MNI US OPEN - Hassett, Warsh on List for Next Fed Chair

EXECUTIVE SUMMARY

- HASSETT, WARSH BATTLE TO BE NEXT FED CHAIR: WSJ

- TRUMP DEAL TO LEAVE EU FACING HIGHER TARIFFS THAN UK: FT

- RBNZ LEAVES OCR AT 3.25%, EYES AUGUST CUT

- CHINA CPI RISES TO FIVE-MONTH HIGH, PPI AT LOWEST SINCE JUNE 2023

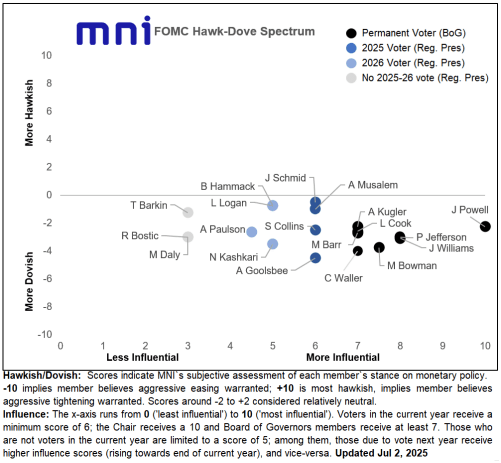

Figure 1: MNI FOMC Hawk-Dove Spectrum

NEWS

MNI FOMC MINUTES PREVIEW - JUNE 2025: Lack of Support for a July Cut

The minutes of the June 17-18 FOMC meeting (released at 2pm ET) should underline the Committee's patience in making its next rate move amid heightened tariff-related economic uncertainty, as encapsulated in the meeting's Dot Plot which showed participants largely divided between no cuts and 2 cuts by year-end. We have heard significant dovishness on the rate front from Board members Bowman and Waller since June's meeting, and while they appear to be outliers, it could be interesting to see whether any other members tend to agree with the view that the incoming tariff inflation will be largely transitory.

US (WSJ): Two Kevins Battle to Be Next Fed Chair in Trump’s ‘Apprentice’-Style Contest

Two Republicans named Kevin are vying to be the next chairman of the Federal Reserve. One is rising to the top of the list of potential candidates, while the other is facing skepticism from President Trump’s allies. Kevin Hassett, one of Trump’s closest economic advisers, is emerging as a serious contender to be the next Fed chair, according to people familiar with the matter. Hassett’s rise threatens the other Kevin—former Fed governor Kevin Warsh—an early favorite for the job who has angled for the position ever since Trump passed him over for it eight years ago. Some people close to the president worry that Warsh, who isn’t in Trump’s inner circle, won’t be a champion of lower rates.

US/EU (FT): Donald Trump Deal to Leave EU Facing Higher Tariffs Than UK

EU negotiators are closing in on a trade deal with Donald Trump that would cement higher tariffs than those granted to the UK, a Brexit dividend that has rattled some European capitals. Brussels is ready to sign a temporary “framework” agreement that sets the US president’s “reciprocal” tariffs at 10 per cent while talks continue, matching the baseline duty imposed on the UK. But the EU is not expecting to achieve the same access to the US market as British steel, cars and other products subject to sectoral duties, according to six diplomats briefed on the issue.

US (WSJ): Trump Delayed Reciprocal Tariffs After Bessent Wanted More Time on Deals

President Trump decided to delay the implementation of his so-called reciprocal tariffs to Aug. 1 after advisers including Treasury Secretary Scott Bessent told him he could get trade deals with more time, according to people familiar with the matter. Administration officials including Bessent felt as if they were making progress on deals with several trading partners such as India and the European Union as Trump’s previous deadline approached, the people said.

US (BBG): US to Start Charging Interest Again on Millions of Student Loans

The Education Department will soon begin to charge interest on student debt for an estimated 7.7 million borrowers who’ve been in legal limbo since a repayment plan created by President Joe Biden was blocked in court. The interest charges for people enrolled in the Saving on a Valuable Education, or SAVE program, will begin on Aug. 1, according to an Education Department official, although, for now, borrowers do not have to resume making loan payments.

US (WaPo): Supreme Court Allows Trump to Launch Mass Layoff and Restructuring Plans

The Supreme Court on Tuesday cleared the way for the Trump administration to launch plans for mass firings and reorganizations at 19 federal agencies and departments while litigation continues. The justices lifted a lower-court order that temporarily blocked plans to lay off thousands of federal workers, including at the State Department and the Social Security Administration, because the administration did not first consult with Congress.

US (WSJ): The Fight Between Musk Acolytes and the White House for Control of DOGE

Elon Musk has left the government, but his clout at DOGE lives on. Weeks after the billionaire left his role at the Department of Government Efficiency amid his feud with President Trump, a small band of Musk loyalists is fighting to preserve the legacy—and power—of the government-slashing office.

US/MALAYSIA (BBG): Malaysia’s Anwar to Seek Lower Tariffs in Meeting With Rubio

Malaysia’s Prime Minister Anwar Ibrahim said he will appeal for lower tariffs when he meets US Secretary of State Marco Rubio on Thursday, after President Donald Trump threatened to impose a steeper rate on the Southeast Asian nation. “The relationship with US has to be maintained, but we will stress that Malaysia is a trading nation, we ask for consideration,” Anwar told reporters on Wednesday.

CHINA/EU (MNI): EU Needs to Readjust Attitude, Not China - China Foreign Ministry

MNI (London) Reuters reports comments from a spox from China's Foreign Ministry regarding trade concerns from the EU. Says that China, "hopes the EU can look at bilateral economic and trade relations comprehensively and positively". Says China "hopes the EU can uphold a more positive and practical China policy." Spox says that the EU "needs to reajust its attitude, not China and not China-EU trade relations." Claims that "the EU's public procurement market is far from being fair and open as the EU claims."

UK (MNI): Probability of Sharp Fall in Risky Asset Prices High

The Bank of England Financial Policy Committee said that the likelihood of sharp falls in risky assets remained high and that overall financial risks were still elevated, but that the domestic picture was more stable with some signs that UK household finances have improved. The record of the FPC's June 27 meeting, published alongside the Financial Stability Report, stated that term premia had risen globally and "the risk of sharp falls in risky asset prices, abrupt shifts in asset allocation and a more prolonged breakdown in historical correlations remains high."

RBNZ (MNI): RBNZ Leaves OCR at 3.25%

The Reserve Bank of New Zealand’s monetary policy committee held the Official Cash Rate at 3.25% on Wednesday, signalling that further easing is likely if medium-term inflation pressures continue to decline as projected. “The economic outlook remains highly uncertain. Further data on the speed of New Zealand’s economic recovery, the persistence of inflation, and the impacts of tariffs will influence the future path of the Official Cash Rate,” the MPC noted in a statement. The RBNZ considered two options at this meeting, to cut by 25bps or hold policy steady.

RBA (BBG): RBA Will Refresh Research Strategy to Support Policy Making

Australia’s central bank intends to refresh its research strategy to support policymaking, Deputy Governor Andrew Hauser said, a day after the Reserve Bank shocked investors and economists with an unchanged interest-rate decision. “Navigating the complex and unpredictable world of tomorrow will pose big new challenges,” Hauser said in the text of a speech on Wednesday.

MALAYSIA (BBG): Malaysia Cuts Rate for First Time Since 2020 After Tariff Threat

Malaysia lowered its benchmark interest rate for the first time in five years, acting after US President Donald Trump increased a threatened tariff on the Southeast Asian country to 25%. Bank Negara Malaysia cut the overnight policy rate by 25 basis points to 2.75% on Wednesday, the first easing since July 2020. Some 13 of 23 economists surveyed by Bloomberg News expected a cut, a slight increase from Monday, with the rest predicting no change.

DATA

CHINA DATA (MNI): June CPI Rises to Five-Month High

- CHINA JUN CPI +0.1% Y/Y VS MEDIAN -0.1%; MAY -0.1%: NBS

China’s Consumer Price Index rose 0.1% y/y in June, ending four consecutive months of decline and reversing May’s 0.1% drop, beating market expectations for a 0.1% fall, according to data from the National Bureau of Statistics released Wednesday. The increase was mainly driven by a rebound in energy prices. On a monthly basis, CPI fell 0.1%, a smaller decline than May’s 0.2%, as energy prices rose 0.1% after falling 1.7% the month before. Core CPI, which excludes food and energy, rose 0.7% y/y, up slightly from 0.6% in May.

CHINA DATA (MNI): Low PPI May Help Global Inflation Pressures, Commodity Prices a Risk

China's PPI downside momentum remained firmly in place for June. We printed -3.6%y/y, the weakest outcome since July 2023. At a time when global inflationary pressures are still elevated, particularly given higher tariff threats, the continued downward momentum in China PPI may provide some further support to downside global CPI momentum. The relationship is by no means perfect, but the correlation in the last 3 years is still running at over 53%.

CHINA DATA (MNI): China Pork CPI Falls in June for First Time

MNI (Beijing) Pork prices in China’s Consumer Price Index declined in June, marking a shift from the positive trend over the first six months of the year, as the overall index rebounded to a 0.1% rise y/y, official data showed on Wednesday. In June, pork prices declined by 8.5% year-on-year and 1.2% month-on-month, reversing the 3.8% growth recorded in H1, the data showed. China’s pork prices are expected to remain negative in H2, eroding one of the already-subdued inflation gauge’s few supports, a government advisor told MNI.

FOREX: USD Index Consolidates Break Above Downtrendline

- Tariffs and trade remain the primary drivers of near-term sentiment, and the President surprised markets again late yesterday in announcing a 50% tariff on copper imports – triggering a near 20% rally in US-listed futures and reminding markets that the White House is not concerned with triggering intraday market vol.

- As such, trade deals and tariffs remain the focus for markets, particularly as even countries that were seen to have sealed agreements with the US – namely the UK – are still subject to tariff risk on August 1st.

- The USD Index is consolidating after the break back above downtrendline resistance drawn off the early February highs earlier in the week. CAD is the poorest performer on the day, while GBP is marginally stronger – but both currencies remain contained inside the recent range.

- The rip higher for EUR/JPY continued apace in APAC trade, with the cross rallying again to touch Y175.43 and the highest level since mid-July last year. This tips the 14-day RSI further into overbought territory, hitting 75 and signalling a further pick-up in upside momentum could be harder to come by without fresh external catalysts in the very near-term.

- Prices are fading somewhat into the NY crossover, however, tipping EUR/JPY off the overnight high and into minor negative territory.

- Final US wholesale inventories and trade sales data for May are the primary data releases Wednesday, however it’s the FOMC meeting minutes due at 1900BST/1400ET that should draw more focus – particularly concerning any discussion among the committee about a possible July rate cut.

EGBS: Topside in Bunds Futures Capped by Equity/Commodity Rally

Bund futures have traded in a relatively contained 35 tick range this morning, with topside seemingly limited by this morning’s rally in European equities and crude oil/gas futures. Bunds are +6 ticks at 129.70, with yesterday’s high at 130.10 untested.

- Markets have mostly looked through yesterday evenings tariff headlines. Although US President Trump’s threat of a 200% pharma tariff would have significant ramifications for the likes of Ireland, Italy and Germany if implemented, the market impact is dampened by (i) Trump’s history of pulling back from his most extreme threats and (ii) yesterday’s comments already suggesting there would be a 1/1.5-year phase in period.

- EGB curves have steepened through July, which has partly been spillover from moves in long-end JGB/Gilt yields. Today’s price action has seen these trends unwind slightly though, with curves lightly bull flattening.

- German yields are up to 1bp lower, despite today’s 15/20-year Bund supply. The Bund results were mixed, with the May-41 line seeing softer cover ratios than the previous outing and the July-44 line seeing stronger demand.

- 10-year EGB spreads to Bunds are within 1bp of yesterday’s closing levels. Portugal also sold OTs this morning.

- Very light regional data calendar today, leaving focus on ECB speakers (Lane, de Guindos, Nagel).

GILTS: Little Changed, Solid Demand at Auction, Curves Back From Highs

Gilts have recovered from session lows after the solid pricing and a decent enough bid-to-cover at this morning’s GBP4.5bln 4.50% Mar-35 auction.

- Light pressure was seen into the bidding deadline, with strength in equities and crude oil markets also factoring into the pre-auction move, which countered the rally seen at the open.

- Futures trade in a narrow 91.54-83 range, last 91.63.

- Bears are in technical control. Initial support at yesterday’s low (91.42), while initial resistance comes in at yesterday’s high (91.98).

- Yields 1.5bp higher to 1.5bp lower, curve flatter.

- 2s10s registered the highest close since April yesterday (75.8bp), while 5s30s registered the first close above 140bp since ’17, but the latter is back below that level this morning.

- Continued digestion of the global trade/tariff backdrop and ongoing negotiations between various countries and the U.S. continue to garner much of the macro focus.

- GBP STIRs essentially unchanged on the day, showing ~51.5bp of BoE cuts through year-end, with 21bp of easing showing for August and 26.5bp priced through September.

- Little to note in the BoE’s FSR, which noted that risks and uncertainty from geopolitical tensions and global fragmentation of trade remain elevated.

- Expect macro & cross-market drivers to remain at the fore during the remainder of the day.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 4.007 | -21.0 |

Sep-25 | 3.951 | -26.6 |

Nov-25 | 3.784 | -43.3 |

Dec-25 | 3.703 | -51.4 |

Feb-26 | 3.576 | -64.1 |

Mar-26 | 3.544 | -67.3 |

EQUITIES: E-Mini S&P Holding Onto Bulk of Recent Gains

Recent gains in Eurostoxx 50 futures from the Jun 23 low still appear to be a potential bull reversal and the contract is holding on to its most recent gains. Price has traded through both the 20- and 50-day EMAs. The clear break of both averages strengthens a reversal theme. This opens 5486.00, the May 20 high and a bull trigger. On the downside, a break of 5194.00, the Jun 23 low, would reinstate a bearish theme. The trend condition in S&P E-Minis remains bullish and the contract is holding on to the bulk of its recent gains. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirmed a resumption of the uptrend that started Apr 7. This was followed by a breach of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA, at 6021.70.

- Japan's NIKKEI closed higher by 132.47 pts or +0.33% at 39821.28 and the TOPIX ended 11.62 pts higher or +0.41% at 2828.16.

- Elsewhere, in China the SHANGHAI closed lower by 4.425 pts or -0.13% at 3493.05 and the HANG SENG ended 255.75 pts lower or -1.06% at 23892.32.

- Across Europe, Germany's DAX trades higher by 180.39 pts or +0.75% at 24385.78, FTSE 100 higher by 7.29 pts or +0.08% at 8861.28, CAC 40 up 60.48 pts or +0.78% at 7827.19 and Euro Stoxx 50 up 38.44 pts or +0.72% at 5410.39.

- Dow Jones mini up 30 pts or +0.07% at 44544, S&P 500 mini up 0.5 pts or +0.01% at 6272.5, NASDAQ mini down 7.25 pts or -0.03% at 22890.

Time: 10:00 BST

COMMODITIES: Recent Weakness in Gold Results in Breach of Support at 50-Day EMA

WTI futures maintain a softer tone following the reversal from the Jun 23 high, and recent gains still appear corrective. Support to watch is the 50-day EMA, at $65.09. The average has been pierced, a clear break of it would signal scope for a deeper retracement. This would expose $58.87, the May 30 low. Initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. Key resistance is at $78.40, the Jun 23 high. Recent weakness in Gold resulted in a breach of the 50-day EMA, and a trendline drawn from the Dec 30 ‘24 low and connected to the Feb 28 low. A clear break of both trend tools would signal scope for a deeper correction, and open $3245.5, May 29 low. Note, the recovery from the Jun 30 low also highlights a possible false t-line break. A resumption of gains would refocus attention on $3451.3, Jun 16 high. The bear trigger is $3248.7, Jun 30 low.

- WTI Crude up $0.54 or +0.79% at $68.89

- Natural Gas down $0.05 or -1.53% at $3.289

- Gold spot down $17.2 or -0.52% at $3284.84

- Copper down $15.7 or -2.76% at $552.85

- Silver down $0.26 or -0.7% at $36.501

- Platinum down $20.74 or -1.51% at $1349.71

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 09/07/2025 | 1000/1100 | BOE FSR Press Conference | ||

| 09/07/2025 | 1045/1245 | ECB Lane At House of the Euro | ||

| 09/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 09/07/2025 | 1100/1300 | EC De Guindos Closing Remarks At Conference | ||

| 09/07/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/07/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 09/07/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 09/07/2025 | 1800/1400 | *** | FOMC Minutes | |

| 10/07/2025 | 0600/0800 | *** | CPI Norway | |

| 10/07/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/07/2025 | 0600/0800 | *** | HICP (f) | |

| 10/07/2025 | 0700/0900 | ECB Cipollone Digital Euro Lecture | ||

| 10/07/2025 | 0800/1000 | * | Industrial Production | |

| 10/07/2025 | - | *** | Money Supply | |

| 10/07/2025 | - | *** | New Loans | |

| 10/07/2025 | - | *** | Social Financing | |

| 10/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 10/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 10/07/2025 | 1400/1000 | St. Louis Fed's Alberto Musalem | ||

| 10/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 10/07/2025 | 1500/1600 | BOE Breeden On Climate Change | ||

| 10/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 10/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 10/07/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 10/07/2025 | 1715/1315 | Fed Governor Christopher Waller | ||

| 10/07/2025 | 1830/1430 | Fed's Mary Daly at MNI |