FED: NY Fed Plans Regular Early Repo Operations Soon

NY Fed SOMA Manager Perli at the 8th Short-Term Funding Markets Conference in Washington, D.C. said that the NY Fed’s plans to move to a regular provision of early repo operations to enhance effectiveness of monetary policy implementation and market functioning. He also notes no evidence of basis trade unwind amidst the “real and significant” deterioration in Treasury liquidity in April. See full remarks here.

- “A key point that I would like to emphasize is that, although liquidity in Treasury cash markets became strained in early April, those markets continued to function, in part because of the resilience of funding liquidity in the Treasury repo market.”

- Regular early repo operations to be offered soon: Having run test operations, including through Mar 27 – Apr 2 to span quarter-end, and following primary dealer consultations, “the Desk plans on making early-settlement SRF auctions part of the regular SRF daily schedule, at some point in the not-too-distant future. These early-settlement auctions, combined with the current afternoon auctions, will enhance the effectiveness of the SRF as a tool for monetary policy implementation and market functioning.”

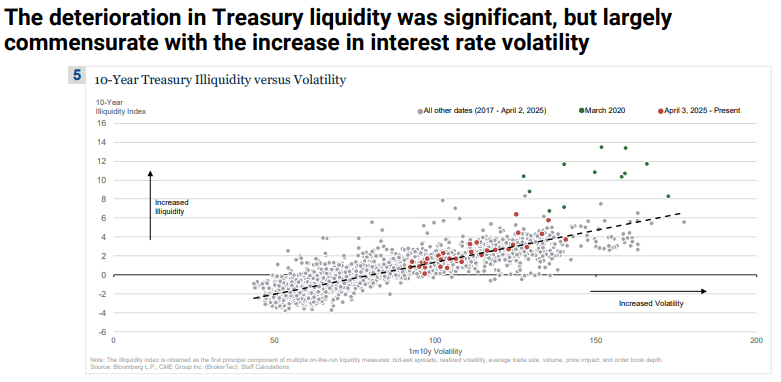

- April deterioration in Treasury liquidity: “The deterioration in Treasury market liquidity was real and significant. Still, it was not exceptional, in the sense that it was largely commensurate with the increase in interest rate volatility.”

- No evidence of unwind of the basis trade in April: One rough proxy for hedge funds’ basis trading volumes stood at about $1 trillion in March 2025, “well above levels observed in February 2020. The sudden unwind of those trades could have been an additional and significant source of market instability due to associated selling pressures that could have overwhelmed dealers, whose balance sheet capacity was already limited.”

- “One factor that could lead to a rapid unwind of the basis trade is substantial repo rate volatility or a persistent increase in repo rates, which could in turn increase the cost of financing the position and therefore make it unprofitable. But this by and large did not happen in April since repo rates were fairly stable and dealers remained willing and able to intermediate. As a result, according to Desk staff’s estimates, the basis remained relatively stable. This stands in sharp contrast to March 2020, when the basis jumped by about 100 basis points and the unwinding of basis trades was likely an important contributor to the sharp dislocation in the Treasury market we observed at that time.”

(Corrected location of conference from Iceland)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: Put spread seller

0RM5 98.125/97.9375ps, sold at 5.5 down to 5.25 in 10k.

STIR: Growth Concerns Support Euribor; Monday's High Contains Upside In ERZ5

Monday’s high of 98.335 has contained upside in ERZ5 for now, with the contract +10.0 ticks at 98.310 at typing. Clearance of Monday’s high would mark the highest level since August 2022, and expose trendline resistance drawn from the January 2024 high (98.3705 today) as the next topside target.

- Euribor whites are 4.0 to 10.0 ticks higher, while blues remain weaker alongside core FI, down 0.5 to 4.5 ticks.

- The announcement of fresh Chinese retaliation against US tariffs has exacerbated existing global growth concerns. Brent crude and natural gas futures have seen an associated sharp pullback, which has fed through into EUR traded inflation metrics.

- Together, this has allowed the market to re-position for a more aggressive ECB easing cycle.

- Hawkish comments from ECB’s Holzmann were fully in line with his previous stance, with more attention paid to dovish rhetoric from Rehn, Villeroy and Escriva earlier (alongside a dovish Reuters sources article referencing the larger-than-anticipated growth hit caused by the US tariff announcement).

- Earlier today, Morgan Stanley adjusted their ECB call to a 1.5% deposit rate by year-end (compared to June 2026 in their prior forecast).

- ABN AMRO remain at the dovish end of the analyst spectrum, expecting 100bp of rate cuts across the next four meetings to a terminal of 1.50%, with risks skewed towards more easing.

EURGBP TECHS: Continues To Appreciate

- RES 4: 0.8715 The Dec 28 ‘23 high

- RES 3: 0.8700 Round number resistance

- RES 2: 0.8683 1.764 proj of the Mar 3 - 11 - 28 price swing

- RES 1: 0.8660 Intraday high

- PRICE: 0.8646 @ 14:03 BST Apr 9

- SUP 1: 0.8470/0.8415 Low Apr 7 / 20-day EMA

- SUP 2: 0.8377 50-day EMA

- SUP 3: 0.8316 Low Mar 28 and a key near-term support

- SUP 4: 0.8299 Low Mar 5

EURGBP continues to appreciate as the impulsive bull rally accelerates further. A key resistance at 0.8625, the Aug 8 ‘24 high, has been cleared. The breach highlights another important technical break and strengthens a bullish condition. Sights are 0.8683 next, a Fibonacci projection. Firm support lies at 0.8415, the 20-day EMA. Note that the cross is in extreme overbought territory, a pullback would allow this condition to unwind.