US DATA: Personal Spending Consolidates In April, Underlying Income Solid

April private spending was a little better than expected - but personal income was much stronger than anticipated. While there are some worrying signs in terms of consumer momentum, particularly in services purchases, the employee income growth which has driven much of the economic expansion has not shown any signs of abating going into Q2.

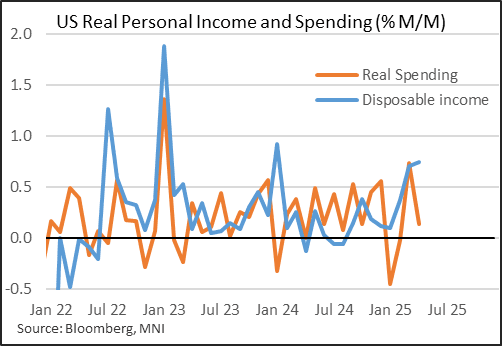

- Real personal spending rose 0.1% M/M in April, a sharp slowdown from 0.7% in March but slightly above the 0.0% consensus. In nominal terms, it was in-line at 0.2% M/M (again after 0.7%).

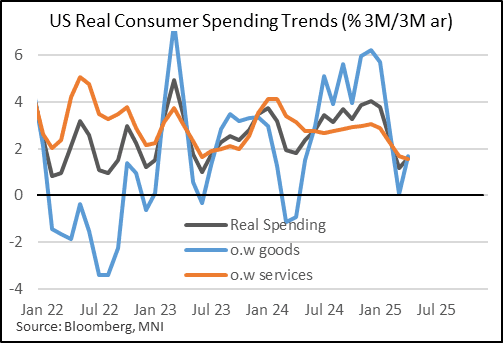

- Overall, spending is running at a nominal 5.5% 3M/3M annualized rate, gaining a bit of momentum since earlier in the year. Real spending is only picking up slowly, at a 1.6% 3M/3M annual rate, though that compares favorably to February's 1.2% which was a 21-month low.

- Real goods consumption contracted by 0.2% after an apparent tariff front-loaded +1.5% in March (still running at a 1.7% 3M/3M rate), with real services purchases dipping to 0.3% from 0.4%. The slowing here is more pronounced on a momentum basis than in goods: 3M/3M annualized real services growth is running at 1.5%, slowest since July 2020 (ie pandemic).

- Income was the big surprise though: it rose 0.8% M/M (in nominal terms) vs 0.3% consensus, with March's revised up to 0.7% from 0.5%.

- Employee compensation - which is 2/3 of income - rose by 0.5% M/M for a remarkably consistent 4th month out of 5. Nominal income is now running at an 8.3% 3M/3M annual rate, which is the fastest since Q1 2024, and has accelerated for 7 consecutive months.

- The jump may prove illusory: personal current transfer receipts stood out for the fastest rise since January 2024, up 2.8% M/M, the bulk of which was Social Security payments (ie government benefits) which will not repeat in terms of future growth. April's bump is very likely reflecting the Social Security Fairness Act, which is upping payments for over 3 million pensioners.

- Either way, real disposable income grew at 0.7% M/M for a second consecutive month, and is growing at a 4.9% 3M/3M annualized clip - likewise the highest since Q1 2024.

- Squaring the circle of soft spending vs high incomes are savings rates: the household savings ratio rose 0.6pp to 4.9% in April, the highest in 11 months. This potentially reflects a lack of consumer confidence in the month, judging from multiple surveys - though we would always take individual months' readings with some caution as they are subject to considerable revisions.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: Real GDP Beats Latest Tracking With Solid Private Domestic Demand

Real GDP was close to expectations in the Q1 advance, although to us that in itself was surprising as there hadn’t been enough time for consensus to fully adjust to a sharp increase in consumer imports in March data released the day before on Tuesday. Hiding beneath some significant crosscurrents from net trade and inventories, private domestic demand was surprisingly little changed from its 2024 average but no doubt with question marks over the extent to which it’s been boosted by tariff front-running.

- Real GDP fell -0.3% annualized vs consensus of -0.2%, a median of 26 analyst estimates updated yesterday of -0.8%, and GDPNow gold-adjusted at -1.5%.

- There were some significant crosscurrents relative to GDPNow expectations.

- In a less positive sign, changes in inventories were much stronger than expected as they added 2.25pps to GDP (GDPNow had 0.3pp) for the largest positive contribution since 4Q21. That should be a large drag going ahead.

- It was partly offset by an even larger drag from net exports of -4.8pp (GDPNow -4.05pp gold-adjusted). Ordinarily that surprise amidst particularly firm import growth would be a positive development but tariff front-running clouds interpretation.

- Looking through these noisier categories, underlying demand signs were encouraging with resilient consumption growth and a bounce in non-residential investment.

- Personal consumption increased 1.8% (cons 1.2), adding 1.2pp to quarterly GDP growth (GDPNow saw 0.9pp or 1.4%). That said it’s still a sizeable moderation from 4.0% in Q4 and 3.1% averaged in 2024 and that’s despite some likely tariff front-running.

- Non-residential investment meanwhile saw a large bounce from a weak Q4, rising 9.8% to add 1.3pp to GDP growth (strongest quarter since 2Q23) after -0.4pp.

- Government spending however was surprisingly negative on the quarter, dragging -0.25pp (GDPNow 0.3pp).

- That combination meant that final domestic demand increased 2.3% in Q1 after 3.0% in Q4 but private domestic demand impressively accelerated a touch to 3.0% in Q1 after 2.95% in Q4, having averaged 3.0% in 2024.

GILTS: UK 10yr Yield level update

- A quick update on the UK 10yr Yield after it cleared the initial 4.46% support.

- Most Investors will now be Watching out for any potential extension towards the April and 2025 low at 4.363%.

Today, reference 93.60:

- 4.363% = 94.36.

STIR: U.S. Data Offsets, 97bp Of Fed Cuts Priced Through Dec

Two-way movements in Fed pricing after the latest rounds of data, with the firmer-than-expected Q1 PCE and personal consumption prints, as well as a Q1 GDP release that wasn’t as bad as many expected in the wake of yesterday’s trade data (-0.3% vs. -0.2% in the BBG median, latter deemed stale in light of yesterday’s data), offsetting the softer-than-expected ADP employment release.

- Zooming out, the Q1 data underscores the stagflationary risks evident in the economy.

- Fed Funds show 2.5bp of cuts for May, 16bp through June, 39bp through July, 60.5bp through September, 78.5bp through October and 97.5bp through year-end.

- That compares to 2.5bp, 17bp, 38.5bp, 60bp, 78bp and 97bp ahead of the data.

- Market briefly priced ~99.5bp of Fed cuts through year-end on the back of the ADP reading, before swing back to ~95bp following the Q1 data.

- Focus now moves to March PCE data, due at 10:00 NY/15:00 London.