US TSYS: Poised to Revisit Early Session Lows

* Treasuries are poised to extend session lows after quietly retreating since midday. No obvious h...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Price Pressures Rising But Analysts Still See Scope for Possible Rate Cut

As noted earlier, Chinese PPI inflation jumped to 3.9% y/y in May, marking the highest level since July 2022. Meanwhile, CPI inflation held at 1.2% y/y, marginally below expectations. While therelationship between PPI and CPI has weakened over the last year, higher oil prices remain an upside risk for CPI inflation. Nonetheless, sell-side analysts don’t expect any significant pass-through, and still see scope for potential PBoC easing later this year:

- ING believes that food and property prices are helping suppress headline inflation for now, but that rising prices more broadly suggest we're moving from deflation into a low inflation environment. However, ING don’t expect any significant second round effects this year and believe that the low but positive inflation backdrop isn't likely to impede potential monetary policy easing. They think this is still on the table this year, especially if economic data continue to soften.

- JP Morgan writes that PPI drivers were industrial upgrade/AI demand, reinforced by seasonal strength in coal/cooling-linked categories. They believe that AI-related cost pass-through is broadening, adding a more durable inflation tailwind. However, while PPI has some upside risk, excess capacity and weak demand will limit the pass-through, leaving CPI inflation benign in their view. With core CPI inflation muted around 1% y/y, they expect the PBoC will likely stay on hold for now, although a rate cut could be back on the table in H2 if growth downside risks persist.

- Meanwhile, Goldman Sachs notes that upstream sectors accounted for around 82% of the rebound in year-over-year headline PPI inflation. In terms of the CPI data, higher energy prices were broadly offset by lower food prices. The tick down in core CPI inflation to 1.1% y/y was likely due to softer tourism-related services prices.

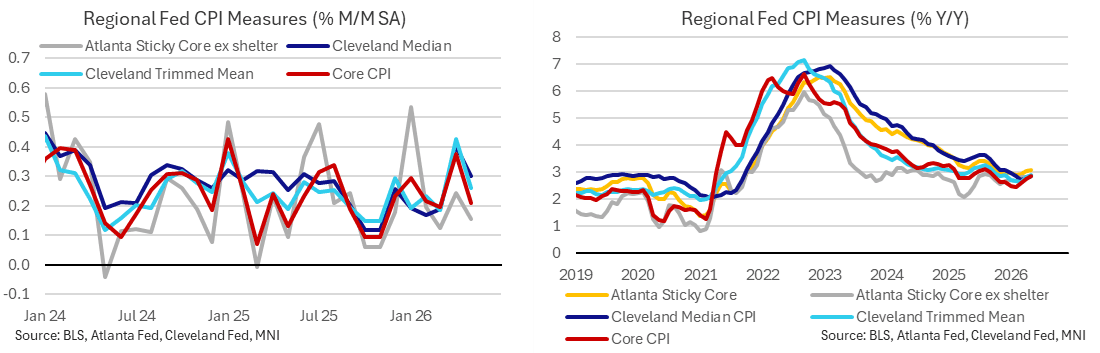

US DATA: Regional Fed CPI Metrics Echo May's Modest Y/Y Acceleration In Core

Regional Fed CPI metrics confirmed an acceleration or at best trend stabilization in Y/Y inflation in May, mostly a little under the 3% handle for only slightly above the 2.85% Y/Y seen for core CPI.

- Core CPI inflation was marginally softer than expected in May at 0.21% M/M (MNI unrounded consensus 0.23, more notable against rounded Bloomberg consensus of 0.3%) whilst headline saw a slightly larger unrounded miss at 0.47% M/M (MNI unrounded consensus 0.51).

- Median and trimmed mean monthly inflation was stronger than core in May according to the Cleveland Fed although these measures were very similar in Y/Y terms to the 2.85% for core.

- The Cleveland Fed median CPI accelerated marginally to 2.85% Y/Y in May (highest since Feb) from 2.80% in April. It’s broadly stabilized at an average 2.80% Y/Y through Feb-May via a low of 2.72% in March.

- The Cleveland Fed trimmed CPI has seen a stronger recent acceleration meanwhile, most recently firmed to 2.91% Y/Y in May (highest since Dec 2025) from 2.83% in May and a low of 2.64% in April (lowest since Apr 2021).

- Alternatively, the Atlanta Fed sticky CPI firmed marginally to 3.12% Y/Y (highest since Sep 2025) from 3.07% in Apr for a slow acceleration from the low of 2.97% in Feb (lowest since Sep 2021). This measure has broadly plateaued for some time now, averaging 3.05% since October.

- The Atlanta Fed sticky core CPI ex shelter measure firmed to 2.89% Y/Y in May (highest since Sep 2025) from 2.82% in Apr, up from a low of 2.56% in Nov 2025.

GBPUSD TECHS: Monitoring Support

- RES 4: 1.3658 High May 1 and a key resistance

- RES 3: 1.3574 76.4% retracement of the May 1 - 18 bear leg

- RES 2: 1.3522 61.8% retracement of the May 1 - 18 bear leg

- RES 1: 1.3448/1.3509 50-day EMA / High May 26

- PRICE: 1.3391 @ 17:07 BST Jun 10

- SUP 1: 1.3303 Low May 18 and the bear trigger

- SUP 2: 1.3277 76.4% retracement of the Mar 31 - May 1 bull leg

- SUP 3: 1.3212 Low Apr 7

- SUP 4: 1.3159 Low Mar 31 and a key support

GBPUSD continues to trade above key short-term support at 1.3303, the May 18 low, however, this level remains exposed. Clearance of it would strengthen a bearish threat and pave the way for an extension towards 1.3277, the 76.4% retracement of the Mar 31 - May 1 bull leg. A break of this retracement point would further strengthen a bearish theme and open 1.3159, the Mar 31 low. Key short-term resistance is at 1.3509, the May 26 high.