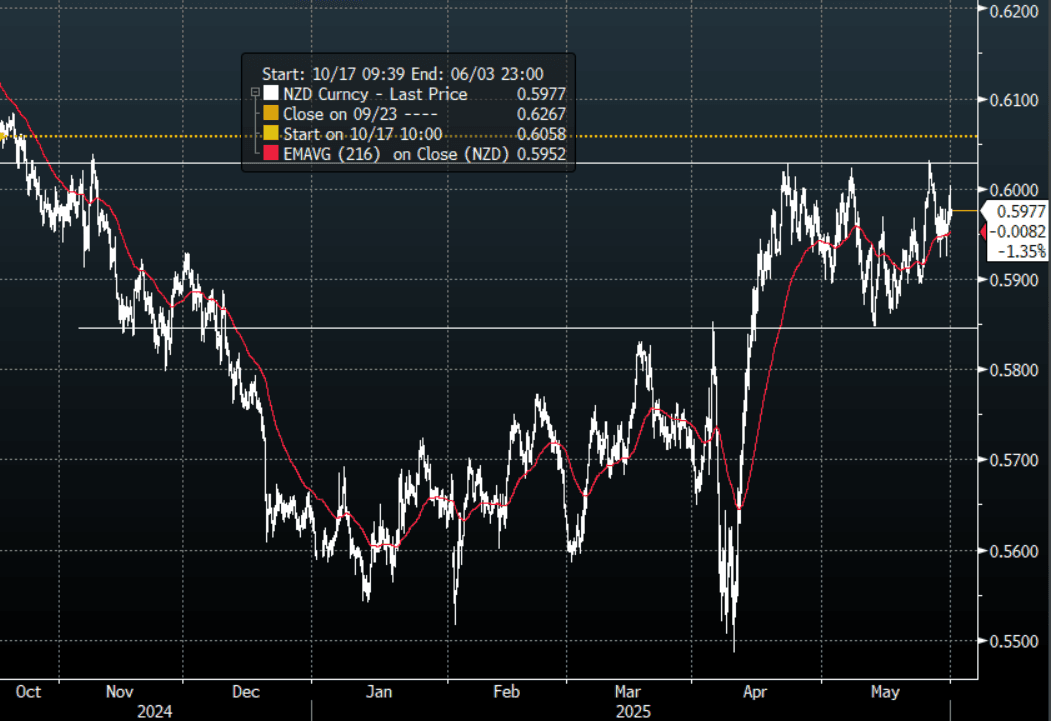

NZD: NZD/USD - Eyeing The Highs Above 0.6000 Once More

The NZD had a range overnight of 0.5932 - 0.5992, Asia is trading around 0.5975. The NZD has bounced like everything else as the USD move was reversed overnight. Good demand was seen back towards the 0.5900 area once more as focus now returns back to the highs above 0.6000.

- A federal appeals court offered President Donald Trump a temporary reprieve from a ruling threatening to throw out the bulk of his sweeping tariff agenda, offering at least some hope to a White House now facing substantial new restrictions on its effort to rewrite the global trading order.

- NZ MAY CONSUMER CONFIDENCE INDEX FALLS TO 92.9: ANZ

- NZ MAY CONSUMER CONFIDENCE FALLS 5.5% M/M: ANZ" - BBG

- The NZD continues to trade in a 0.5850/0.6050 range, the hawkish slant from the RBNZ has probably seen a good portion of the new shorts added last week by leveraged accounts pared back.

- The support back towards 0.5800/50 has held very well, and while this continues to hold expect buyers to be around on dips. A break above 0.6050 is needed to provide the spark for the next leg higher.

- CFTC Data showed Asset managers maintaining their shorts, while the leveraged community added a decent clip back to their own short.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6100(NZD375m June 3), 0.5900(NZD401m June 4)

Data/Event : Building Permits

Fig 1: NZD/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: US Crude Stocks Build While Products Keep Falling

Bloomberg reported that there was a US crude inventory build of 3.8mn barrels last week, according to people familiar with the API data. 674k barrels were added at Cushing. Products continued to destock with gasoline down 3.1mn and distillate 2.5mn. The official EIA data is out on Wednesday.

AUSSIE 10-YEAR TECHS: (M5) Remains Toward Top End of Recent Range

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.960 - High Apr 7

- PRICE: 95.805 @ 16:05 GMT Apr 29

- SUP 1: 95.420/95.300 - Low Feb 13 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.640 - 1.0% 10-dma envelope

Aussie 10-yr futures extended a recent strong bounce through to the Friday close, putting prices through the top end of the recent range. The confirmed breach of 95.851, the Dec 11 high on the continuation contract, reinstates a bull cycle and focuses attention on resistance at 96.207, a Fibonacci retracement point. A stronger bearish theme would expose 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition.

CNY: ING On Differences In FX Markets Between Now and 2018/19 Period

The bank highlights the differences in FX markets between current and the first trade conflict between US and China

ING: "There are some key differences between the first and second trade wars for the FX market.

- First and most importantly, the first trade war took place during a Federal Reserve rate hike cycle, which prompted a strong dollar environment; the dollar index rose around 12.2% between the 2018 low and the 2019 high. The second trade war takes place during a rate cut cycle, prompting a weaker dollar environment, and the dollar index is already down around 9.9% from this year’s high.

- Secondly, the first trade war featured relatively smaller tariff measures, which were partially absorbed by exporters and importers cutting margins, and generally was seen as more damaging to China than the US. Many Chinese firms were ill-prepared for a trade war, given the narrative at the time was that high levels of interdependence would prevent a trade war. The second trade war is of a much larger scale and threatens not just the economic outlook for China but also the US. Recession risks in the US generally look higher than in China this time around.

- Thirdly, the past few years have featured a significantly different backdrop for asset allocation and capital flows. In the past few years, we saw heavy capital inflows to the US after the rate hikes and the tech boom, while China has seen capital outflow pressure and a period of entrenched pessimism. The hot money available to flow out of each market is markedly different compared to 2018.

- Fourthly, China’s focus on currency stability has strengthened in recent years. Compared to 2018, more Chinese companies are also expanding outward direct investment, and the yuan’s role as a settlement currency has expanded. Maintaining consumer confidence and domestic purchasing power is also increasingly important given the pivot toward boosting domestic demand."