SOUTH KOREA: Mortgages Increase in September

- Given the government's focus on cooling the housing market, particularly in Seoul, today's release of the September Loans to households was worth considering to see if the focus on housing is having an effect.

- However with mortgage loans increasing 2.5t won MoM to KRW932.7 tn at end of September, markets may have to wait awhile longer before the impact shows up in the data.

- South Korea has announced further measures at cooling the sector including tighter loan limits specifically in Seoul, higher risk weights on banks' home loan portfolios and reducing loan to value ratios for purchases.

- "The recent instability in housing markets is spreading on global rate-cut expectations and persistent supply-demand imbalances that are driving concerns over excess capital inflows into real estate," said the Minister of Land, Infrastructure and Transport Kim Yun-duk said in a briefing Wednesday. “In response, we’re going to take preemptive measures to curb instability in the housing market early and to ensure that capital is directed toward more productive sectors of the economy,” he added. (as per BBG)

- Since October the Bank of Korea has cut rate four times but in April went on hold, following the release of the initial policy changes by the then new government. The BOK then cut rats in May and as next meeting approaches, markets remains uncertain with no rate cuts priced in over a one month time horizon and just -6bps over the next three months.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

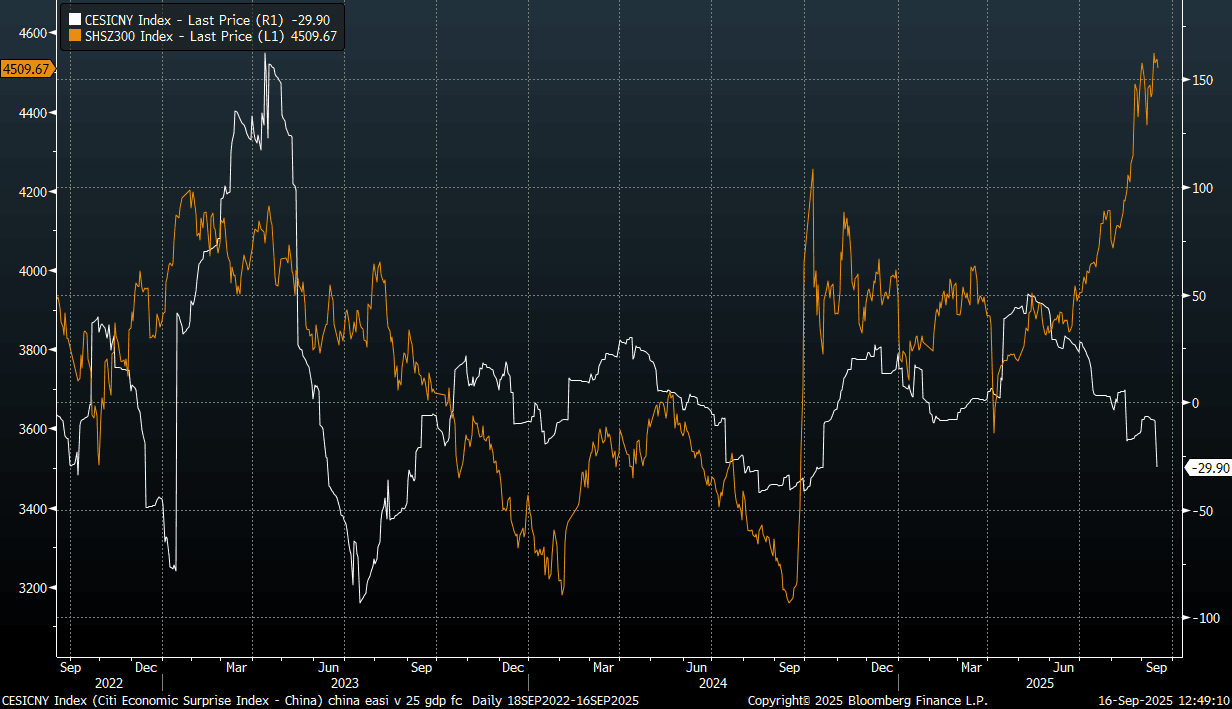

CHINA: China Surprise Index At Fresh 2025 Lows, But Local Equities Supported

Yesterday's softer than expected China data outcomes for August sent the Citi China economic surprise index (EASI) to fresh lows for 2025. It also widened the wedge between this surprise index and China equity trends, see the chart below. Even with mainland China equities down modestly so far today, this only closes the gap a touch (CSI 300 is off around 0.50%).

- To be sure, there have been divergences in the past but usually what we see is positive correlation between the two series, with positive data surprises usually coinciding with higher equity index levels. At face value, concerns around China growth momentum could weigh on equity trends at some stage.

- Still, we may remain divergent in the near term. Firstly, China isn't alone is having softer data outcomes recently relative to expectations. The other major economy EASIs have also softened (although they remain at higher levels relative to the China index). This is impacting these equity markets either, where in the US for example we have hit fresh record highs.

- Focus remains in the tech/AI space. For China the Chinext is up over 40% from start July levels, while the CSI 300 index is up a more modest 15% over the same period.

- The policy shift towards reducing excess capacity in parts of the economy may also weigh on economic activity but aid profitability. This has been a focus in the steel sector in recent months.

- Finally, softer data may encourage views that easier policy settings/economic support will come from the China authorities. Easing Fed expectations has certainly been a support for US/tech led global equity indices in recent months.

Fig 1: Citi China Surprise Index (White Line) and CSI 300 Equity Index (Orange Line)

Source: Citi/Bloomberg Finance L.P./MNI

INDONESIA: MNI Bank Indonesia Preview-Sep 2025: BI Pause, Monitors Events

- Download Full Report Here

- After Bank Indonesia (BI) has had to intervene to defend the rupiah over the last two weeks due to political unrest and then President Prabowo’s decision to remove respected finance minister Indrawati, rates are likely to be left at 5% on 17 September especially given the central bank’s focus on FX stability.

- BI has monthly meetings, so it can be cautious to ensure that the rupiah stabilises, that there aren’t significant portfolio outflows and to monitor political and fiscal developments.

- It expects inflation to stay within its target band this year and next and has eased 125bp so far this cycle and so it can continue to focus on FX stability and be cautious with further rate cuts. We expect it to retain its easing bias.

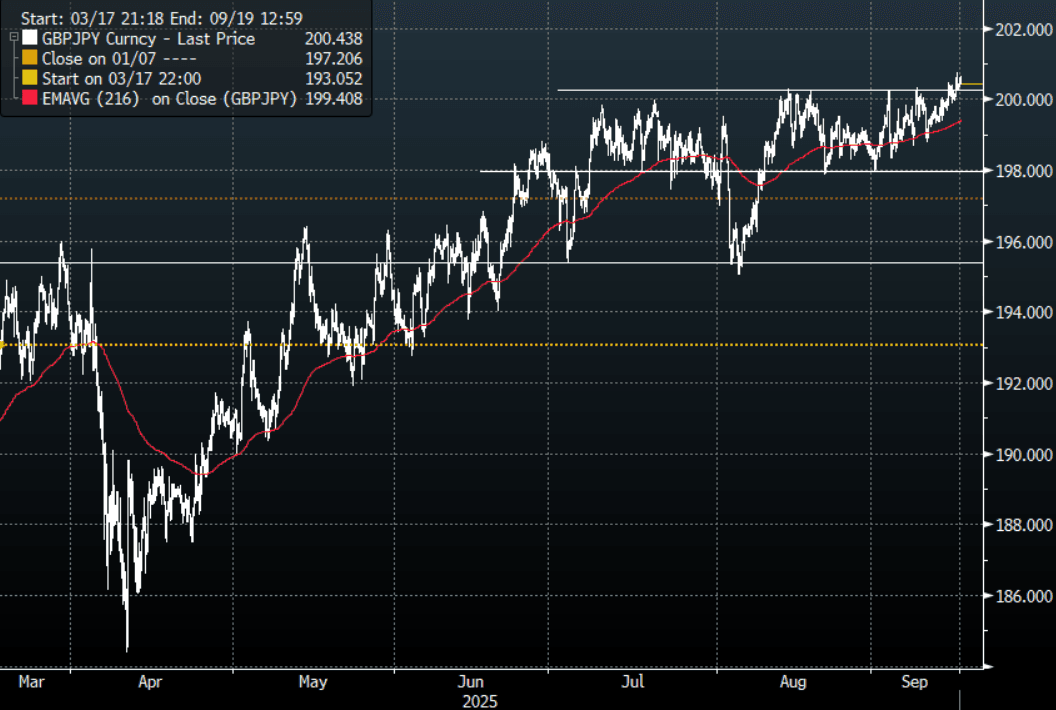

FOREX: JPY Crosses-Grind Higher, GBP/JPY Breaking Above 200.00, FOMC & BOJ Ahead

US Equities continue to march higher and seem to be pricing in a goldilocks scenario regarding what the potential upcoming cutting cycle could look like. This morning US futures have opened muted, E-minis -0.01%, NQU5 +0.05%. The JPY crosses are grinding higher; it still feels like fresh impetus is needed for them to extend. Could the FOMC or the BOJ this week give it the nudge it needs ? GBP/JPY is breaking 200.00, can it extend before we have had the FOMC and BOJ ?

- EUR/JPY - Overnight range 172.91 - 173.19, Asia is trading around 173.30. The pair is grinding back towards 173.50. The range looks to be 171.00-174.00 for now, a sustained break back above 174.00 would look bullish, but I'm not sure I would play it in the cash market until the FOMC and BOJ is out the way.

- GBP/JPY - Overnight 200.03 - 200.74, Asia trades around 200.40. This pair is now making an effort to push above 200.00, a clear sustained break above 200.00 should regain the momentum higher. Can this break accelerate before we get the FOMC and BOJ, tough ask.

- NZD/JPY - Overnight range 87.75 - 88.02, Asia is currently dealing 87.85. The pair continues to stall around the 88.00 area, a sustained move back above 88.00/88.50 and I will have to reassess my bias lower.

- CNH/JPY - Overnight range 20.6743 - 20.7192, Asia is currently trading around 20.7000. This pair has remained above its pivotal 20.30/20.40 support. The pair continues to trade comfortably within its recent 20.40-21.00 range.

Fig 1 : GBP/JPY 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P