FED: Musalem Reiterates Hawkish Stance, Notes Consumption Tailwinds

Oct-17 17:46

- St Louis Fed’s Musalem (’25 voter, hawk) broadly reiterated recent comments around there being little room to ease monetary policy before it becomes overly loose, with policy somewhere between modestly restrictive and neutral.

- “I could support a path with an additional reduction in the policy rate if there are further risks to the labor market that emerge,” and if the risks for persistent inflation remain contained, Musalem said Friday during an event in Washington. “I do think we need to not be on a preset course.”

- He added “right now, I think it’s particularly important to go meeting by meeting”

- He also offered color on what have been tailwinds for consumption across income spectrums:

- "*MUSALEM: LOWER-INCOME HOUSEHOLD CONSUMPTION IS PRETTY STRONG

- *MUSALEM: LOWER-INCOME HOUSEHOLDS ARE TAKING ON CREDIT TO SPEND

- *MUSALEM: WEALTH EFFECT IS BOOSTING HIGHER-INCOME HOUSEHOLDS" – bbg

- The St Louis Fed team estimates the breakeven job growth rate is between 30-80k.

- The data don’t suggest an imminent labor market deterioration although there is increasing risk of higher unemployment. Broadly, the labor market is around full employment.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ECB: Well Advised To Remain Cautious - Nagel

Sep-17 17:42

- Bundebank President Nagel says in a speech that the ECB is well advised to remain cautious.

- “I consider the decision of the ECB Council 's decision last Thursday to keep key interest rates constant was the right one. We are well advised to remain cautious given the uncertainties. Our approach of making decisions based on data and on a meeting-by-meeting basis has proven successful. With the current monetary policy stance, we are well positioned to respond to unexpected changes.”

- His speech also looks at some structural reasons behind weak German exports amidst a deterioration in competitiveness, including high energy prices, a shortage of skilled workers and supply chain disruptions.

- More broadly on the EU, he adds: "The former ECB- President Mario Draghi has put forward numerous proposals for how Europe can become more competitive. Now it's time to implement these proposals. So far, only a fraction of them have been realized." That broadly echoes Lagarde's growing calls for reform.

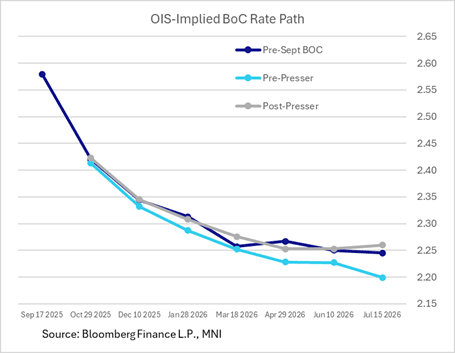

BOC: MNI BoC Review-Sept 2025: Rate Pricing, Analyst Reactions Limited (2/2)

Sep-17 17:28

There are 21bp of cuts priced through year-end, pretty much where pricing came into the rate decision, with the next cut only fully priced by around March – and no more than 2 cuts seen through the rest of the cycle.

- Key to the October decision will be one report each of labour force and inflation data (for September) and the quarterly BOC Business Outlook Survey in the interim. In the meantime, there’s only about a one-in-three market implied probability of a follow-up cut.

Sell-Side Analyst Reaction: There was only one sell-side analyst view change that we saw after the meeting:

- RBC came in expecting the BOC’s easing cycle to already be at an end (including a hold this week), but now appears to see an October cut: “unless there is a drastic turnaround in softening employment trends and easing core inflation in September, we think the likelihood for another cut in the October meeting is high.” Otherwise analysts remain roughly split between whether there will be one or two further cuts – similar to market pricing.

SOFR OPTIONS: Nov'25 SOFR Call Spreaad Buy

Sep-17 17:26

- +25,000 SFRX5 95.62/95.75 call spds, 1.0 vs. 96.325/0.05%