MNI US OPEN - China Boosts Tariffs Again, But Signals Ceiling

EXECUTIVE SUMMARY:

- CHINA RAISES TARIFFS ON US GOODS TO 125%, BUT SIGNALS NO FURTHER ESCALATION

- WITKOFF TO MEET PUTIN FOR THIRD TIME IN LATEST BID FOR UKRAINE CEASEFIRE

- EARNINGS SEASON KICKS OFF WITH BIG BANKS DUE TODAY

- US-JAPAN TRADE TALKS TO BEGIN NEXT WEEK

NEWS:

US/CHINA (MNI): China Raises Tariffs On US Goods To 125%

The Chinese State Council Tariff Commission has confirmed that China will impose additional tariffs on US goods from 12 April, with the rate increasing from 84% to 125%. This puts it level with the US's 'reciprocal' tariff, although below the total US tariff rate of 145% due to the additional 20% fentanyl-related tariff. Statement here: http://gss.mof.gov.cn/gzdt/zhengcefabu/202504/t20250411_3961823.htm. Excerpts below:

- "The US's imposition of abnormally high tariffs on China seriously violates international economic and trade rules, basic economic laws and common sense, and is completely a unilateral bullying and coercion."

- "Given that at the current tariff level, there is no market acceptance for US goods exported to China. If the US continues to impose tariffs on Chinese goods exported to the US, China will ignore it."

US/RUSSIA (MNI): US Envoy Witkoff In Russia Ahead Of Putin Meeting:

Kremlin spox Dmitry Peskov has confirmed that US Middle East envoy Steven Witkoff has arrived in Moscow ahead of an anticipated meeting with Russian President Vladimir Putin. Axios first reported the meeting earlier this morning. It will be the third time that the two have held in-person conversations amid ongoing talks between US and Russian officials aimed at restoring embassy operations.

EQUITIES: MNI US EARNINGS SCHEDULE - Pre-Tariff Behaviour in Focus

- Financials take early focus this earnings season, with JPMorgan, Morgan Stanley, BNY Mellon, Wells Fargo and BlackRock all set to have reported by the end of this week.

- Markets will be particularly focused on any signs of front-loading corporate purchases ahead of expected tariffs, the rate at which firms will passthrough costs to the consumer and the expected impacts of tariffs on the bottom-line for consumer staples.

- Walmart have already this week withdrawn their quarterly income forecast given the uncertainty surrounding tariffs, however also stated that tariffs provide an opportunity to growth market share.

Full quarterly schedule including EPS, revenue expectations and timings here: https://mni.marketnews.com/4cnn1GO

CHINA/US (MNI): China Can Leverage Procurement To Counter U.S.

China can offset the negative impact of U.S. tariffs by leveraging procurement towards domestic firms impacted by the duties, the Public Procurement Branch of the China Federation of Logistics and Purchasing said on Friday.

CHINA/EU (SCMP): Xi Set to Host EU Leaders in July, South China Morning Post Says

Top European Union officials are making plans to visit China for a meeting with President Xi Jinping, the South China Morning Post reported — a sign Brussels may be keen to develop better ties with Beijing amid the Trump administration’s tariff onslaught.

US (BBG): BofA’s Hartnett Says Sell S&P 500 Rally Until Trade War Abates

Investors should sell any rallies in the S&P 500 Index until the Federal Reserve steps in and the US and China de-escalate the global trade war, according to Bank of America Corp.’s Michael Hartnett. The strategist said President Donald Trump’s tariffs and the resulting market turmoil were turning US exceptionalism into “US repudiation.” He recommends a short position on stocks — until the S&P 500 hits 4,800 points — and a long bet on two-year Treasuries.

US (BBG): Top US Pension Funds Lost $169 Billion After Tariff Shock

The top 25 state and local US pension investment funds suffered an estimated paper loss of $169 billion in public equities after US President Trump’s tariff announcement, according to a report by Equable Institute. For the whole year so far, the top funds have lost an estimated $249 billion, according to the group.

US/SPAIN/CHINA (BBG): Spanish Premier Sticks to China Pivot, Ignores US Warnings

Spanish Prime Minister Pedro Sanchez repeated calls for the European Union to deepen ties with China, brushing aside warnings from the US that it would be detrimental to do so. It’s “necessary to build a positive relationship between Spain and China,” Sanchez said in a press conference in Beijing Friday after meeting with Chinese President Xi Jinping. “Spain and the European Union defend the same principals, the same values and the same interests.”

US/JAPAN (MNI): Econ Min To Meet w/Treasury Sec & USTR 17 Apr For Tariff Talks -NHK:

Japan's NHK reporting date for Minister for Economic Revitalisation Ryosei Akazawa's visit to Washington, D.C., for trade talks with US officials. According to NHK's sources, Ryosei will hold talks with US Treasury Secretary Scott Bessent and US Trade Representative Jamieson Greer on Thursday 17 April.

MNI speaks to the Bank of China's chief researcher about U.S. Treasury bonds.- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

MNI INTERVIEW: White House Warns China Not To Devalue Yuan

MNI obtains exclusive comments from White House on China and FX policy -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

DATA:

UK GDP is estimated to have grown by 0.5% in February, with growths in all main sectors,with the growth coming on an upwardly revised flat growth in the previoius month, the Office for National Statistics said Friday. Real GDP is estimated to have grown by 0.6% in the three months to February, compared with the three months to November, mainly because of growth in the services sector.

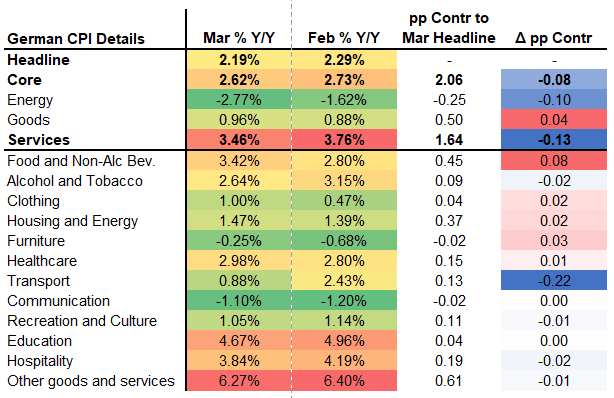

EUROPEAN INFLATION: German Services Moderate But Still Elevated in March

German final March HICP was unrevised from the flash readings at 2.3% Y/Y (2.6% prior) and 0.4% M/M (0.5% prior). The final reading of national CPI was also unrevised at 2.2% Y/Y (2.3% prior) and 0.3% M/M (0.4% prior). Core CPI printed at 2.6% Y/Y (0.1pp upwardly revised, 2.7% prior), the lowest rate since June 2021.

- Overall, the CPI data confirms a notable deceleration in services Y/Y inflation (a -0.13pp smaller contribution than in February) but with a caveat that it was mostly driven by airfares with the Easter holidays in April this year vs March last year.

- Goods inflation slightly accelerated (+0.04pp contribution vs prior) as softer energy was not quite able to cancel out firmer food / core goods inflation.

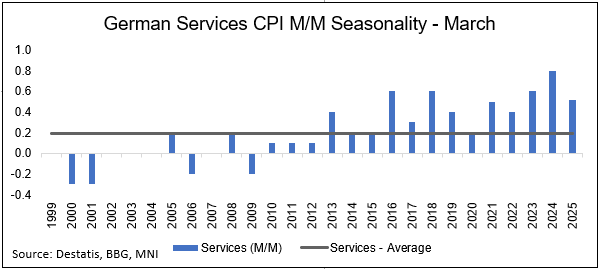

- Echoing January and February's releases, the M/M pace of services has slowed compared to the same period in 2023 and 2024 but remains elevated on a historical comparison - see chart below. The still elevated pace is noteworthy though, especially when considering that the Mar 2024 M/M would have been boosted by the timing of Easter as noted above.

EGBS: Core EGBs Supported As Further China Retaliation Weighs On Risk Sentiment

A further intensification of the US-China trade war has provided support to Bund futures this morning, but signs that further retaliatory tariff increases are unlikely from the Chinese side may have limited the rally. Heavy Italian supply (E9bln of 3/7/13-year BTPs) will have capped upside in the run-up to the 1000BST bidding deadline, but this channel should now fade after acceptable auction results.

- Bund futures are +30 ticks at 130.66, having tested yesterday’s high of 130.73. Wednesday’s range provides initial support and resistance levels (128.60 and 130.75 respectively). On the upside, clearance of Wednesday's high exposes 131.32, the 76.4% retracement of the Apr 7 - 9 pullback.

- The German curve has bull steepened, with Schatz ~5.5bps lower at 1.73%. 10-year yields are down 2bps on the session.

- 10-year peripheral spreads to Bunds once again display a strong correlation with global risk sentiment, with the 10-year BTP/Bund spread widening 4.5bps back to 129bps. The spread is currently up 10bps on the week, reflecting a ratchet higher in EUR 3m10y swaption vol.

- US PPI and UMich data headline today’s US macro calendar, but tariff headlines – in particular any response to China’s latest retaliation – are the primary focus.

GILTS: Off Lows But Wider Vs. Peers

Gilt spreads hold wider vs. peers.

- This morning’s firmer-than-expected UK GDP data drove the initial sell off and widening, before the latest round of Chinese retaliatory tariffs on the U.S. provided some outright support (albeit with China signalling a top in tariffs on the U.S.).

- Futures recovered from lows of 90.78 to ~91.20 last, sticking within yesterday’s range.

- Bears remain in control from a technical perspective, initial support and resistance located at Wednesday’s low (89.99) & the 20-day EMA (91.96), respectively.

- Benchmark yields last little changed to 6bp higher, curve steepens.

- Long end yields remain below Wednesday’s highs.

- 2s10s curve below cycle highs, last 78bp, but the likes of 2s30s, 5s30s and 10s30s have all registered fresh cycle highs.

- A reminder that even thinner-than-usual liquidity and forced liquidations were touted as key drivers of Wednesday’s weakness in the long end. Diminished liquidity may be lingering.

- BoE-dated OIS unwinds most of the early hawkish adjustment as gilts recover from lows, pricing 25bp of cuts for May, 36.5bp through June and 88bp through year-end. ’25 meeting contracts are little changed to ~2bp more hawkish on the day.

- SONIA futures +5.5 to -1.0, strip twist flattens.

- We don’t see today’s GDP data as a gamechanger for BoE policy, at least in isolation.

- Expect macro cues to dominate into the weekend.

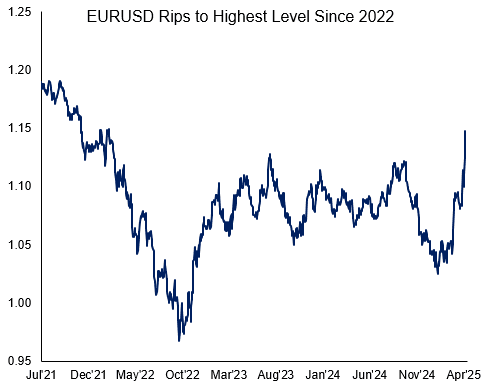

FOREX: EURUSD Extends Sharp Gains, Eyes 2022 Highs ~1.1500

- The relentless dollar selling across Thursday has filtered through into Friday’s session, culminating in a further 1.5% depreciation for the US dollar index to levels below the psychological 100.00 mark. Price action has been exacerbated by China announcing additional tariffs on US goods, reaching 125%.

- The Euro has been the key beneficiary of price dynamics this morning. Intra-day EURUSD gains currently stand at ~2%, however spot managed to reach as high as 1.0473, placing the pair at its highest level since early 2022.

- This has substantially narrowed the gap to 1.1495, the Feb 10 2022 high and a key medium term technical point. Should the blowout price action continue, a Fibonacci projection level at 1.1555 is notable. Initial support lies at the 1.1144 breakout level.

- Greenback losses have remained broad based, with the safe haven JPY and CHF also trading in a constructive manner. USDJPY has traded as low as 142.07, extending a clean break below 144 overnight. Sights are on 141.65 next, the Sep 30 ‘24 low.

- For USDCHF, price action has remained aggressive following the break of 0.8333 yesterday. The pair continues to trade at fresh ten-year lows, printing 0.8111 this morning. Emphasising the severity of the move, this extends the USDCHF selloff from the February highs to 11.8%. The next target for the move is at 0.8028 - 1.382 projection of the May 1 '24 - Sep 6 '24 - Jan 13 price swing.

- The China tariff news is weighing on the AUD, a relative underperformer in G10, and even diverging from its antipodean counterpart (AUDNZD down 1.3%).

- US PPI and preliminary U Mich sentiment data highlights the data calendar on Friday.

COMMODITIES: Bearish Oil Theme Intact

The trend condition in Gold remains bullish and this week’s rally confirms and reinforces this condition. The yellow metal has traded through $3167.8, the Apr 3 high, to resume the primary uptrend and trade to fresh all-time highs. A bearish theme in WTI futures remains intact and Wednesday’s rally from the day low is - for now - considered corrective. The move higher is allowing an oversold trend condition to unwind.

- WTI Crude down $0.12 or -0.2% at $59.8

- Natural Gas down $0.03 or -0.87% at $3.511

- Gold spot up $39.05 or +1.23% at $3217.3

- Copper up $7.2 or +1.66% at $440.55

- Silver up $0.07 or +0.23% at $31.2935

- Platinum up $6.63 or +0.71% at $940.82

EQUITIES: EuroStoxx Rally Could Signal Start of Correction

A short-term reversal in S&P E-Minis on Wednesday highlights the start of what appears to be a corrective cycle. The trend condition has been oversold following recent weakness and the move higher is allowing this set-up to unwind. Eurostoxx 50 futures have traded in an extremely volatile manner this week and rallied sharply higher from this week’s lows. The climb highlights the start of a corrective cycle and if this is correct, marks an unwinding of the recent oversold trend condition.

- Japan's NIKKEI closed lower by 1023.42 pts or -2.96% at 33585.58 and the TOPIX ended 72.49 pts lower or -2.85% at 2466.91.

- Elsewhere, in China the SHANGHAI closed higher by 14.589 pts or +0.45% at 3238.227 and the HANG SENG ended 232.91 pts higher or +1.13% at 20914.69.

- Across Europe, Germany's DAX trades lower by 369.17 pts or -1.8% at 20199.17, FTSE 100 lower by 36.18 pts or -0.46% at 7874.79, CAC 40 down 91.04 pts or -1.28% at 7042.92 and Euro Stoxx 50 down 70.76 pts or -1.47% at 4751.91.

- Dow Jones mini down 231 pts or -0.58% at 39564, S&P 500 mini down 21.25 pts or -0.4% at 5333.75, NASDAQ mini down 79 pts or -0.43% at 18418.

| Date | GMT/Local | Impact | Country | Event |

| 11/04/2025 | 0940/1040 | BoE's Saporta on 'How financial crisis reshape market and strategies’ | ||

| 11/04/2025 | 0945/1145 | ECB's Lagarde at Eurogroup Press Conference | ||

| 11/04/2025 | - | *** | Money Supply | |

| 11/04/2025 | - | *** | New Loans | |

| 11/04/2025 | - | *** | Social Financing | |

| 11/04/2025 | 1230/0830 | *** | PPI | |

| 11/04/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 11/04/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 11/04/2025 | 1400/1000 | St. Louis Fed's Alberto Musalem | ||

| 11/04/2025 | 1500/1100 | New York Fed's John Williams | ||

| 11/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 11/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |