COMMODITIES: Oil and Gold Fall into the Fourth of July

- In a market where liquidity was low ahead of the US holiday, stronger than expected jobs data and the ongoing discussions from OPEC+ about an increase supply were enough to push oil lower.

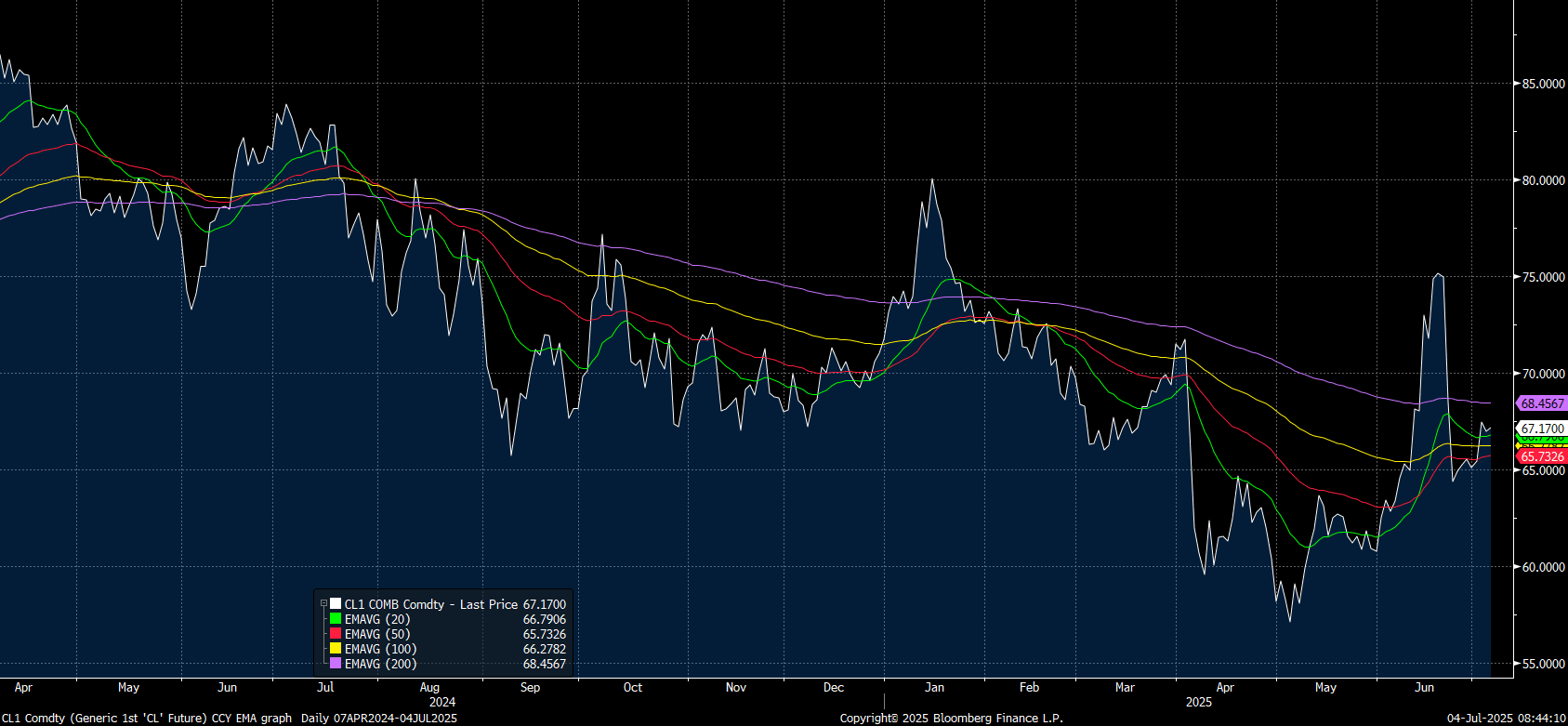

- WTI finished the US session at US$67.17 bbl, down -0.67% and wedged between the 20-day EMA of $66.78 and the 200-day EMA of $68.45.

source: Bloomberg Finance LP / MNI

- Brent finished down -0.45% at $68.86 and remains between the converged 20-day and 100-day EMA of $69.23 and the 50-day EMA of $68.45.

- American refiners are relying on oil supplies from the country’s biggest shale basins more than ever as flows of denser varieties from places like Mexico and Canada ebb. US drillers are using the lightest oil on record, according to recent government data, leaning heavily on shale formations in Texas, New Mexico and North Dakota. The shift comes as heavy crude supplies are strained by falling production from Mexico, a trade spat with Canada and a de facto US ban on imports of Venezuelan oil. (source BBG)

- China avoided purchasing US crude for the third straight month — the longest stretch since 2018 — delivering a fresh blow to shale drillers already facing lower oil prices.

- Iranian oil output reached a 46-year high in 2024 and is expected to increase again this year, despite US oil sanctions. The country's energy sector has emerged unscathed, with energy export revenue hitting a 12-year high of $78 billion last year.

- Gold had a tough night following strong US data posing questions for the path of interest rate cuts.

- Gold finished the US session at US$3,326.12, down -0.93%.

- Gold remains up 27% this year on safe haven demand and as the world approaches the July 9 deadline for trade deals with the US, gold investors will watch carefully for any outcomes of discussions. US President Trump has said that a deal has been reached with Vietnam which sets a tariff of 20% on Vietnamese exports and 40% on transshipped goods, the latter likely aimed at China.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Modestly Richer Despite US Tsys Finishing Modestly Cheaper

In local morning trade, NZGBs are 2bps richer despite US tsys finishing ~2bps cheaper across benchmarks. The NZ-US 10-year yield differential is -4bps at +13bps.

- US tsys finished well off early session bests after higher-than-expected JOLTS job openings and an up-revision to prior openings.

- The JOLTS report for April was, on balance, one of relative stability in another look at early reaction to Trump administration policies. Job openings surprisingly increased (7391k (sa, cons 7100k) in April after a marginal upward revision of 7200k (initial 7192k) in March), while the hire rate pushed to its highest since September. However, the quit rate pushed back lower again after what to us was a surprising uptick back in March.

- S&P e-minis were just off May 29 highs after the White House announced that President Trump will sign 50% steel and aluminium import tariffs on Wednesday.

- Swap rates are 2-3bps lower.

- RBNZ dated OIS pricing is little changed across meetings. 6bps of easing is priced for July, with a cumulative 30bps by November 2025.

- Today, the local calendar will be empty.

- On Thursday, the NZ Treasury plans to sell NZ$200mn of the 3.00% Apr-29 bond, NZ$200mn of the 4.50% May-35 bond and NZ$50mn of the 5.00% May-54 bond.

JPY: USD/JPY - JPY Bulls Made To Wait

The overnight range was 142.61 - 144.11, Asia is currently trading around 143.95. The USD continued from where it left in Asia and was well bid the whole overnight session, retracing nearly all of Monday’s move lower.

- Bloomberg - “Japanese PM Shigeru Ishiba is considering dissolving the lower house of parliament if the opposition submits a no-confidence vote during the current session through late June, local media reported.”

- Reuters - “Japan to promote domestic ownership of JGBs, policy draft shows.” reut.rs/4ktcZY4

- This would have been a frustrating day for the JPY Bulls, though I suppose in hindsight the market should not have been expecting any clear breaks until the NFP data on Friday.

- The market still seems very confident of a move lower in USD/JPY but with positioning quite large now we have seen the risks of pullbacks increase. Resistance around the 146.00 area held perfectly and the JPY bulls would be quite relieved as well as vindicated by the price action.

- A break below 142.00 in USD/JPY and all eyes will once again turn to the pivotal 140.00 area. Sellers should emerge on this bounce back towards the 144.00/145.00 area now.

- Options : Close significant option expiries for NY cut, based on DTCC data: 143.50($698m), 145.00($629m). Upcoming Close Strikes : 140.00($2b June 5), 142.00($1.17b June 5), 148.00($1.21b June 5).

- CFTC data shows Asset managers maintained their already extensive JPY longs, and leveraged funds reduced their longs that had just started to be built up.

Data/Event : Jibun Bank Japan PMI's

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

JGB TECHS: (M5) Rallies Off Lows

- RES 3: 147.74 - High Jan 15 and bull trigger (cont)

- RES 2: 146.53 - High Aug 6

- RES 1: 141.48/142.95 - High May 2 / High Apr 7

- PRICE: 139.01 @ 16:09 GMT Jun 03

- SUP 1: 138.54 - Low May 22

- SUP 2: 136.57 - 1.382 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

- SUP 3: 134.89 - 2.000 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

JGBs have rallied off recent lows, however a bearish theme remains intact following the reversal that started Apr 7. A continuation lower would signal scope for an extension towards 136.57, a Fibonacci projection. On the upside, a reversal higher would instead refocus attention on 142.95, the Apr 7 high. The first important resistance to watch is 141.48, the May 2 high. A break of this level would be viewed as an early bullish signal.