EM ASIA CREDIT: POSCO Holdings: EU tariffs will hurt

(POHANG, Baa1/A-neg/NR)

"S. Korea Sees ‘Significant Impact’ From EU Steel Protection Plan" - BBG

Korean steelmaker POSCO Holdings is likely to be impacted by the EU’s proposed steel tariffs and reduced import quotas. The Korean Ministry of Trade has stated that new EU steel tariffs of 50%, combined with a cut of roughly 45% in import quota volumes, will negatively affect the domestic steel industry, which relies on the EU as its second largest export market. The measures will make Korean steel less competitive in Europe and could pressure credit spreads for the sector.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Off Friday Highs, JGB Curve Steeper, US-JP 10yr Diff At Fresh Lows

JGB futures sit at 137.96, flat versus settlement levels in latest dealings. This is comfortably off intra-session highs from Friday (138.37), but recent lows, near 137.20, are still some distance away.

- Some negative bias is likely coming from the modestly softer US Tsy futures tone (TY is off -04) in early Monday dealings.

- Positive Q2 GDP revisions may have also helped at the margins, with Q2 growth revised up to 0.5%, from an initial estimate of 0.3%. Still, this hasn't done much for the yen, which is still down 0.70% for the session so far.

- Political concerns are weighing on the yen, although local equities are at fresh record highs.

- In the cash JGB space, back end yields are higher, with the 40yr up near 4bps to 3.51%. The 20 and 30yr tenors are +2bps higher, the 30yr yield back close to 3.27%. The 10yr yield is little changed at 1.58%. The JGB 2/30s curve is +2bps steeper, back to +243bps.

- The US-JP 10yr spread is at +251bps, fresh lows back 2022.

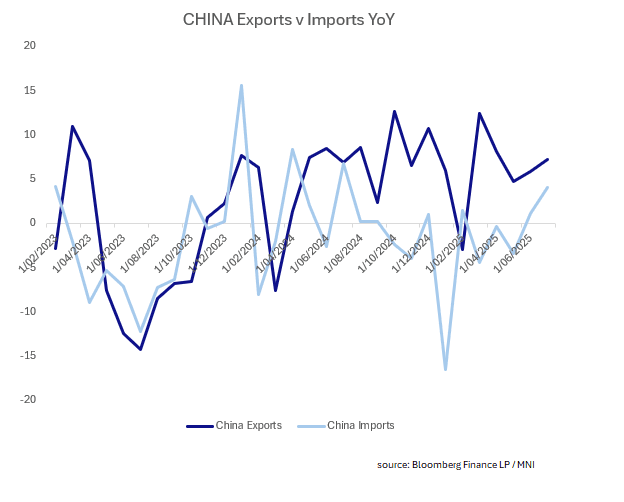

CHINA: Week Ahead: The Macro, Valuation, Sentiment & Technical Lens

Macro: Last week's August PMIs surprised to the upside with manufacturing expanding at +50.5 (forecast 49.8) and services very strong at 53.0. This week's key releases will be the August trade data. Exports for July rose +7.2% and the forecasts for August is currently +5.5% and Imprts +3.4%.

Fig 1: China Trade Data Year on Year

Valuations: The performance of equity markets in recent weeks have seen P/Es at the top end of their full year forecasts and above the average of for the full year over the last 5-years, though lower than the post-COVID highs. Bonds remain well contained with the 10-Yr government bond trading in a 2-3bp range over the last few weeks.

Sentiment: The strength of the equity market has seen people rushing to open equity accounts. Signs of life in the Shanghai real estate market are encouraging, but will need to see a more sustained recovery in multiple key cities. Margin trade account openings have grown, though in context the size of China’s stock market also has nearly doubled in the past decade. The amount of leveraged purchases as a proportion of total market capitalization was 2.2% as of Monday last week, slightly above the 10-year average but far below 2015’s peak of 4.6% (as reported by BBG).

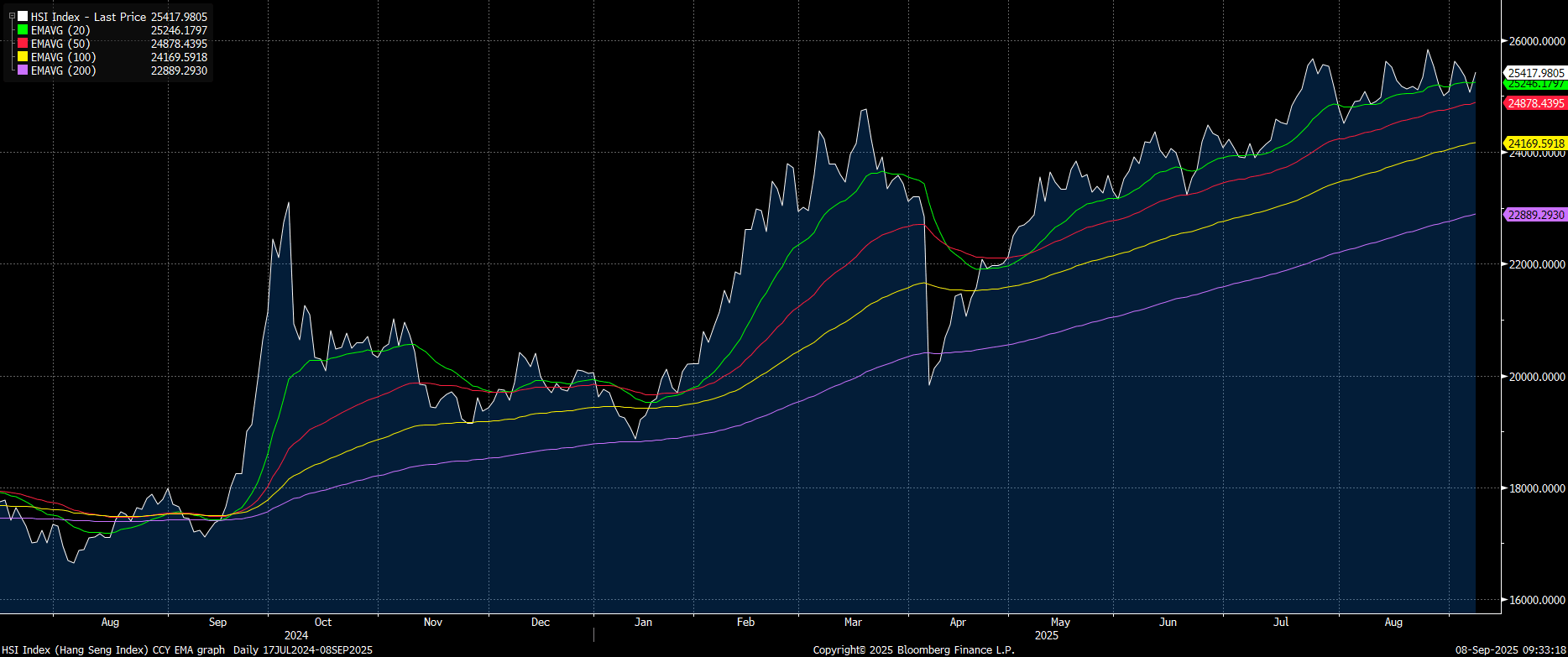

Technicals: Whilst the CSI 300 sits comfortably above the 20-day EMA, the Hang Seng has bounced above and below it in the last fortnight, closing above it last week, and is up +2.2% over the last month, compared to +8.6% for the CSI 300. Government bond issuance for the week ahead sees a barbell approach to maturities.

09/10 : China to Sell 149 Billion Yuan 2030 Bonds

09/10 : China to Sell 35 Billion Yuan 2075 Bonds

Fig 2: Hang Seng vs 20, 50, 100 and 200-day EMA

source: Bloomberg Finance LP / MNI

JAPAN DATA: Q2 GDP Growth Revised Higher, Consumption Up, Capex Down

Japan Q2 GDP revisions were stronger than expected. Headline Q2 GDP rose 0.5%q/q, against a 0.3% expectation (which was the initial print). Nominal GDP rose 1.6%q/q, against a 1.3% forecast. The y/y deflator was unchanged though at 3.0%.

- In terms of the detail, private consumption growth was revised up to 0.4%q/q from 0.2%, but capex was revised to 0.6%q/q growth (from 1.3%). The inventory contribution was flat, versus an initial -0.3pt drag. Exports contribution was unchanged at 0.3%pt.

- It's also likely that public investment improved versus initial estimates. Our policy team noted last week: "Public investment is expected to be revised to flat on quarter from the initial -0.5%."

- The revisions are welcome from a broader growth standpoint. We have now had 5 consecutive quarters of growth (albeit with Q1 only marginally positive at 0.1%q/q).

- The authorities will be hoping that this trend is sustained, with near term focus on the tariff fallout. Its impact on profitability/capex is a BOJ watchpoint, with the next Tankan survey, out at the start of Oct, to help gauge impact.