AMERICAS OIL: Ovintiv to Acquire NuVista Energy

Ovintiv plans to acquire NuVista for C$17.80/share, or ~$2.7 billion, in a 50/50 stock-cash transaction.

- The deal is expected to close by the end of 1Q2026.

- OVV stated the deal is expected add ~140,000 net acres and ~100 Kboe/d to their oil-rich Alberta Montney acreage.

- The acquisition is expected to bring ~930 total net 10,000-foot equivalent well locations at an average cost of $1.3 million per location according to the release.

- The company also plans to begin a divestiture from its Anadarko assets in 1Q2026, which it secured with the Newfield acquisition in February 2019.

- Ovintiv currently owns ~9.6% of NuVista’s outstanding shared previously purchased in a private transaction for C$16/share.

- The cash component of the transaction will be funded though a combination of OVV’s cash on hand, borrowings under the credit facility, and/or proceeds from a term loan.

- Additionally, OVV will pause their share buyback program for two quarters to fund a portion of the cash proceeds.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (Z5) Reversal Lower Extends

- RES 3: 95.960 - High Apr 7 (cont.)

- RES 2: 95.875 - High Jul 2 (cont.)

- RES 1: 95.780 - High Sep 12, 18 and 19

- PRICE: 95.640 @ 15:49 BST Oct 03

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

Aussie 10-yr futures are trading closer to their recent lows. It is still possible that the recent move down is a correction. Near-term resistance to watch is 95.780, the Sep 12 high. A clear break of this level would signal scope for a continuation higher and open 95.875, the Jul 2 high on the continuation chart. On the downside, key short-term support to watch has been defined at 95.510, the Sep 3 low. Clearance of this level would instead be bearish.

OIL: Crude Higher On Monday Following Careful OPEC Output Increase

Oil has started today over a percent higher after OPEC+ decided to increase output by 137kbd from November, in line with October’s move. There had been some speculation last week that it could have been larger which helped to drive prices sharply lower. They were down over 7% last week but stabilised on Friday in a narrow range. The more cautious OPEC supply move has reassured the market at this stage as excess supply is expected.

- WTI rose 0.4% on Friday to $60.69/bbl but was still down 7.7% last week. The benchmark reached $61.38 before declining to $60.55. It breached the bear trigger at $60.85 on Thursday and remains below that level. WTI is currently up 1.4% to $61.72/bbl today.

- Brent was up 0.4% to $64.36/bbl after a high of $65.02 and then a low of $64.20, the bear trigger. It fell 7% on the week. Initial resistance is at $69.87.

- With a market surplus expected from the end of 2025, OPEC’s decision was cautious as it continues to gradually unwind previous output reductions. The group is trying to regain market share but most members have limited spare capacity except Saudi Arabia.

- According to Bloomberg there were some dissenting views with Russia arguing that prices needed to be protected and Algeria that demand could weaken.

- The OPEC+ decision for December will be made on November 2.

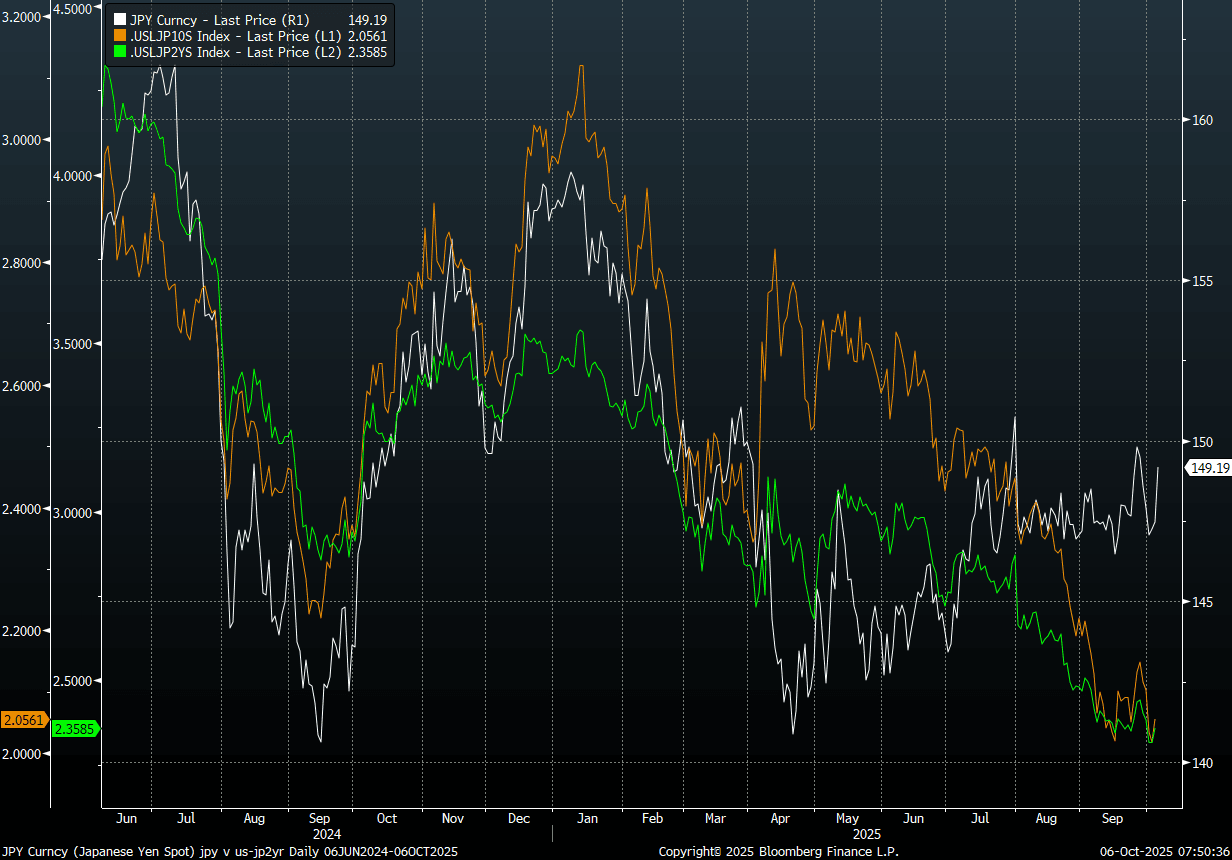

JPY: US-JP Swap Rate Differentials Not Arguing For Sustained 150 Break

For USD/JPY a key focus focus point will be the BoJ outlook, given Takaichi's comments around the central bank's policy decisions in the past (along with remarks post Saturday on the need for the government and BoJ to be closely aligned on economic policy). A test above 150.00 can't be ruled out for USD/JPY in the near term (session highs rest at 149.62 today, after closing last Friday at 147.47). Still, as we note below swap rate differentials with the US are not arguing for a sustained break above 150.00 at this stage. Asset manager position shifts are likely to be as well, given they have build up a long JPY position in recent monhts.

- From a technical standpoint, 149.69, the Sep 26 high and bull trigger, is a key upside focus point in the near term. Beyond that 150.92 is the Aug 1 high. On the downside, the Oct low 1 is back at 146.59.

- In terms of broader macro trends, US-JP yield differentials will likely to continue to dictate broader risks in the pair. At the current juncture, yield differentials are just up from cycle low. At face value, this is not arguing for a surge above 150.00, as the market remains focused on Fed easing risks.

- Focus may also shift to US-JP swap rate differentials, given JGB yields could be heavier influenced by the local fiscal outlook in the near term (rather than BOJ expectations. The chart below plots USD/JPY versus US-JP 2y and 10y swap rate differentials.

- From a positioning perspective, asset managers have built up a JPY long position, while leveraged players have been short. Latest data shows Asset managers at +79.2k net longs, while leveraged names were -63.4k net short. Hence fresh upside in USD/JPY is likely to be dictated by whether asset managers scale back longs/shift back to an outright short.

Fig 1: USD/JPY Versus 2yr & 10yr Swap Rate Differentials

Source: Bloomberg Finance L.P./MNI