STIR: Next BoE Cut Still Priced Through Feb

GBP STIR pricing little changed this morning, following yesterday’s hawkish adjustment in the wake of the domestic labour market data.

- A reminder that the data pointed to a slightly less downbeat picture on the quantity side, while wage growth measures were broadly in line with expectations.

- BoE-dated OIS shows no movement for September, 10bp of easing through November, 16bp through year-end and 26bp through the February ’26 MPC.

- SONIA futures flat to +1.0.

- Prior August lows in SFIZ5 and SFIZ6 remain untouched despite yesterday’s hawkish adjustment.

- Fiscal issues continue to dominate local headlines. Guardian sources have reported that “the Treasury is looking at ways to raise more money from inheritance tax amid growing pressure on the country’s finances ahead of the autumn budget”.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Sep-25 | 3.969 | +0.2 |

Nov-25 | 3.865 | -10.2 |

Dec-25 | 3.807 | -16.0 |

Feb-26 | 3.704 | -26.3 |

Mar-26 | 3.656 | -31.1 |

Apr-26 | 3.573 | -39.4 |

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: JPY Outperforms, BBDXY Higher

The BBDXY continues to edge higher in early London trade, with the index registering the firmest level of July.

- The USD bid comes in the wake of an equity sell off and U.S. President Trump’s weekend tariff threats against both the EU & Mexico.

- The theme of broad-based USD selling alongside fresh tariff news has abated in recent sessions, with the market already short USD and broader sentiment against the greenback already operating well into negative territory.

- Markets seem to be taking a more balanced view on the odds of tariffs being implemented & subsequent impact global growth risks.

- The greenback outperforms all G10 FX peers outside of the JPY, which Is seemingly drawing support from lower equities and higher long end JPY rates, leaving USD/JPY ~15 pips lower at 147.30.

- EUR/USD threatens a clean break below the 20-day EMA (1.1660), with lows of 1.1651 registered in early Asia trade.

- Note that dovish commentary from BoE Governor Bailey and a soft REC jobs report (detailed earlier) haven’t resulted in meaningful underperformance for sterling on the major GBP crosses.

- Little of note on the broader G10 calendar for Monday, outside of some ECBspeak from Cipollone & Vujcic.

- Tomorrow’s U.S. CPI data provides the data highlight of the week, with UK CPI (Wednesday) & labour market (Thursday) data also eyed.

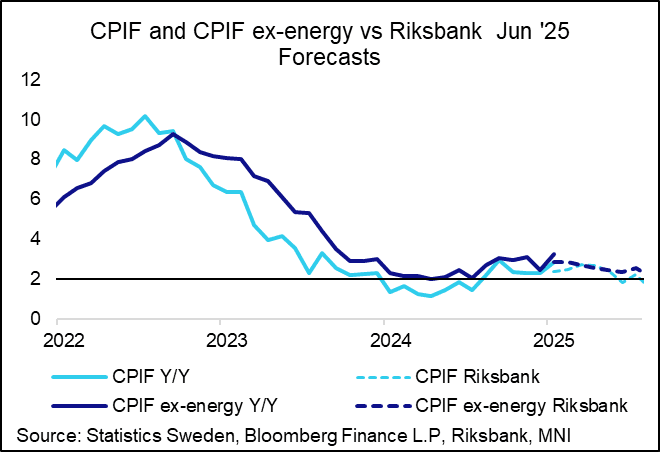

SWEDEN: Package Holidays A Key Factor In June Inf, But Firmness Elsewhere Too

A 0.01pp downward revision to Swedish headline CPIF inflation to 2.84% in June was enough to bring the rounded print down to 2.8% Y/Y (vs 2.85% flash, 2.26% prior). CPIF ex-energy was 3.28% Y/Y (vs 3.29% flash. 2.47% prior), so still 0.4pp above the Riksbank’s June MPR projection. As expected, the start of the Swedish holiday season pushed inflation on package holidays, airfares and accommodation/restaurant inflation higher. Meanwhile, there was fairly limited disinflation to note elsewhere in services, and core goods inflation also appears a little firmer than expected.

- Overall, the print appears strong even after accounting for the expected volatile factors. It will be worth monitoring these trends in the coming months. SEK appreciation earlier this year and subdued demand is still expected to contain inflationary pressures during the summer/autumn – as suggested by forward-looking indicators.

- Package holidays rose 31.08% M/M, contributing 0.49pp to monthly CPI. On an annual basis, prices still fell 1.10% Y/Y (vs -2.68% prior), implying a 0.40pp contribution to annual CPI due to the higher basket weight in 2025.

- Airfares rose 24.03% M/M, contributing 0.05pp to annual CPI. Annual airfare inflation was -2.08% Y/Y (vs -11.27% prior), but actually pulled annual CPI down by 0.17pp on net. Restaurant and hotels inflation accelerated to 4.62% Y/Y (vs 3.28% prior).

- There was fairly limited disinflation in other major services categories:

- Personal care was steady at 2.86% Y/Y (vs 2.85% prior), while insurance and financial services were essentially unchanged.

- Recreation and cultural services rose to 4.08% Y/Y (vs 2.50% prior).

- However, the communication component eased to -1.34% Y/Y (vs -0.71% prior), and rents also softened to 4.71% Y/Y (vs 4.92% prior).

- Within goods, although summer sales pulled down clothing inflation by 2.20% M/M, on a Y/Y basis clothing accelerated to 2.76% Y/Y (vs 1.95% prior). Footwear and furniture inflation also ticked higher. Meanwhile, vehicle purchase inflation was 0.39% YY (vs 0.45% prior).

- Food inflation also rose to 4.26% Y/Y (vs 4.09% prior) – still below March/April levels.

EQUITY TECHS: E-MINI S&P: (U5) Bulls Remain In The Driver’s Seat

- RES 4: 6402.44 1.382 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6381.00 1.764 proj of the Apr 7 - 10 - 21 price swing

- RES 2: 6356.12 1.236 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6335.50 High Jul 10

- PRICE: 6265.00 @ 07:25 BST Jul 14

- SUP 1: 6246.25 Low Jul 7

- SUP 2: 6201.21/6054.38 20- and 50-day EMA values

- SUP 3: 5811.50 Low May 23

- SUP 4: 5645.75 Low May 7

The trend condition in S&P E-Minis remains bullish and short-term weakness is considered corrective. Recent activity has resulted in a break of resistance at 6128.75, the Jun 11 high. The breach confirmed a resumption of the uptrend that started Apr 7. This was followed by a break of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA, at 6054.38.