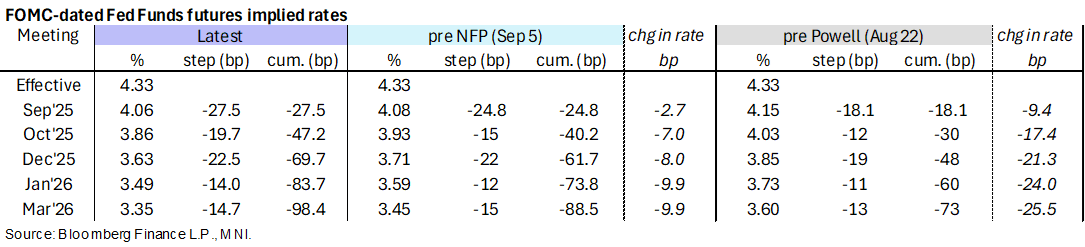

STIR: Payrolls Rally Broadly Consolidated With Tue-Thu Data Eyed

Sep-08 10:43

- Fed Funds implied rates are little changed since Friday’s close, holding what was only a modest paring of the rally on a soft payrolls report at the time.

- It sees close to three consecutive cuts priced to year-end, with only limited odds of a 50bp cut next week (~10%).

- Cumulative cuts from 4.33% effective: 27.5bp Sep, 47bp Oct, 69.5bp Dec, 83.5bp Jan and 98.5bp Mar.

- The SOFR implied terminal yield of 2.86% (SFRH7) is 1bp lower from Friday as it sits a little off 150bp of cuts ahead from current levels. The yield is only 2.5bp lower than levels just prior to the NFP release after rates rallied into the release.

- It’s a quieter start to the week before preliminary payrolls benchmark revisions, PPI and CPI over Tue-Thu. The Fed is now in media blackout ahead of the FOMC meeting on Sep 16-17.

LOOK AHEAD: Monday Data Calendar: NY Fed Inflation Exp, Consumer Credit

Sep-08 10:41

- US Data/Speaker Calendar (prior, estimate)

- 09/08 1100 NY Fed 1-Yr Inflation Expectations (3.09%, --)

- 09/08 1130 US Tsy $82B 13W & $73B 26W bill auctions

- 09/08 1500 Consumer Credit $7.371B, $10.2B)

- Source: Bloomberg Finance L.P. / MNI