NATGAS: Gas Summary at European Close: TTF Rises

Nov-07 16:45

TTF front month is set for gains today, supported by expectations of higher demand due to cooling weather next week.

- TTF DEC 24 up 2.4% at 41.37€/MWh

- Temperatures in NW Europe are currently still above normal but are forecast to fall below normal next week.

- Hurricane Rafael has passed through Cuba but is expected to wane.

- The U.S. Gulf had shut in 131mmcf/d or 7.04% of gas production BSEE said yesterday.

- Norwegian pipeline supplies to Europe are nominated at 332.2mcm/d today, according to Bloomberg.

- Net European natural gas storage withdrawals rise to meet demand ahead of colder weather forecast for NW Europe next week.

- European gas storage is down to 94.75% full on Nov. 5, according to GIE.

- Russia’s continued gas transit through Ukraine beyond 2024 will depend on buyer demand, Kremlin spokesperson Dmitry Peskov said

- Malaysia’s Petronas lifted a force-majeure on one of its LNG export facilities Nov. 1.

- Sabine Pass pilots have halted service due to fog, according to Moran Shipping.

- Weak shipping rates across the global LNG market have helped widen the US arbitrage opportunities to Asia, Platts said.

- Global gas liquefaction capacity is expected to grow to about 700m mtpa by 2030 Petronet’s CEO said.

- A global supply glut of LNG is forecast around 2027-2028 but will only last for 2-3 as demand in Asia demand is expected to grow, DGI’s CEO said.

- New Fortress Energy expects to produce slightly lower LNG volumes in Q4.

- European storage and new LNG capacity should be sufficient to cover a potential 15 bcm/y shortfall in Europe’s gas if Russian transit flows via Ukraine cease, Italian grid operator Snam’s CEO said.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: US TSY 3Y AUCTION: NON-COMP BIDS $193 MLN FROM $58.000 BLN TOTAL

Oct-08 16:45

- US TSY 3Y AUCTION: NON-COMP BIDS $193 MLN FROM $58.000 BLN TOTAL

US TSYS/SUPPLY: Preview 3Y Note Auction

Oct-08 16:32

- Tsy futures are trading mixed ahead of the $58B 3Y note auction (91282CLQ2) at 1300ET, 2s-10s firmer vs. bonds. WI is currently at 3.872%, 42.8bp cheap to last month's stop-through sale.

- September auction recap: Treasury futures held near session highs (TYZ4 115-11.5, +10) after $58B 3Y note auction (91282CLL3) traded 1.6bp through: 3.444% high yield vs. 3.456% WI; 2.66x bid-to-cover vs. 2.55x prior.

- Indirect take-up climbed to 78.24% vs. 64.39% prior; direct bidder take-up fell to 11.30% vs. 20.25% prior; while primary dealer take-up slipped to 10.45% vs. 15.35% prior.

- Timing today's 3Y note sale: results will be available shortly after the competitive auctions closes at 1300ET.

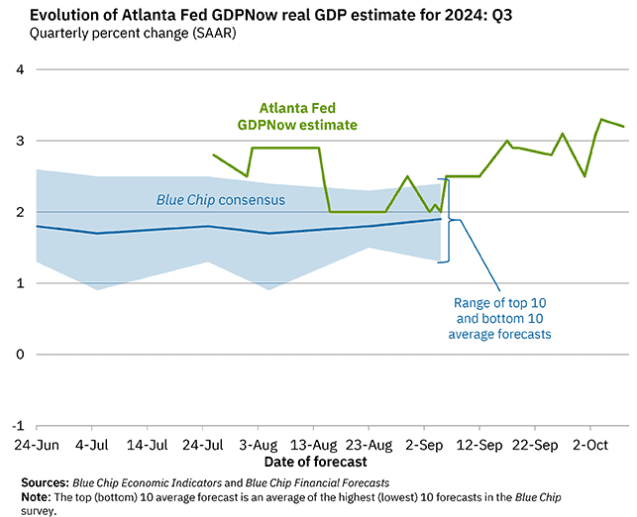

US DATA: Q3 Real GDP Tracking Revised Up To 3.2%, Mainly On ISM Services

Oct-08 16:30

- The Atlanta Fed’s GDPNow tracker for Q3 has been revised higher to 3.2% from 2.54% with the Oct 1 update, leaving a small acceleration from the 3.0% in Q2.

- The bulk of the upward revision came from ISM services (Oct 3) before a modest boost from payrolls (Oct 4) was mostly offset by today’s trade data. The post-payrolls inter-update estimate of 3.3% saw its highest for the Q3 tracker so far.

- Main revisions since the Oct 1 update: real personal consumption seen at 3.3% vs 3.0%, real gross private domestic investment seen at 3.4% vs 0.8% and real government spending seen at 2.2% vs 1.7%.

- The quarterly contribution from personal consumption is strong at 2.22pps, following 1.9pp in Q2 and 1.5pp in Q1.

- Compared to realized Q2 growth, the main outright drags are seen coming from changes in private inventories (0.2pps after 1.05pp) and residential investment (-0.4pp after -0.1pp), whereas the largest sequential boost is seen from net exports (flat after -0.9pps).