AMERICAS OIL: US natural gas stockpiles seen up 46 bcf last week - Reuters

US natural gas stockpiles seen up 46 bcf last week - Reuters

- A Reuters poll indicated US energy firms likely added an above-normal 46 bcf of natural gas into storage last week.

- That compares with an injection of 18 bcf during the same week a year ago and a five-year (2020-2024) average increase of 41 bcf for this time of year.

- If correct, the forecast for the week ended July 11 would increase stockpiles to 3.052 tcf, about 4.9% below the same week a year ago and around 6.2% above the five-year average for the week.

- The EIA is scheduled to release its weekly storage report at 10:30 a.m. EDT (1430 GMT) on Thursday.

- There were 91 total degree days (TDD) last week, compared with the 30-year normal of 82 TDDs for the period, data from financial firm LSEG showed.

- Early estimates for the week ending July 18 ranged from additions of 33 bcf to 48 bcf, with an average increase of 39 bcf.

- That compares with an injection of 20 bcf during the same week last year and a five-year average increase of 30 bcf.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

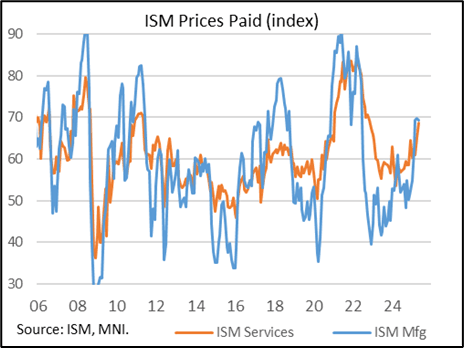

US OUTLOOK/OPINION: Macro Since Last FOMC: Prices - Sharper Increases Expected

- Surveys are indeed pointing to sharp increases in both cost pressures and selling price inflation.

- Business measures have continued to push strongly higher. The ISM services report for May saw prices paid rise further to 68.7 for its highest since Nov 2022, clearly at the expense of new orders which slid to their lowest since Dec 2022.

- This price backdrop was echoed by the S&P Global US services PMI for May reporting that “rising backlogs in part reflected delays in the delivery of ordered equipment due to tariffs, which also drove up cost inflation to its highest in nearly two years. Increased costs were passed on to clients via the steepest increase in output charges since August 2022.”

- Further, the Fed’s Beige Book published June 4th revealed that respondents in all districts indicated higher tariff rates were putting upward pressure on costs and prices and that those that plan to pass tariff-related costs on expect to do so within three months.

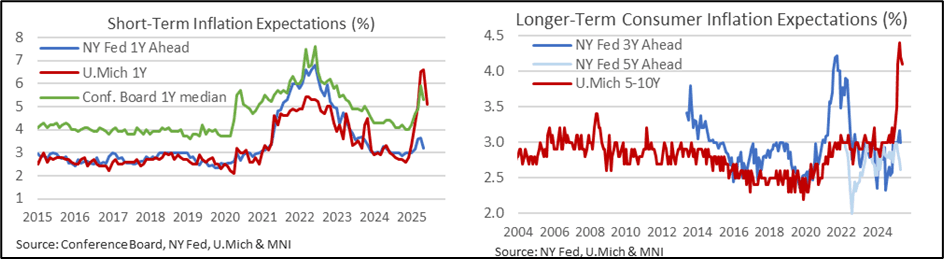

Consumer surveys of inflation expectations meanwhile are off April or May highs although there is a wide range to them. The University of Michigan inflation metrics remain historically elevated despite the 1Y surprisingly cooling in the preliminary June survey, the Conference Board 1Y equivalent is still on the high side whilst the NY Fed’s metrics are far less elevated.

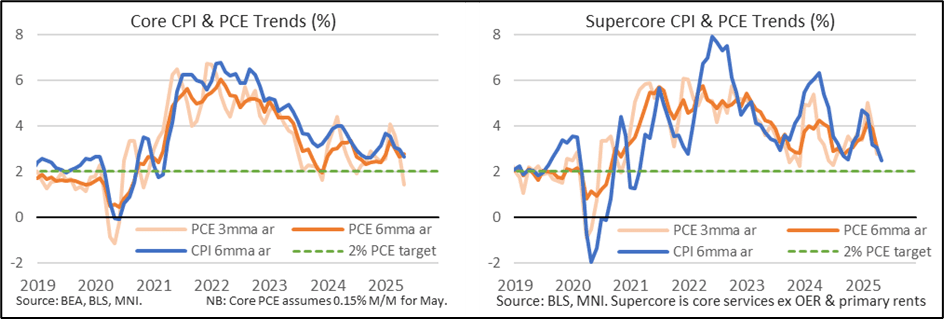

US OUTLOOK/OPINION: Macro Since Last FOMC: Prices - Surprisingly Soft Inflation

- The two CPI reports since the May FOMC meeting surprised lower, the first for April heavily exaggerated by rounding (0.24% M/M vs unrounded consensus of 0.26%) before a large miss for May (0.13% M/M vs 0.27%).

- May’s report started to show some signs of tariff impact across a range of core goods – we estimate the highest median across 56 items since early 2023 – but they were offset by weakness in some heavily weighted items such as new & used cars plus, more surprisingly, apparel. What’s more, core services also surprised softer across both key housing and non-housing components.

- The two PPI reports meanwhile have seen largely benign trends even if trade margins bounced back in May. The PCE-relevant components of PPI were largely neutral on the month in May after a heavy drag in April. That profile has been heavily influenced by portfolio management & investment advice fluctuating on swings in equity markets following US trade policy announcements with near-term strength likely ahead.

- We’re left with core PCE estimates at circa 0.15% M/M for May (released June 27th), which if realized and without revisions would follow 0.12% in April and 0.09% in March. That’s three particularly subdued months, averaging 1.4% annualized, although it would follow what was a worryingly strong 4.1% in the prior three months.

- The Fed will be vary of this volatility in the data whilst acknowledging a still stubbornly high core PCE Y/Y rate of 2.6% currently expected for May, along with strong increases in market-based services PCE inflation at 3.2% Y/Y back in April.

- Further increases in core PCE are expected as greater tariff-driven inflation shows in the summer months although after May’s surprise weakness, questions could start to be asked if there isn’t a stronger increase in next month’s June data.

USDJPY TECHS: Bear Threat Remains Present

- RES 4: 150.49 High Apr 2

- RES 3: 149.28 High Apr 3

- RES 2: 147.67/148.65 High May 14 / 12 and a reversal trigger

- RES 1: 145.46/146.28 High Jun 11 / High May 29 and key resistance

- PRICE: 144.18 @ 17:22 BST Jun 16

- SUP 1: 142.12 Low May 27 and a key support

- SUP 2: 141.96 76.4% retracement of the Apr 22 - May 12 bull leg

- SUP 3: 139.89 Low Apr 22 and a bear trigger

- SUP 4: 138.82 1.50 proj of the Feb 12 - Mar 11 - 28 price swing

USDJPY is trading in a range and remains below last week’s high. Recent weakness suggests the correction between Jun 3 - 11, is over. The trend remains bearish - moving average studies are in a clear bear-mode position, highlighting a dominant downtrend. A resumption of weakness would open 142.12, the May 27 low. Key short-term resistance is 146.28, the May 29 high. First resistance is 145.46, Jun 11 high.