MNI US MARKETS ANALYSIS - USD Index Breaks to New Low

Highlights:

- USD Index through to new '25 lows as negative short-term momentum builds further

- Unilateral tariffs up next, Trump sends letters as trade deals left wanting

- US 30yr auction the next litmus test for Treasury demand, US PPI also due

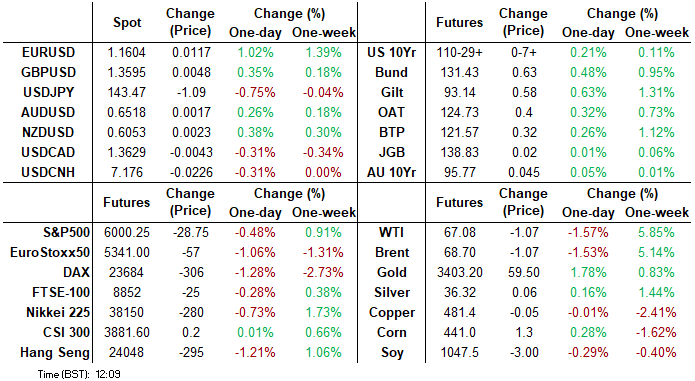

US TSYS: TYU5 Finds Resistance At Pre-NFP Highs; Data and 30Y Supply Ahead

- Treasuries have extended yesterday’s CPI-driven rally, underperforming EGBs and Gilts.

- President Trump said he intends to send letters to trading partners setting unilateral tariff rates in the next two weeks, ahead of a July 9 deadline to reimpose paused duties.

- Beyond PPI and weekly jobless claims at 0830ET, attention should turn to 30Y supply. Yesterday’s 10Y auction stopped through by a healthy 0.9bps but bid-to-cover faded from 2.60x to 2.52x and indirect take-up nudged lower.

- Cash yields are 3.3-4.4bp lower, with 2s lagging the decline whilst 5s through 30s otherwise see similar moves.

- 2s10s at 46.5bp (-1bp) tick back closer to towards recent flats whilst 5s30s at 89.9bp (unch) consolidates yesterday’s steepening back above pre-NFP levels.

- TYU5 has seen session highs of 110-29 overnight (+07), on solid cumulative volumes of 375k following some particularly subdued overnight sessions earlier this week.

- It’s finding some resistance here, with 110-29+ the Jun 6 high, after which lies 111-14+ (Jun 5 high and 61.8% retrace of May 1 -22 downleg). Extending the recovery from Wednesday’s low, it cancels a recent bearish threat for now. Support is seen at 109-26 (May 29 low).

- Data: Jobless claims (0830ET), PPI May (0830ET), Household net worth Q1 (1200ET)

- Coupon issuance: US Tsy $22B 30Y Bond auction re-open - 912810UK2 (1300ET)

- Bill issuance: US Tsy $65B 4W & $55B 8W bill auctions (1130ET)

- Trump schedule: Potential comments from a Bill Signing Ceremony at 1100ET.

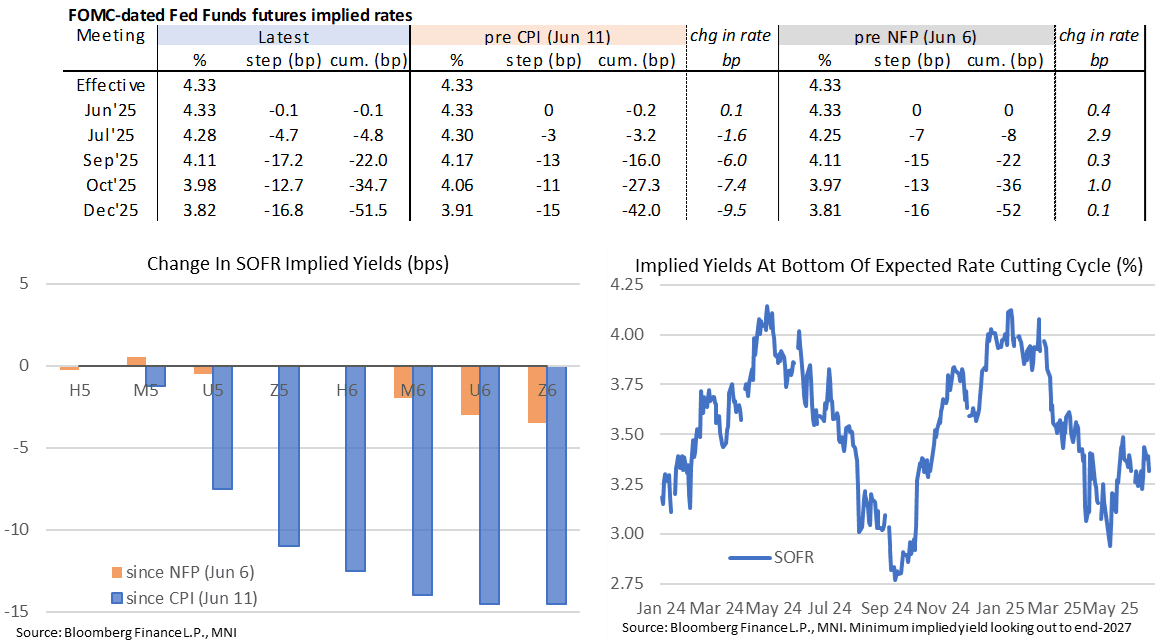

STIR: Holding Shift Back To 50bp Of Fed Cuts For 2025

- Fed Funds implied rates for 2025 meetings have modestly extended yesterday’s drop on a soft CPI report, amidst broader fixed income rallies.

- It has reversed the shunt higher seen on Friday's reasonably solid payrolls report having approached payrolls with a string of dovish releases.

- Cumulative cuts from 4.33% effective: 0bp Jun, 5bp Jul, 22bp Sep, 34.5bp Oct and 51.5bp Dec (42bp pre-CPI).

- The SOFR implied terminal yield of 3.285% (SFRZ6, -3bp) is 14.5bp lower since CPI.

- The FOMC is of course in media blackout. Today’s docket focus is on jobless claims and PPI, both at 0830ET, with the latter’s implications for core PCE helping shape next week’s FOMC projections.

- Tsy Sec Bessent yesterday indicated he'd like to remain in the role until 2029 – of note given reports and market speculation that he could be named Powell's successor as Fed Chair in the near future.

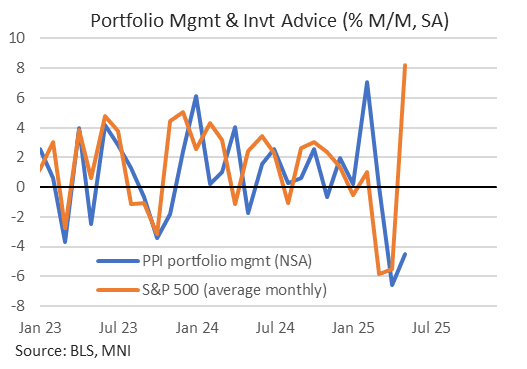

US OUTLOOK/OPINION: Wide Range To Core PCE Estimates, PPI Portfolio Mgmt Watched

- There remains a wide range of estimates for core PCE inflation in May (0.11-0.35% M/M across analysts below, after 0.12% M/M in April) following yesterday’s CPI release.

- Today’s PPI release is likely to see a sizeable narrowing in this range. There are many, mostly services-related, components that feed into core PCE but we expect most attention this month on portfolio management & investment advice after its -6.6% M/M drop dragged circa -0.12pps from core PCE in April.

- The S&P 500 increased 8.2% M/M in May when looking at monthly averages after -5.5% in April and -5.9% in March but the lags at which these moves filter into the PPI category are uncertain.

- This category is also prone to large revisions (on the subject of which, February's 7.0% M/M jump still looks out of kilter with market moves).

Analyst estimates for % M/M core PCE inflation.

- BNP Paribas: 0.11% - assuming an 8bp drag from portfolio mgmt owing to 1-mth lag to S&P 500. [we estimate that 8 looking for a circa -4.5%]

- TD Securities: 0.16%

- Goldman Sachs: 0.18%

- JPMorgan: 0.19%

- BofA: 0.18-0.24%

- Nomura: 0.35% - eyeing portfolio mgmt & invt advice +4.4% after -6.6%

UK FISCAL: Spending Review: Credibility concerns on health, defence, admin

- On our first 24 hour read of the Spending Review details we are most concerned about the credibility of health productivity and spending (despite the headline increases), the future increases in defence spending and the ability to deliver admin cuts on the scale suggested.

- Together with higher bond yields and inflation remaining relatively sticky as well as global growth forecast downgrades, as well as the April monthly borrowing figures coming in GBP3.5bln above the OBR's forecasts, it looks as though there will be a sizeable requirement for Chancellor Reeves to increase taxes in the Autumn Budget if she is to meet her fiscal rules.

- Despite health and social care spending making up the largest part of the budget and being discussed as one of the big winners, all of the increase in the budget in real terms is in current spending. Health and social care real spending will average 2.8% in real terms between FY25-26 and FY29-28 (NHS England 3.0%).

- However, the IFS had estimated ahead of the event that this would need to rise by 3.6%p.a. in order to keep up with the aging population - and this was based on the same optimistic 2%p.a. healthcare productivity target that the NHS has held since the Conservative government. The latest NHS productivity figures refer to FY22/23 (so are very stale) but show that productivity was 7.8% below the FY17/18 peak (and 5.3% below the largely pre-Covid FY19/20. There is therefore some scope for a catch up but annual average healthcare productivity growth in the first 20 years of the decade was below 1%. It is therefore questionable whether the current spending on health is realistic, or if it will need to be increased further.

- Also, growth on capital spending on health and social care will average 0.0% in real terms between FY25-26 and FY29-30. There was an increase in capital spending in recent years - but with a number of hospitals requiring rebuilds due to RAAC safety issues this won't leave a lot to spend on extra equipment (which would help with the increased productivity targets).

- Defence spending has been confirmed to be increasing to 2.6% of GDP by 2027 with a commitment to increase this to 3% in the next parliament. Note that the 3% figure is not currently costed in any plans by the OBR (as they only consider plans in the current parliament). The NATO plan of 3.5% of GDP (plus 1.5% on defence-related spending like cybersecurity, defence infrastructure etc) looks likely to be agreed to at some point - but that is not costed at all at present.

- The increase in the police budget will be partly funded through the increase in the police council tax precept - and it looks increasingly likely that the 5% cap on annual council tax increases (which would of course be a real terms increase) will be utilised by almost all councils to help fund this in future. This technically isn't a tax rise as it was already allowed under current rules - but makes smaller increases increasingly unlikely.

- Admin budgets are being cut by an average of 11% between FY25-26 and FY28-29 - and cumulatively by 16% in the five years to FY29-30. Admin budgets are always a target by successive governments, but seldom delivered on in full.

SOFR: Net Long Setting & Short Cover Seen In Futures On Wednesday

OI data points to a mix of net long setting and short cover as SOFR futures rallied on the back of the softer-than-expected CPI data on Wednesday.

- Net long setting was more prominent in the whites and reds, before net short cover came to fore in the greens and blues.

| 11-Jun-25 | 10-Jun-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,062,905 | 1,067,089 | -4,184 | Whites | +15,930 |

SFRM5 | 1,424,478 | 1,432,899 | -8,421 | Reds | +28,373 |

SFRU5 | 1,169,533 | 1,164,347 | +5,186 | Greens | -3,977 |

SFRZ5 | 1,162,763 | 1,139,414 | +23,349 | Blues | -4,330 |

SFRH6 | 924,414 | 909,425 | +14,989 |

|

|

SFRM6 | 875,500 | 857,427 | +18,073 |

|

|

SFRU6 | 790,643 | 787,983 | +2,660 |

|

|

SFRZ6 | 854,245 | 861,594 | -7,349 |

|

|

SFRH7 | 655,511 | 659,966 | -4,455 |

|

|

SFRM7 | 596,190 | 600,624 | -4,434 |

|

|

SFRU7 | 430,124 | 426,207 | +3,917 |

|

|

SFRZ7 | 405,684 | 404,689 | +995 |

|

|

SFRH8 | 306,633 | 305,079 | +1,554 |

|

|

SFRM8 | 214,295 | 218,742 | -4,447 |

|

|

SFRU8 | 169,460 | 169,586 | -126 |

|

|

SFRZ8 | 167,761 | 169,072 | -1,311 |

|

|

US TSY FUTURES: Net Long Setting Dominated On Wednesday

OI data points to relatively meaningful net long setting (in cumulative terms) across all contracts as Tsys rallied in the wake of Wednesday’s softer-than-expected CPI reading.

- The most prominent round of net long setting came in the belly/intermediates (FV through UXY), which accounted for ~$5.4mln of the ~$6.9mln DV01 equivalent net longs that were added across the curve.

| 11-Jun-25 | 10-Jun-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 3,966,655 | 3,963,068 | +3,587 | +141,484 |

FV | 6,824,303 | 6,785,390 | +38,913 | +1,701,118 |

TY | 4,749,071 | 4,718,987 | +30,084 | +1,999,284 |

UXY | 2,318,490 | 2,299,434 | +19,056 | +1,669,148 |

US | 1,723,377 | 1,720,782 | +2,595 | +359,099 |

WN | 1,893,590 | 1,888,105 | +5,485 | +988,095 |

|

| Total | +99,720 | +6,858,227 |

EUROPE ISSUANCE UPDATE:

Italy auction results

- E2.50bln of the 2.65% Jun-28 BTP. Avg yield 2.24% (bid-to-cover 1.63x).

- E3.00bln of the 3.25% Jul-32 BTP. Avg yield 3.02% (bid-to-cover 1.48x).

- E1.25bln of the 4.30% Oct-54 BTP. Avg yield 4.26% (bid-to-cover 1.60x).

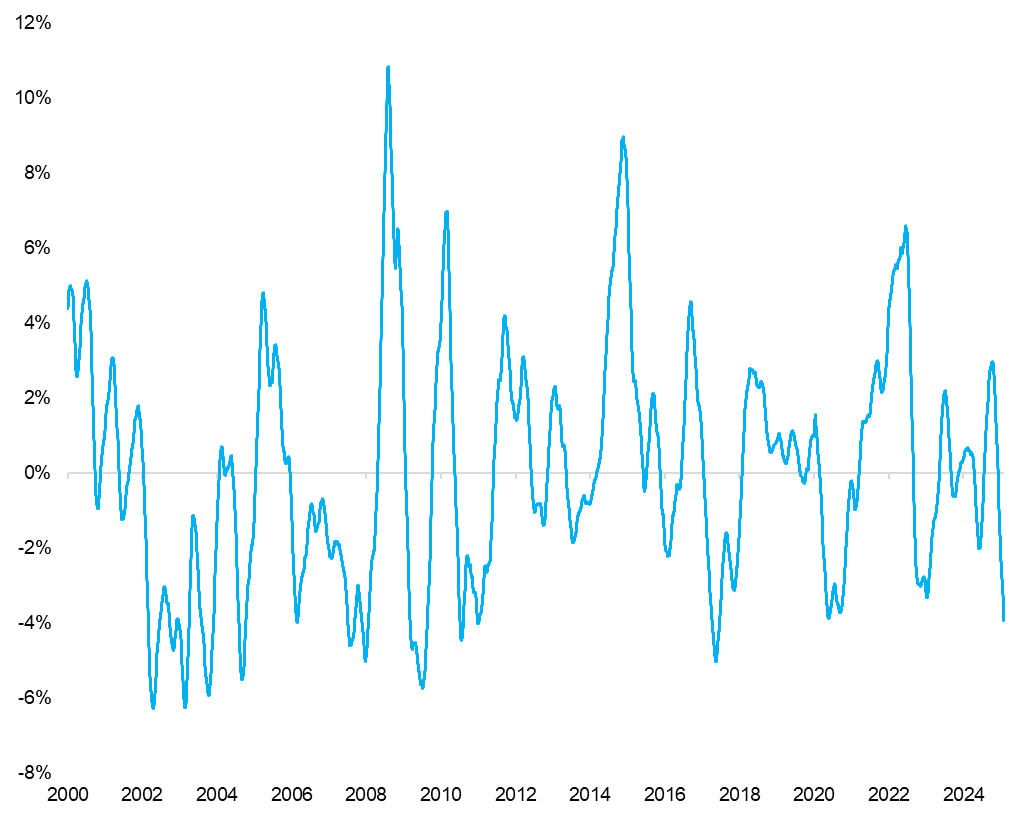

FOREX: EUR a Key Beneficiary as USD Index Breaks to New Low

- EUR/USD through to new YTD highs on this latest phase of USD weakness, with a clear uptick in price action, volumes and activity on the break of 1.1573, the mid-April and previous year-to-date high.

- This price action is making for solid FX futures volumes at the NY crossover: just over 3,000 EUR futures contracts traded on the break of the level - a cash equivalent of ~$570mln and easily the best volumes of the day

- We noted earlier this morning that 1.1573 was the key level, with that mark broken, 1.1608 is the 09-Nov 2021 high. We note close to E3bln notional is set to roll-off at the 1.1600 handle in EUR/USD over the coming week - the largest of which expire today and Monday.

- This keeps the downtrendline resistance intact for the USD Index, which has shown well through the April low of 97.921. There is now a near 4% premium for the 200-dma over the 50-dma for the first time since the throes of COVID in 2020 - characterising the still building S/T negative momentum in the USD.

Figure 1: USD Index 50-dma premium over 200-dma (%)

Source: Bloomberg Finance L.P. / MNI

GBP: Second Leg of Sales Supports Sell-on-Rallies Theme

- GBP is underperforming through this latest USD bounce, dragging the pair further off the overnight recovery high of 1.3593, as the soft growth data prevents any material test on the $1.3600 handle (which would open markets to gains toward YTD highs) and raises the risk of a sell-on-rallies phase for the pair, characterised by slowing momentum in long positioning, sliding call vol premiums, shakier UK data and sticky BoE pricing around 2 x 25bps rate cuts later this year.

- Yesterday's GBP/USD rally on the US CPI print may firm this view: in contrast with broader G10, the pair failed to top the Tuesday high despite the break lower in the USD Index and the move in the US/UK 2yr yield spread. Any bounce for the greenback could disproportionately impact GBP, with Wednesday's UK inflation print the next flashpoint for activity.

- A technical correction lower would target 1.3504 ahead of layered support between 1.3434-44, marked by a series of historic highs (Sep'24, Apr'25) as well as the 38.2% retracement of the upleg off mid-May low.

FOREX: EURUSD Extends Post US CPI Gains to 1.1%, Broad Euro Strength Notable

- Building on its recent resilient profile, EURUSD has rallied well in the aftermath of the US inflation data, gaining 1.1% from pre-data levels. Momentum has extended above the post-ECB peak at 1.1495, confirming an extension of the current bull cycle.

- Outperformance for the single currency has been notable as market participants continue to cite the recent hawkish turn from the ECB and the building narrative around the Euro’s global reserve status as gaining traction. EURAUD and EURNZD building on yesterday’s gains is evidence of this, helped by a slightly more fragile equity backdrop on Thursday. Both crosses have traded up to fresh six-week highs at 1.7789 and 1.9172 respectively.

- Softer risk sentiment has stalled the progress for EURJPY this morning, however, yesterday’s advance did mark the fifth consecutive session of gains. Above here, 166.69 (Oct 31 high) is a key resistance for EURJPY, before a couple of daily highs around the 168 mark. The prior breakout point at 165.21 is initial support.

OPTIONS: Expiries for Jun12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1350(E1.9bln), $1.1395-00(E1.3bln), $1.1425-35(E1.4bln), $1.1440-50(E2.7bln), $1.1500(E2.4bln), $1.1525(E835mln)

- USD/JPY: Y143.00($1.3bln), Y143.85-00($1.0bln)

- GBP/USD: $1.3400-15(Gbp690mln)

- AUD/USD: $0.6475-85(A$1.1bln), $0.6500(A$532mln), $0.6520-30(A$992mln), $0.6600(A%643mln)

- USD/CAD: C$1.3750($833mln)

- USD/CNY: Cny7.1600($515mln), Cny7.2200($831mln)

EQUITIES: Moving Average Studies for Eurostoxx 50 Futures in Bull-Mode Position

- Eurostoxx 50 futures are trading inside a range for now. The trend condition is bullish - moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Clearance of this level would strengthen the bull theme. Key support to watch lies at 5295.43, the 50-day EMA. A clear break of this average would signal a possible reversal.

- The trend condition in S&P E-Minis remains bullish and the contract traded to a fresh cycle high yesterday, reinforcing current bullish conditions. The recent break of 5993.50, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. Sights are on 6080.75 next, the Feb 26 high. Key support to watch lies at 5816.70, the 50-day EMA.

COMMODITIES: Gains for WTI Futures This Week Mark Acceleration of Bull Phase

- WTI futures have traded higher this week and yesterday’s gains mark an acceleration of the current bull phase. The contract has cleared all key retracement points of the Apr 2 - 9 bear leg and this signals scope for an extension towards $71.10 the Apr 2 high and a key hurdle for bulls. A break of this level would strengthen the bullish condition. On the downside, initial firm support to watch is $63.04, 50-day EMA.

- A bullish theme in Gold remains intact and the latest pullback appears corrective. Medium-term trend signals remain bullish - moving average studies are in a bull-mode position, highlighting a dominant uptrend. An extension higher would open $3435.6 next, the May 7 high. A break of this hurdle would strengthen bullish conditions. On the downside, support to monitor is $3249.9, the 50-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 12/06/2025 | - | *** | Money Supply | |

| 12/06/2025 | - | *** | New Loans | |

| 12/06/2025 | - | *** | Social Financing | |

| 12/06/2025 | 1200/1400 | ECB de Guindos At Financial Integration Conference | ||

| 12/06/2025 | 1220/1420 | ECB Schnabel At Financial Integration Conference | ||

| 12/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 12/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 12/06/2025 | 1230/0830 | * | Household debt-to-income | |

| 12/06/2025 | 1230/0830 | *** | PPI | |

| 12/06/2025 | 1400/1000 | * | Services Revenues | |

| 12/06/2025 | 1415/1615 | ECB Elderson At Senior Supervisors Conference | ||

| 12/06/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 12/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 12/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 12/06/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/06/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 13/06/2025 | 2301/0001 | ** | KPMG/REC Jobs Report | |

| 13/06/2025 | 0430/1330 | ** | Industrial Production | |

| 13/06/2025 | 0600/0800 | *** | Final Inflation Report | |

| 13/06/2025 | 0600/0800 | *** | HICP (f) | |

| 13/06/2025 | 0645/0845 | *** | HICP (f) | |

| 13/06/2025 | 0700/0900 | *** | HICP (f) | |

| 13/06/2025 | 0830/0930 | ** | Bank of England/Ipsos Inflation Attitudes Survey | |

| 13/06/2025 | 0900/1100 | ** | Industrial Production | |

| 13/06/2025 | 0900/1100 | * | Trade Balance | |

| 13/06/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 13/06/2025 | 1230/0830 | ** | Wholesale Trade | |

| 13/06/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 13/06/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 13/06/2025 | 1500/1700 | ECB Elderson At Senior Supervisor's Conference | ||

| 13/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 13/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |