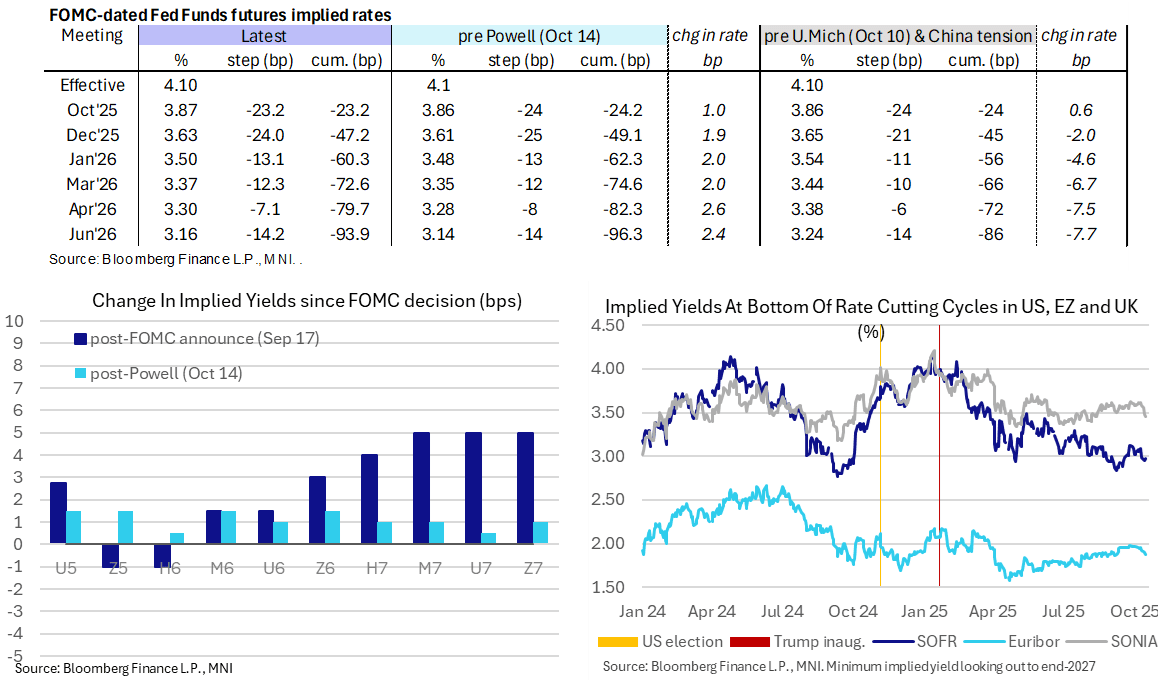

STIR: Most Of Hawkish Tilt Held But Still Close To 50bp Of Fed Cuts To Year-End

Oct-16 14:18

- US rates have only slightly pared a hawkish shift that possibly came on Fed Governor Waller indicating a little more caution in cutting rates beyond October. It’s caveated notably by him earlier today noting that not much has changed since his last speech in late August and him being in the three-cut camp for 2025 in the September SEP – see earlier posts for more color.

- He will look to how solid growth data reconcile with a softer labor market beyond this month’s meeting, but his suite of today’s remarks regularly noted the weakness seen across various labor market sources.

- FF cumulative cuts from 4.10% effective: 23bp Oct, 47bp Dec, 60.5bp Jan, 72.5bp Mar, 79.5bp Apr and 94bp June.

- SOFR futures are now broadly unchanged on the day, giving up an earlier rally with the Z6 for instance 3 ticks lower since Waller.

- Terminal implied yields remain around the Z6/H7 contracts, back to little changed at 2.975% (SFRH7) to keep within a narrow range so far this week with closes between 2.95-2.975%.

- Funding pressures have seen a marked increase in SOFR recently, including +10bp to 4.29% yesterday (14bp above IORB). That came along with the NY Fed accepting $6.75B in yesterday’s O/N repo operation, which has since increased to $8.35bn today.

- Data still ahead: the Dallas Fed weekly economic index at 1130ET whilst state-level jobless claims data should be released in the afternoon ET.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CROSS ASSET: Equities are under renewed pressure

Sep-16 14:15

- European Banking Index (SX7E) and Especially Italian Banks are still leading European Equities lower.

- The Index was sold off on the open and has been under pressure today following a Bloomberg story suggesting that the Italian Government was planning to raise €1.5bn from lenders.

- Unicredit and Intesa Sanpaolo are some of the most weighted within the Index, behind the Spanish BBVA.

- BNP Paribas has been the most weighted but has fallen down somewhat in the ranking.

- In terms of flows for the Emini, 140k lots have traded down since the Cash Open.

- The Price action in Europe has dragged down US Equities and in turn have provided a bid to Bond Futures.

FOREX: Dollar Weakness Extends, EURUSD at Four-Year Highs

Sep-16 14:15

- USD weakness picking up momentum in recent minutes as EURUSD (+0.65%) extends to fresh four-year highs above 1.1829. As noted, the stealthy appreciation leading into the Fed will be providing confidence for those looking for the next leg higher for the pair, with several sell-side analysts continuing to hold strong with year-end forecasts of 1.20 and above.

- Clearance of this hurdle confirms a resumption of the primary uptrend and it’s worth noting the Sep 10 2021 high comes in just above current spot at 1.1851.

- For USDJPY (-0.54%), we are also currently plumbing new session lows at typing, around 146.60. This narrows the gap to key short-term support at 146.21, the Aug 14 low and a bear trigger. A break of this level would highlight a stronger bearish threat and highlight a range breakout.

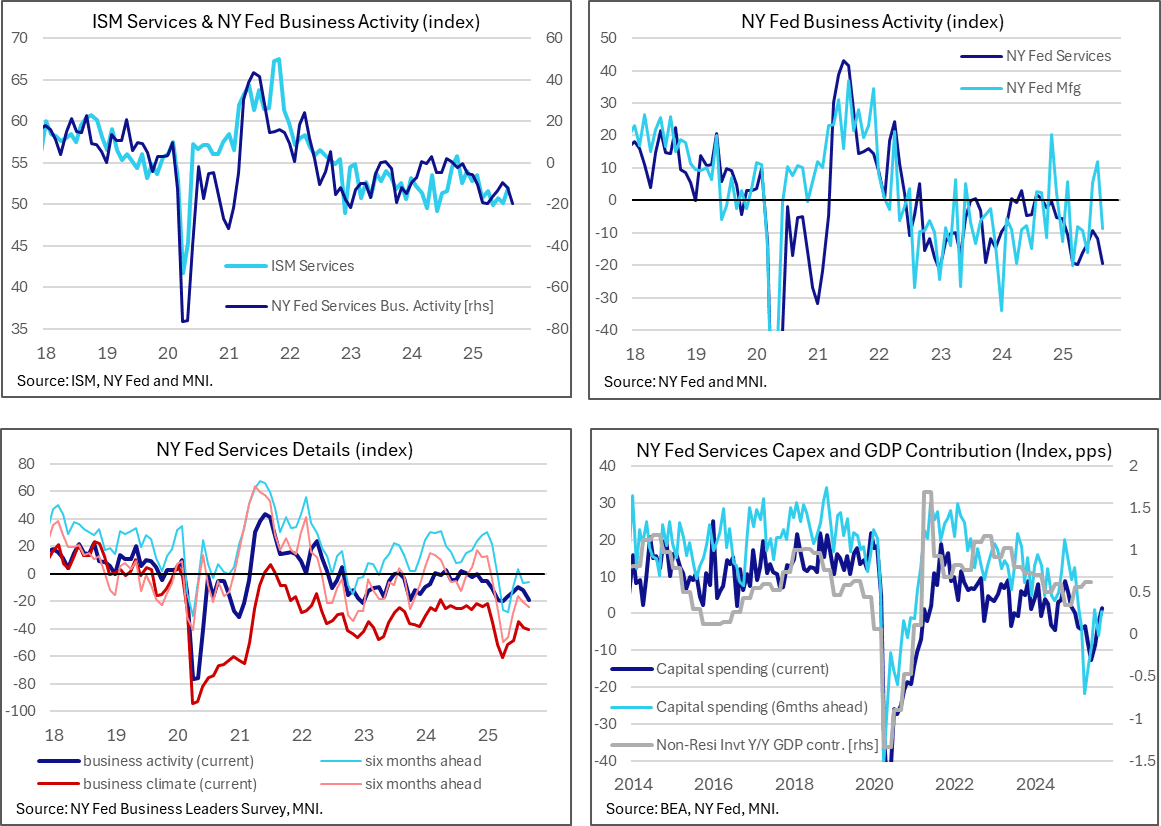

US DATA: NY State Service Firms Echo Manufacturing Weakness In Early September

Sep-16 14:14

Service firms in New York State got off to a similarly weak start to September as their manufacturing counterparts saw yesterday. These are the first September readings for the regional Fed surveys.

- The general activity index surprisingly fell to -19.4 (cons -5.8) in September after -11.7 in Aug to come close to the -19.8 low in April, having last been lower in Jan 2023.

- The six-month ahead measure isn’t as pessimistic though, at -5.8 in Sept after -6.8 in Aug vs a recent low of -28.1 in May.

- In one upside to the report even if not strong, the capital spending index pushed up to 1.4 for its first positive reading since Dec 2024 having recently bottomed at -12.6 in June.

- Other details from the press release: “Employment edged lower, and wage growth remained modest. Supply availability continued to worsen.”

- “Input and selling price increases remained elevated but were little changed from last month. Firms remained pessimistic about the outlook.”

- As with the manufacturing report, the survey was collected through Sep 2-9.