US TSYS/SUPPLY: No Shutdown For Auctions In October (1/2)

From our latest Treasury Deep Dive (PDF Here): Most attention in Washington D.C. is on the federal government shutdown that began on October 1, but the Department of Treasury will largely carry on business as usual given its many so-called “essential” functions.

- That includes Treasury auctions, which will continue uninterrupted however long the shutdown persists. (And perhaps needless to say, Treasury will continue to service existing debt as usual.)

- There has been some tweaking in the T-bill department. While Treasury greatly exceeded its end-Q3 cash target with a total of $890B on September 30, vs $850B targeted in the August refunding, there was an unexpectedly early increase in auction bill sizes to start the month: 4-week by $5B to a record $105B, 8-week also by $5B to a joint-record $90B, and 4-month by $2B to a record $67B. $5B upped in 6W and $2B in 13 and 26W.

- Most expectations we'd seen were for bill sizes to remain relatively steady until later in October – a month that typically sees bill upsizing - so this is coming a little early.

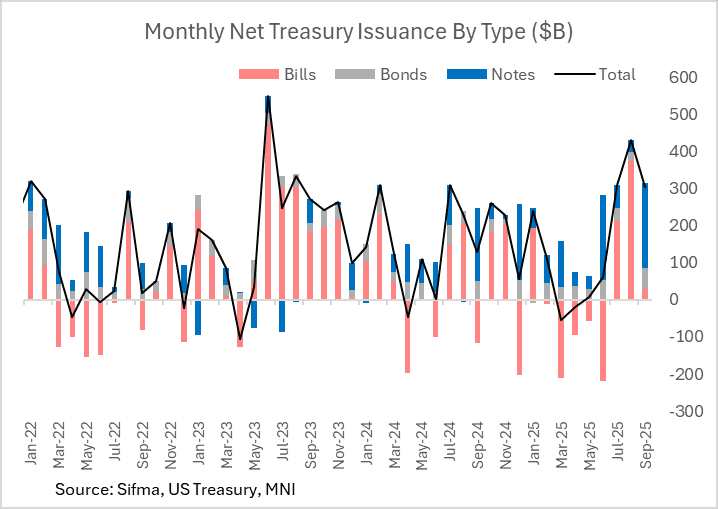

- Total net issuance in September in terms of cash raised (per Sifma data) was $304.1B, with Bills making up just $28B of that – albeit that’s after close to $600B of issuance in the prior two months with August easily the high watermark of the year ($373B) as Treasury aggressively rebuilt cash reserves. That effectively reversed the $596B negative net bill issuance in February through June under the debt limit.

- Bill issuance in October is expected to run close to the $182B (net) seen in the same month of 2024.

- We wouldn’t necessarily take it as a sign of net fiscal receipt concern in the first month of the new fiscal year, but it does remind that Treasury has kept nominal auction sizes on the backburner (haven’t been upsized since May-Jul 2024). Current expectations are for no change until well into 2026.

- It is of course only weeks to the next quarterly Refunding announcement (Nov 5), with attention in the interim on the questions to Primary Dealers ahead of the announcement due out on Oct 17. In the past it’s provided some hints as to the upcoming Refunding announcement themes, including on buybacks.

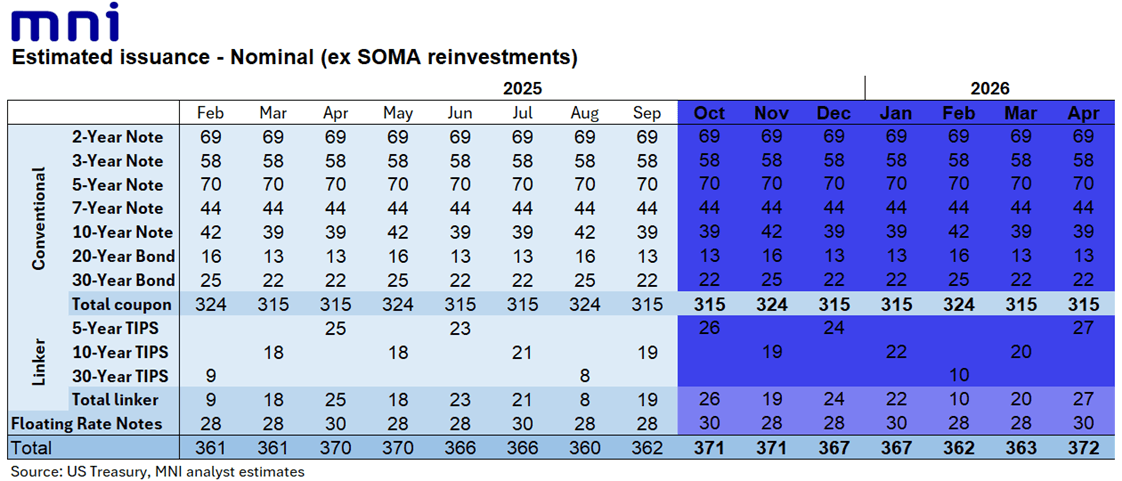

- Upcoming issuance: October’s issuance schedule is set to see $315B in nominal Treasury coupon sales (unch from Sept), in addition to $26B in 5Y TIPS (up $1B from prior) and $30B FRN (unch from prior quarter) for a total of $371B. That’s the highest for any month since October 2021.

- Sales for the month start on Tuesday Oct 7 with $58B of 3Y Note, Wednesday Oct 8 with $39B of 10Y Note reopen, and Thursday Oct 9 with $22B of 30Y Bond reopen.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Thursday Could Prove Eventful For Board Developments

Thursday could prove eventful for Fed Board developments, with Governor nominee Miran testifying before the Senate banking committee at 1000ET, and a potential decision by the judge in Governor Cook's lawsuit against her "firing" by President Trump (a judgment had been anticipated to come as soon as Tuesday but the judge gave the Justice Department until Thursday to file another brief).

- We've fielded some client questions about whether the Trump administration could nominate a replacement for Gov Cook while she disputes her firing - the answer increasingly appears to be "no".

- Politico quotes Republican Senator Tillis as telling reporters today “I’m not going to consider anybody until that’s been adjudicated". That could effectively rule out a Cook replacement being named for now: Tillis is on the Senate banking committee on which the Republicans have a 13-11 majority, so without his support it is hard to see them confirming a new nominee.

- Per Politico, Tillis said: “I’m going to leave it to the courts to decide whether or not it’s legal... But if in fact it is to be for cause, it’s dubious whether or not — even if these events are as they’ve been described — [they’re] a basis for cause. If it’s a move to really kind of create a partisan divide in the Fed, then I’m against it on that basis....I have no interest in moves that would make the Fed really come under direct control of the executive branch."

- It's still unclear however whether Cook will participate in the September FOMC meeting that starts in just under 2 weeks' time.

FED: Beige Book: Inflation Pressures Broadening (3/3)

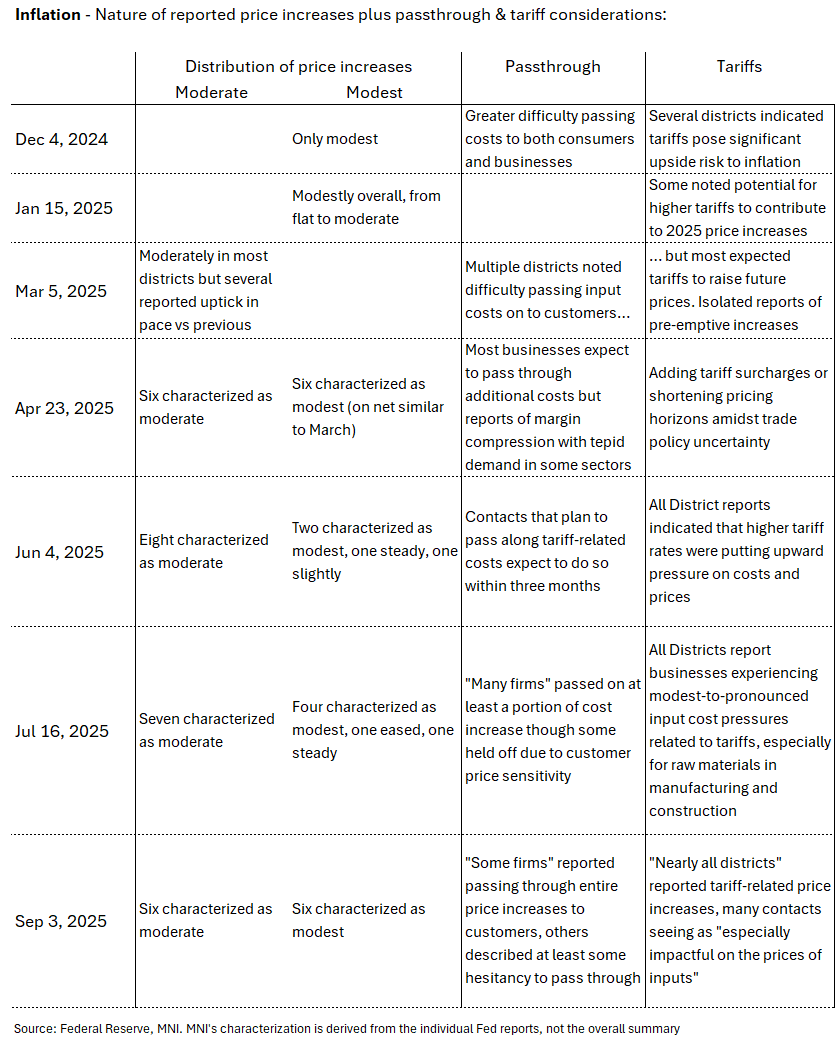

Inflation: The August Beige Book notes "ten Districts characterized price growth as moderate or modest. The other two Districts described strong input price growth that outpaced moderate or modest selling price growth." The latter two appear to be New York ("Selling prices rose moderately, marking some acceleration since the previous period") and St Louis ("Prices have increased moderately since our previous report, but at a faster pace than in previous months").

- The report notes that "nearly all Districts noted tariff-related price increases, with contacts from many Districts reporting that tariffs were especially impactful on the prices of inputs".

- In terms of tariff passthrough, "while some firms reported passing through their entire cost increases to customers, some firms in nearly all Districts described at least some hesitancy in raising prices, citing customer price sensitivity, lack of pricing power, and fear of losing business. In some cases, as highlighted by Cleveland and Minneapolis, firms reported being under pressure to lower prices because of competition, despite facing increased input costs."

- As with the previous reports, there were expectations that price increases still lay ahead: "Most Districts reported that their firms were expecting price increases to continue in the months ahead, with three of those Districts noting that the pace of price increases was expected to rise further."

US TSYS: Late SOFR/Treasury Options: Second Half Puts Fading Underlying Bid

SOFR & Treasury options remain mixed late Wednesday, both leaning towards puts in the second half. Underlying futures scaling off late session highs. Projected rate cuts have gained vs. morning (*) levels: Sep'25 at -23.8bp (-23bp), Oct'25 at -37.7bp (-35.9bp), Dec'25 at -58.5bp (-55.4bp), Jan'26 at -70.2bp (-66.9bp).

- SOFR Options:

- +12,500 SFRV5 96.00/96.12/96.25/96.37 call condors, 4.75

- +5,000 SFRZ5 96.25/96.50 1x2 call spds, 1.75 vs. 96.24/0.05%

- over 5,000 0QH6 96.50/96.75 put spds vs. 3QH6 96.25/96.50 put spds, 0.75 net steepener

- +4,000 SFRZ5 96.06/96.12/96.18/96.25 put condors, 1.75 ref 96.21

- 2,000 SFRV5 96.06/96.18/96.25/96.37 call condors ref 96.21

- -3,500 SFRU5 95.81/95.87/95.93 put flys, 1.75 ref 95.905

- 2,000 SFRU5 95.87/95.93 2x1 put spds

- +22,000 SFRX5 95.93/96.06/96.18 put flys, 2.5-2.75 ref 96.215

- +10,000 SFRU5 96.00/96.12/96.25 call flys, 0.75

- +22,500 SFRU6 97.25/97.50 call spds vs. 96.00 put, 1.0 ref 96.885

- Treasury Options:

- +23,647 wk2 TY 112 puts, 13 vs. 112-20.5 (exp 9/12)

- 2,500 TYV5 110.25/110.5/111.25 broken put flys, 2 ref 112-17

- Block/screen, 20,000 USV5 108/USX5 106 put spds, 7 net/steepener vs. 113-10

- +5,000 UXYZ5 109.5/112.5 put spds, 39

- +4,000 FVV5 110 calls, 22

- over +22,200 TUV5 104.62 calls, 4.5-5.0

- over +16,800 TUV5 104.5 calls, 6.5

- over 19,800 TUV5 104.75 calls, 3.5 ref 104-06.62

- 9,000 Wed wkly TY 112 puts ref 112-02

- 6,000 wk1 TY 112.5 calls, 11 ref 112-04

- 4,000 wk1 TY 112/112.5 1x2 call spds, 3