GERMAN AUCTION RESULTS: New 2.50% Nov-32 Bund

Aug-27 09:34

| 2.50% Nov-32 Bund | |

| ISIN | DE000BU27014 |

| Total sold | E4bln |

| Allotted | E2.675bln |

| Avg yield | 2.46% |

| Bid-to-offer | 0.79x |

| Bid-to-cover | 1.19x |

| Avg Price | 100.26 |

| Low Price | 100.24 |

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: Early Weakness Reversed, EGBs Lead

Jul-28 09:33

Core global FI markets reversed the Asia-Pac gap lower, with the inflation readthrough in the wake of the U.S.-EU trade deal and some ongoing questions surrounding trade between the two eventually outweighing any growth boost when it comes to bonds.

- Benchmark global equity index futures have eased back from Asia-London handover highs but remain comfortably firmer on the day.

- Bund futures as high as 129.74, bulls unable to test the 20-day EMA (129.97). Bears remain in technical control, Friday’s multi-month low (128.84) provides initial support.

- German yields are 2-3bp lower, belly and intermediates outperform. 10s hold below 2.75% after Friday’s brief move above.

- EGB spreads to Bunds little changed to 1bp tighter, aided by firmer equities.

- Gilts follow cues from peers with little in the way of meaningful UK news flow. Futures as high as 91.85, last +31 at 91.77. Initial resistance at the 20-day EMA (91.92) goes untested. Initial support comes in at the July 24 low (91.18).

- UK yields 1-4bp lower, curve flatter. 10s ~1bp wider vs. Bunds.

- ECB & BoE pricing little changed after the recent hawkish adjustments, 16bp of ECB easing showing through year-end, ~46bp of BoE cuts priced over the same horizon.

- Focus is on wider macro matters (any ongoing adjustment to the U.S.-EU trade deal and Sino-U.S. discussions in Stockholm).

- Note the BoE will sell GBP750mln of medium-dated gilts from its APF this afternoon.

- Plenty of EUR event risk as the week moves on, with the ECB’s inflation expectations survey (Tuesday), wage tracking data & (Wednesday), Eurozone GDP (Wednesday) & Eurozone HICP (Friday) all eyed.

EUROPEAN INFLATION: Expectations Not Swayed By Two-Sided Trade Deal Impacts

Jul-28 09:28

- As discussed, there has been little reaction in European front rates to weekend news on the US-EU trade deal with a 15% tariff on EU goods, having already been rumoured last week.

- There is still just 4bp of cuts priced for the Sept ECB, having adjusted from 10bp prior to Thursday’s ECB press conference and subsequent sources pieces pointing to a high bar to a cut next meeting. This had been ~ 12.5bp before headlines earlier in the week on the trade deal nearing.

- Recall Lagarde from the Q&A: "But one thing I will add to that is that the sooner this trade uncertainty is resolved – I think we use the word “resolved swiftly” – so the sooner it is resolved, the less uncertainty we will have to deal with, and that would be welcomed by any economic actors, including ourselves.”

- From a near-term domestic inflation angle, the deal has clearly reduced the prospects of EU retaliation, for which there had been growing support for more penal approaches. Nevertheless, details on the deal more broadly are sparse.

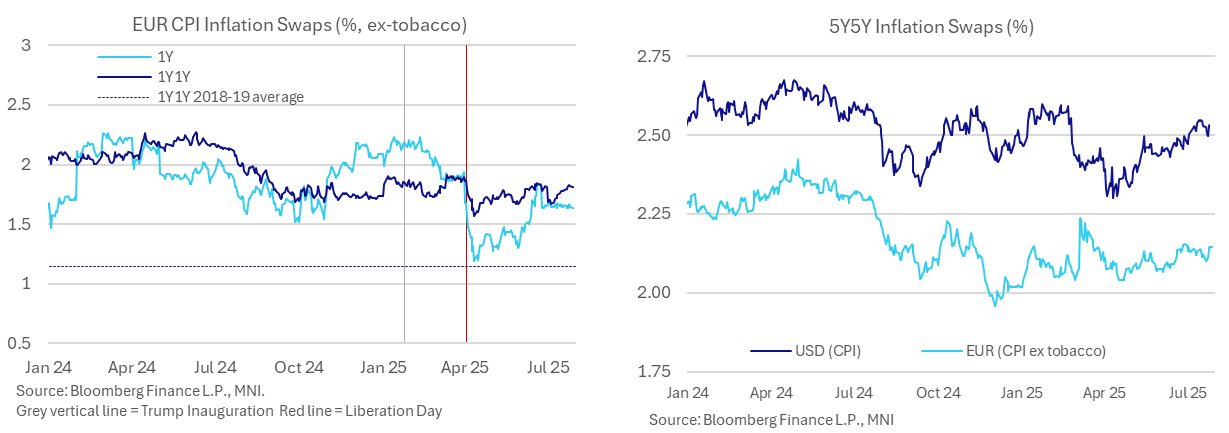

- For now, 1Y inflation swaps are just 0.5bp lower than Friday’s close, at 1.638% a little further off last week’s 1.668% but having broadly kept an unusually narrow range of 1.64-1.69% in July to date.

- 1Y1Y inflation swaps meanwhile at 1.81% are holding their trend climb seen over the month, close to recent highs having average close to 1.9% in the two weeks ahead of early April “Liberation Day” tariff announcements. Whilst still below 2%, as they have been since July 2024, they remain far higher than the tepid 1.1% averaged in 2018/19 pre-pandemic.

- Much further out, 5Y5Y inflation expectations at 2.144% are towards the high end of ranges over the past couple months but with little change over the weekend. This remains comfortably between the ~2.05% seen prior to EU and German fiscal announcements in early March after which they briefly surged to 2.22%.

USD: A strong early performance for the Dollar

Jul-28 09:19

- The Dollar was mostly mixed against G10s going into the European session and just ahead of the EU Cash Govie Open, but as Europe came in, the Dollar saw a Broader base bid, after Desks took in the Overnight Tariff news in their stride.

- The US and the EU agreed a 15% Tariff deal, Europe also agreed to cut its Car Import duty to 2.5% as part of the deal.

- Multiple Desks are still somewhat perplexed at the strength of the Dollar in early trade, and aside from the Trade news, new headlines or drivers have so far been limited.

- Instead some Market participants also speculate that the Fed will stick to its Hawkish stance at Wednesday's Meeting when unchanged Rate is expected from the FOMC, for some of the bid into the Dollar.

- G10 Pairs/Crosses have seen some decent early ranges, the EURUSD sees over a 100 pips range, with the EUR mostly under some small pressure following the fade off the highs in European Equities.

- The Kiwi is the worst early performer within G10 against the Greenback, and the initial support will be seen at 0.5939 in NZDUSD, last Week's low.

- Looking ahead, there are no Tier 1 Data for the session, but the US-EU trade deal details continue to trickle down.